- Home

- »

- Advanced Interior Materials

- »

-

Water Clarifiers Market Size And Share Report, 2026-2033GVR Report cover

![Water Clarifiers Market (2026 - 2033)Report]()

Water Clarifiers Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Conventional Clarifiers, Lamella Clarifiers, Tube Settler Clarifiers, Sludge Blanket Clarifiers, Solids Contact Clarifiers, Ballasted Clarifiers), By End Use, By Application, By Region, And Segment Forecasts

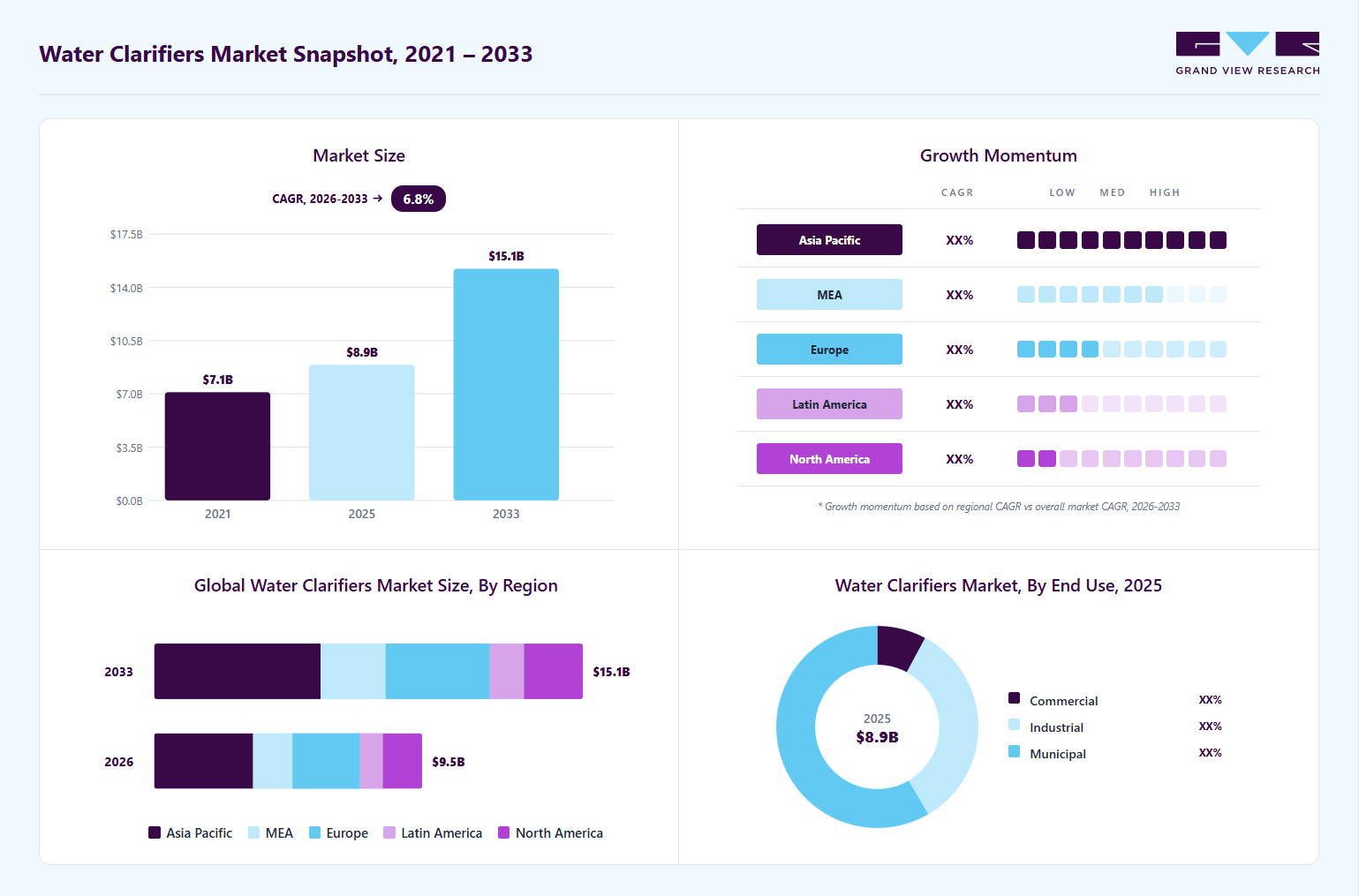

Market Size, 2025

$8.9BMarket Estimate, 2026

$9.5BMarket Forecast, 2033

$15.1BCAGR, 2026–2033

6.8%Water Clarifiers Market Summary

The global water clarifiers market size was valued at USD 8.9 billion in 2025 and is projected to grow from USD 9.5 billion in 2026 to USD 15.1 billion by 2033, at a CAGR of 6.8% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 36.0% in 2025. Increasing global investment in municipal wastewater treatment infrastructure is a major factor driving the market growth.

Key Market Trends & Insights

- By end use: Municipal segment held the largest market share of 58.2% in 2025.

- By application: Primary clarification segment held the largest market share of 44.1% in 2025.

- By type: Conventional clarifiers segment held the largest market share of 38.3% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (36.0% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 8.9 Billion

- Estimated market size in 2026: USD 9.5 Billion

- Projected market size by 2033: USD 15.1 Billion

- CAGR (2026-2033): 6.8%

")

Governments and utilities are expanding and upgrading treatment facilities to address rising urbanization, aging infrastructure, and stricter water quality regulations. This is increasing demand for both conventional and high-rate clarification systems across primary, secondary, and tertiary treatment applications. The market is aided by growing industrial water reuse initiatives, rising adoption of compact treatment technologies, and tightening environmental discharge standards. Industries such as power generation, mining, food & beverage, and chemicals are increasingly investing in advanced clarification systems to improve water recovery efficiency and reduce wastewater discharge volumes.Market Dynamics

The growth of the water clarifiers industry is driven by increasing municipal and industrial wastewater treatment investments, stricter environmental regulations, rising water reuse requirements, and growing demand for efficient solids separation technologies. Expanding urban populations, industrialization, and the need for compact high-rate treatment systems are further supporting the adoption of advanced clarification technologies globally.

The growth of the water clarifiers market is restrained by high capital installation costs, operational complexity associated with advanced clarification systems, and the long replacement cycles of existing treatment infrastructure. In many developing regions, limited funding for water treatment upgrades and the continued reliance on conventional sedimentation systems can slow the adoption of newer high-rate clarification technologies. Additionally, fluctuations in municipal spending and industrial capital expenditure can impact large-scale project investments.

Market Concentration & Characteristics

The water clarifiers market is relatively consolidated, with competition led by established water treatment equipment manufacturers offering broad municipal and industrial treatment portfolios. Large players benefit from strong global distribution networks, long-term municipal relationships, and integrated treatment capabilities, while regional and niche companies compete through customized engineering solutions and specialized clarification technologies. The market is also characterized by high project-based competition and long procurement cycles for large infrastructure developments.

Stringent environmental regulations related to wastewater discharge, nutrient removal, and water reuse are playing a major role in shaping market demand. Governments and environmental agencies across North America, Europe, and Asia Pacific are increasing investments in wastewater treatment upgrades and advanced tertiary treatment infrastructure. These regulations are accelerating the adoption of high-efficiency clarification systems capable of meeting stricter water quality and sludge management standards.

Technological advancements such as compact high-rate clarifiers, ballasted clarification systems, and enhanced sludge handling solutions are reshaping the competitive landscape. Manufacturers are increasingly focusing on automation integration, process optimization, reduced footprint systems, and energy-efficient operations to improve treatment performance. Leading companies are also expanding through partnerships, acquisitions, and infrastructure modernization projects to strengthen their presence in growing municipal and industrial water treatment markets.

Types Insights

The conventional clarifiers segment led the market in 2025 in terms of revenue share, holding 38.3% of the market. These systems are widely preferred for large-capacity treatment applications because of their operational reliability, established infrastructure compatibility, and comparatively lower capital costs. The demand continues to be supported by ongoing municipal infrastructure upgrades and replacement projects in both developed and developing regions.

Ballasted clarifiers are estimated to be the fastest-growing segment within the water clarifiers industry due to their ability to deliver high-rate treatment performance within significantly smaller footprints compared to conventional clarification systems. These systems use ballast media to accelerate solids settling, enabling significantly higher treatment efficiency within smaller footprints than conventional clarification technologies. Growing investments in tertiary treatment, water reuse projects, and space-constrained urban treatment facilities are driving the global adoption of ballasted clarification systems.

End Use Insights

The municipal segment accounts for the largest share of the water clarifiers market, driven by extensive deployment in drinking water treatment plants and municipal wastewater treatment facilities. Increasing urbanization, population growth, and surging investments in wastewater infrastructure modernization are supporting continued demand for clarification systems globally. Governments and utilities are also expanding tertiary treatment and water reuse capabilities to comply with stricter environmental regulations and address growing water scarcity concerns.

The industrial segment is expected to witness the strong growth over the forecast period at an estimated CAGR of 8.9%. This growth is driven by the increasing investments in industrial wastewater treatment, process water recycling, and water reuse initiatives across sectors such as power generation, mining, chemicals, food & beverage, and semiconductors. Stricter discharge regulations and rising water management costs are encouraging industries to adopt advanced clarification technologies to improve treatment efficiency and reduce freshwater consumption. Additionally, the rapid expansion of industry in emerging economies is a key driver of demand for water clarifiers, as industrial water and wastewater treatment infrastructure grows.

Application Insights

The primary clarification represented a key segment in 2025, accounting for 44.1% of the revenue share. The primary clarification segment represents the initial sedimentation stage of the water treatment process, immediately following raw water intake or grit screening. Municipal and industrial facilities heavily utilize conventional circular or rectangular clarifiers in this phase to reduce overall turbidity and lower biochemical oxygen demand (BOD) loads. Market growth for this segment is primarily driven by rapid global urbanization and industrial expansion, which drastically increase raw wastewater volumes. Additionally, the critical need to protect sensitive, high-value downstream biological equipment from clogging and operational failure ensures consistent investment in robust primary clarification assets.

The tertiary clarification segment is the final sedimentation stage designed to polish treated wastewater before it is reused or safely discharged into the environment. Since tertiary solids are light and difficult to settle, this market segment is a major driver of growth for high-efficiency, advanced technologies such as lamella plates, solids-contact systems, and ballasted clarifiers. The segment is heavily propelled by increasingly strict government environmental mandates governing nutrient discharge limits. Furthermore, the global corporate push toward sustainability, water scarcity solutions, and zero liquid discharge (ZLD) practices is forcing industrial plants to adopt tertiary clarification more widely for process water recycling.

Regional Insights

North America represents a significant market for water clarifiers due to strong investments in municipal wastewater treatment upgrades, aging water infrastructure replacement, and stringent environmental regulations related to water quality and discharge standards. The region is witnessing increasing adoption of advanced clarification technologies such as lamella and ballasted clarifiers, particularly in tertiary treatment and water reuse applications. Industrial demand from sectors such as power generation, chemicals, food & beverage, and semiconductors is also contributing to market growth, supported by a rising focus on water recycling and sustainable water management practices.

U.S. Water Clarifiers Market Trends

The U.S. represents a mature, high-value market for water clarifiers, where demand is primarily driven by the replacement and upgrading of aging municipal infrastructure. Stringent environmental regulations enforced by the EPA, particularly regarding nutrient limits and stormwater management, heavily propel the adoption of high-rate technologies such as ballasted clarifiers and advanced tertiary systems. Additionally, robust investments in the domestic semiconductor, oil and gas, and pharmaceutical industries stimulate steady demand for high-efficiency solids contact and lamella clarifiers for industrial process water pretreatment.

Europe Water Clarifiers Market Trends

The Europe water clarifiers industry is characterized by mature infrastructure, a strong emphasis on environmental sustainability, and stringent European Union directives regarding nutrient removal. Due to strict municipal discharge limits for phosphorus and nitrogen, Europe stands out as a highly technically advanced region, serving as a primary driver for sophisticated tertiary clarification and solids contact systems.

Germany water clarifiers market represents a technologically advanced market, supported by stringent environmental regulations and strong emphasis on sustainable water management and circular economy initiatives. The market is characterized by significant investments in upgrading existing municipal wastewater treatment infrastructure, driving the adoption of high-efficiency technologies such as tube settlers and lamella clarifiers in retrofit projects. Regulatory requirements related to phosphorus removal, micropollutant treatment, and wastewater discharge standards are further supporting demand for advanced tertiary clarification systems and automated process control technologies that improve treatment efficiency and chemical dosing optimization.

The water clarifiers market in France is relatively consolidated and technologically advanced, supported by the presence of major global water treatment companies and strong regulatory oversight. Market growth is closely linked to compliance with European Union environmental regulations and increasing investments in climate resilience and sustainable water management infrastructure. The country is witnessing growing adoption of compact ballasted clarification systems for managing variable urban wastewater flows, along with increasing use of solids contact clarifiers in industrial process water treatment and water recycling applications.

Asia Pacific Water Clarifiers Market Trends

The Asia Pacific region represents the fastest-growing market for water clarifiers, fueled by rapid industrialization, massive population growth, and accelerating urbanization in major economies such as China, India, and Southeast Asian nations. Rising daily volumes of municipal sewage and industrial wastewater have prompted governments to heavily fund the construction of centralized wastewater treatment facilities. While conventional circular and rectangular clarifiers remain the key segment for large-scale primary treatment, the region's expanding manufacturing, mining, and textile industries are rapidly adopting lamella and sludge blanket systems to address severe local freshwater scarcity through process water recycling.

The China water clarifiers market is the one of the largest and fastest-growing markets for water clarifiers globally, driven by massive public-private partnership (PPP) investments and aggressive green initiatives outlined in its national economic plans. To meet strict urban discharge standards and combat widespread freshwater scarcity, the country is rapidly expanding its network of centralized municipal sewage plants. While conventional circular clarifiers remain highly sought after for large-scale primary treatment, strict Zero Liquid Discharge (ZLD) mandates in China's massive textile, electronics, and heavy manufacturing sectors are fueling a major surge in high-efficiency lamella and sludge blanket systems.

South Koreawater clarifiers market is a highly advanced and industrialized market focusing heavily on precision engineering and space constraints. The market is primarily propelled by the country's strong- semiconductor, automotive, and petrochemical manufacturing sectors, which require ultra-pure water and advanced industrial wastewater reclamation systems. Due to limited land availability and high urban density, the South Korea water clarifiers industry is rapidly adopting compact, packaged lamella clarifiers and high-rate separation technologies, heavily prioritizing automated systems embedded with smart water monitoring sensors.

Latin America Water Clarifiers Market Trends

The water clarifiers industry in Latin America is developing steadily driven by the region's massive mining, pulp and paper, and agricultural processing industries, which rely on large-scale solids contact and conventional clarifiers to handle heavy particulate loads and process water pretreatment. While municipal investments in sewage infrastructure have traditionally lagged behind, tightening public health policies and rising private sector participation in water utilities are expected to generate fresh demand for primary and secondary clarification systems to upgrade urban sanitation facilities.

Brazil water clarifiers market represents one of the largest markets in Latin America, supported by strong demand from resource-intensive industries such as pulp & paper, mining, and sugar processing. These industries extensively utilize conventional and solids contact clarifiers for raw water treatment and industrial wastewater management involving high particulate loads and complex effluents. In the municipal sector, ongoing regulatory reforms and increasing private sector participation in water infrastructure development are supporting investments in the modernization and expansion of primary and secondary clarification systems across urban wastewater treatment facilities.

Middle East & Africa Water Clarifiers Market Trends

The Middle East and Africa market operates under conditions of extreme water stress, making advanced water treatment and conservation an absolute necessity. In the GCC countries, the market is heavily skewed toward tertiary applications, where desalination pretreatment and municipal wastewater reuse for irrigation are vital; this creates high demand for specialized solids contact and ballasted systems. In contrast, the market in Africa is seeing a gradual increase in fundamental primary and secondary municipal infrastructure spending within the resource-rich mining sectors of South Africa and the Sub-Saharan region.

The market for water clarifiers in Saudi Arabia operates under conditions of severe natural water scarcity, making water conservation a critical national security priority under its strategic economic vision. The market is highly skewed toward industrial pretreatment and advanced tertiary clarification, as municipal wastewater must be extensively polished for reuse in agricultural irrigation and industrial cooling. The Kingdom’s massive investments in megaprojects and coastal industrial cities are expected to drive substantial procurement of high-capacity solids contact clarifiers and specialized ballasted systems to handle desalination pretreatment and complex industrial recycling.

Key Water Clarifiers Company Insights

Some of the key players operating in the market include Xylem Inc. and Veolia, among others.

-

Veolia is a multinational company engaged in designing and distributing water, waste, and energy management solutions. The company operates through three business segments, namely water management, waste management, and energy management. The company has operations worldwide covering the regions North America, Europe, Latin America, and Middle East & Africa with Europe and North America being its major geographical markets followed by Middle East & Africa.

-

Xylem, Inc is a global water technology company, engaged in the manufacture, designing and service of products that primarily cater to water sector as well as electric and gas sector. The company owns numerous brands and offers various water technology products under these brands such as water clarifiers, polarimeters, pumps, valves, reverse osmosis membrane filtration systems, and others.

Key Water Clarifiers Companies:

The following key companies have been profiled for this study on the water clarifiers market.

-

Xylem, Inc.

-

Veolia

-

WesTech Engineering, LLC

-

Parkson Corporation

-

Ovivo Water Inc

-

Smith & Loveless

-

Kusters Water

-

Sentry Equipment Corp.

-

Clearwater Industries, Inc

-

Hydroflux

-

KHN Water Treatment Equipments Co.,Ltd

-

Monroe Environmental Corp

-

MAK Water

-

AWC Water Solutions Ltd

-

Jorsun Environment Co., Ltd

-

AUC Group

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Xylem, Inc. Veolia, WesTech Engineering, LLC

- Mature market players focus on expanding integrated municipal and industrial water treatment portfolios supported by large-scale engineering and long-term service capabilities.

- These companies actively pursue infrastructure modernization projects, technology acquisitions, and strategic partnerships to strengthen their market presence.

- Mature players increasingly invest in automation, digital monitoring, and process optimization technologies to improve treatment efficiency and operational performance

- Mature players benefit from strong global brand recognition and extensive installed customer bases across municipal and industrial sectors.

- Their broad product portfolios enable them to offer integrated water treatment solutions across multiple clarification technologies and applications.

- Long-standing relationships with municipalities and industrial customers strengthen their competitive positioning in major infrastructure projects

- Their dependence on large municipal infrastructure projects can expose them to procurement delays and fluctuations in public spending.

- Premium pricing and higher operational overhead can reduce competitiveness in smaller and cost-sensitive projects

Emerging Players: MAK Water, Jorsun Environment Co., Ltd

- Emerging players primarily focus on modular treatment systems, customized engineering solutions, and decentralized water treatment applications.

- These companies actively target high-growth industrial wastewater treatment and water reuse projects across regional markets.

- Strategic collaborations, distributor agreements, and regional partnerships are commonly used to expand market presence and technical capabilities.

- Emerging players benefit from greater operational flexibility and faster responsiveness to project-specific customer requirements.

- Their leaner organizational structures often support quicker product customization and competitive project pricing.

- Emerging players generally operate with smaller global footprints and more limited financial resources compared to established competitors.

- Lower brand recognition and narrower service networks can restrict participation in large-scale municipal infrastructure projects.

Recent Developments

-

In May 2025, Smith & Loveless announced that its Australian subsidiary acquired CST Wastewater Solutions to strengthen its particle separation and wastewater inlet works portfolio across Australia and New Zealand. The acquisition expands Smith & Loveless’ capabilities in wastewater screening, grit removal, dewatering, and membrane bioreactor (MBR) screening technologies for municipal and industrial applications. The companies stated that the move builds on a long-standing partnership and is intended to enhance integrated wastewater treatment solutions and regional market presence.

-

In October 2024, AUC Group, a subsidiary of Seven Seas Water Group, acquired key assets of WAWCON, Inc. to strengthen its clarifier design and manufacturing capabilities for large-scale water and wastewater treatment projects. The acquisition expands AUC’s ability to offer larger clarifier systems exceeding 80 feet in diameter in both steel and concrete configurations, while also enhancing its expertise in clarifier internals and high-capacity treatment infrastructure.

Water Clarifiers Market Report Scope

Report Attribute

Details

Market size in 2025

USD 8.9 billion

Estimated market size in 2026

USD 9.5 billion

Projected market size by 2033

USD 15.1 billion

Growth rate

CAGR of 6.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market position analysis, competitive landscape, growth factors, and trends

Segments covered

Type, end use, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; China; India; Japan; South Korea; Australia; Brazil; Argentina; South Africa; Saudi Arabia; UAE

Key companies profiled

Xylem, Inc; Veolia; WesTech Engineering, LLC; Parkson Corporation; Ovivo Water Inc; Smith & Loveless; Kusters Water; Sentry Equipment Corp.; Clearwater Industries Inc; Hydroflux; KHN Water Treatment Equipments Co., Ltd; Monroe Environmental Corp; MAK Water; AWC Water Solutions Ltd; Jorsun Environment Co., Ltd; AUC Group

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.,

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Water Clarifiers Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global water clarifiers market based on type, end use, application, and region:

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Conventional Clarifiers

-

Lamella Clarifiers

-

Tube Settler Clarifiers

-

Sludge Blanket Clarifiers

-

Solids Contact Clarifiers

-

Ballasted Clarifiers

-

Others

-

-

End use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Municipal

-

Industrial

-

Commercial

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Primary Clarification

-

Secondary Clarification

-

Tertiary Clarification

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

A detailed regional segmentation analysis was delivered including assessment of key municipal and industrial water treatment markets. The analysis evaluated region-specific trends in wastewater infrastructure investments, industrial water reuse initiatives, environmental regulations, and adoption of advanced clarification technologies such as lamella and ballasted clarifiers.

The study enabled the client to identify high-growth regional markets, understand differences in technology adoption patterns, and evaluate infrastructure investment trends influencing clarifier demand. It also supported regional expansion planning, sales prioritization, and strategic market positioning decisions across municipal and industrial treatment sectors.

Competitive Benchmarking

A detailed competitive benchmarking analysis was delivered comparing leading and emerging water clarifier manufacturers based on product portfolio strength, clarification technology capabilities, geographic presence, end-use focus, and strategic initiatives. The assessment evaluated companies across conventional, lamella, tube settler, sludge blanket, solids contact, and ballasted clarification technologies.

The benchmarking analysis enabled the client to better understand the competitive landscape, identify technology differentiation opportunities, and evaluate the strategic positioning of key market participants. It also supported decision-making related to partnership evaluation, competitive intelligence, and long-term business strategy development.

Opportunity Assessment

A comprehensive opportunity assessment was delivered to identify high-growth application areas, emerging clarification technologies, and evolving water treatment infrastructure requirements within the global water clarifiers market. The assessment included analysis of tertiary treatment expansion, industrial water recycling trends, compact treatment system adoption, and growing demand for high-rate clarification technologies across municipal and industrial facilities.

The analysis enabled the client to identify attractive growth opportunities, prioritize investment areas, and evaluate future demand trends across key end-use sectors and regions. It also supported strategic decision-making related to product development, technology positioning, and long-term market expansion initiatives.

Frequently Asked Questions About This Report

The municipal segment led with a 58.2% revenue share in 2025.

The primary clarification segment dominated the market and accounted for the largest revenue share of 44.1% in 2025.

Conventional clarifiers segment held the largest share (over 38.0%) in 2025, while ballasted clarifiers is the fastest-growing types.

The global water clarifiers market is expected to grow at a CAGR of 6.8% from 2026 to 2033, reaching USD 15.1 billion by 2033.

The global water clarifiers market size was valued at USD 8.9 billion in 2025 and is estimated at USD 9.5 billion for 2026.

The Asia Pacific water clarifiers market dominated the global revenue share in 2025 accounting for 36% of the share, due to rapid urbanization, expanding industrial wastewater treatment investments, and increasing government spending on municipal water infrastructure modernization.

Key players include Xylem, Inc; Veolia; WesTech Engineering, LLC; Parkson Corporation; Ovivo Water Inc; Smith & Loveless; Kusters Water; Sentry Equipment Corp.; Clearwater Industries Inc; Hydroflux; KHN Water Treatment Equipments Co., Ltd; Monroe Environmental Corp; MAK Water; AWC Water Solutions Ltd; Jorsun Environment Co., Ltd; and AUC Group.

The water clarifiers market is primarily driven by rising investments in municipal and industrial wastewater treatment infrastructure, stricter environmental regulations, and growing demand for water reuse and recycling systems.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.