- Home

- »

- Plastics, Polymers & Resins

- »

-

Transparent Plastics Market Size, Industry Report, 2033GVR Report cover

![Transparent Plastics Market Size, Share & Trends Report]()

Transparent Plastics Market (2025 - 2033) Size, Share & Trends Analysis Report By Polymer Type (PET, PVC, PP, PS, PC, PMMA), By Form (Rigid, Flexible), By Application (Medical & Healthcare, Automotive, Consumer Goods), By Region, And Segment Forecasts

- Report ID: GVR-4-68040-691-9

- Number of Report Pages: 120

- Format: PDF

- Historical Range: 2021 - 2023

- Forecast Period: 2025 - 2033

- Industry: Bulk Chemicals

- Report Summary

- Table of Contents

- Segmentation

- Methodology

- Download FREE Sample

-

Download Sample Report

Download Sample Report

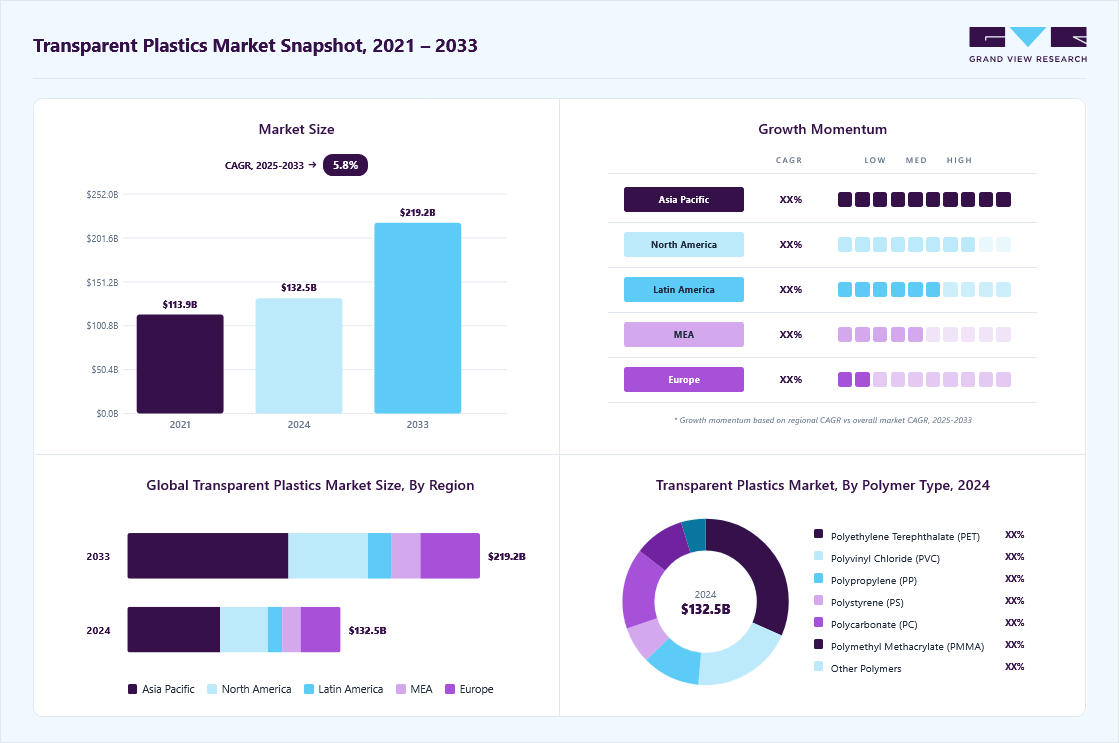

Market Size, 2024$132.5BMarket Estimate, 2025$139.5BMarket Forecast, 2033$219.2BCAGR, 2025 - 20335.8%Transparent Plastics Market Summary

The global transparent plastics market size was estimated at USD 132.54 billion in 2024 and is projected to reach USD 219.17 billion by 2033, growing at a CAGR of 5.8% from 2025 to 2033. A surge in e‑commerce and premium packaging demands is driving transparent plastics as brands seek clear, lightweight containers that showcase product quality and enhance shelf appeal.

Key Market Trends & Insights

- Asia Pacific dominated the transparent plastics market with the largest revenue share of 43.52% in 2024.

- The transparent plastics market in the U.S. is driven by the expansion of healthcare facilities and outpatient clinics.

- By polymer type, the polymethyl methacrylate (PMMA) segment is expected to grow at a considerable CAGR of 7.3% from 2025 to 2033 in terms of revenue.

- By form, the rigid segment is expected to grow at a considerable CAGR of 6.2% from 2025 to 2033 in terms of revenue.

- By applications, the medical & healthcare segment is expected to grow at a considerable CAGR of 7.4% from 2025 to 2033 in terms of revenue.

Market Size & Forecast

- 2024 Market Size: USD 132.54 Billion

- 2033 Projected Market Size: USD 219.17 Billion

- CAGR (2025-2033): 5.8%

- Asia Pacific: Largest market in 2024

Manufacturers benefit from streamlined production and reduced logistics costs when substituting glass with durable, shatter‑resistant polymer alternatives. The market is witnessing a pronounced shift towards bio‑based and recyclable resin formulations as sustainability becomes a central tenet of corporate strategy. Manufacturers are investing in advanced polymer chemistries that maintain optical clarity while enabling circularity through chemical recycling. Concurrently, there is growing adoption of additive manufacturing applications that leverage transparent thermoplastics for rapid prototyping and end‑use components. This convergence of environmental stewardship and manufacturing innovation is redefining market expectations and driving premiumization.")

Market Dynamics

The transparent plastics market is being driven by increasing demand for lightweight, high-clarity, and impact-resistant materials across packaging, healthcare, electronics, automotive, and construction industries. Transparent plastics offer superior optical properties, processability, chemical resistance, and design flexibility compared with traditional glass materials, making them highly suitable for modern industrial and consumer applications. The growing preference for visually appealing packaging and durable, lightweight materials continues to strengthen global market demand.

The market is further propelled by the rapid expansion of downstream premium packaging, consumer electronics, and display technology industries. Increasing demand for transparent food packaging, pharmaceutical containers, cosmetic packaging, electronic display panels, and protective films is driving strong demand for polycarbonate, acrylic, PET, and other specialty transparent polymers. Rising investment in retail-ready packaging, smart electronic devices, and advanced display systems is further accelerating the adoption of high-performance transparent plastic materials.

One of the major restraints affecting the plastic films and sheets market is increasing environmental concern regarding plastic waste generation and disposal. Governments and regulatory agencies across multiple regions are implementing stricter regulations related to single-use plastics, recycling mandates, and packaging sustainability requirements. These regulatory pressures are increasing compliance costs and forcing manufacturers to invest heavily in recyclable, biodegradable, and circular packaging technologies.

Market Concentration & Characteristics

The market growth stage is medium, and the pace is accelerating. The market exhibits fragmentation, with key players dominating the industry landscape. Major companies like Dow, Inc., SABIC, BASF SE, Covestro AG, PPG Industries, Inc., LyondellBasell Industries N.V., DuPont de Nemours, Inc., INEOS Group Limited, LANXESS AG, Berry Global, Cosmo Films, Amcor plc, and others play a significant role in shaping the market dynamics. These leading players often drive innovation within the market, introducing new products, technologies, and applications to meet evolving industry demands.

The transparent plastics sector is rapidly embracing advanced material sciences, with self‑healing polymers that autonomously repair surface scratches extending product lifespans and reducing maintenance costs. Concurrently, manufacturers are deploying blockchain‑enabled recycling platforms to trace feedstock provenance and certify recycled content, enhancing supply‑chain transparency and unlocking premium pricing for verifiable circular products. These convergent innovations are reshaping value propositions and driving investment into next‑generation resin technologies.

Stringent mandates under the EU Single‑Use Plastics Directive require 77% collection of plastic bottles by 2025 and a minimum of 25% recycled content in PET beverage containers from the same year. In July 2025, the European Commission’s consultation on chemically recycled content rules will standardize verification methodologies, fostering scale‑up of advanced recycling technologies and affording legal certainty to investors. Together, these regulatory drivers are compelling brand‑owners and converters to reconfigure formulations and adopt certified recycling streams to maintain market access.

Polymer Type Insights

Polyethylene terephthalate (PET) dominated the market, accounting for a share of 31.57% in 2024 and is expected to grow at a CAGR of 6.1% from 2025 to 2033. Surging demand for sustainable beverage packaging underpins PET’s dominance, as brand owners shift toward lightweight, fully recyclable containers to meet circular economy targets.

Its proven barrier properties and compatibility with high‑speed filling lines deliver operational efficiencies and lower carbon footprints. Innovation in mono‑material PET trays and thermoforming solutions further cements its cost‑effective appeal for both food and non‑food applications.

The polymethyl methacrylate (PMMA) segment is anticipated to grow at the fastest CAGR of 7.3% through the forecast period. Rapid uptake of energy‑efficient LED lighting and architectural glazing drives PMMA’s exceptional growth, thanks to its superior light transmittance and weather resistance.

OEMs in the automotive and signage industries increasingly specify PMMA for headlamp covers and display panels to enhance design flexibility and durability. Ongoing material enhancements that improve scratch resistance and UV stability are accelerating adoption in specialty markets.

Form Insights

The rigid segment dominated the market, accounting for a share of 69.02% in 2024 and is anticipated to grow at a CAGR of 6.2% over the forecast period. Robust demand for clear, crash‑worthy automotive components and durable electronic housing propels the rigid segment to both the largest and fastest positions.

Manufacturers benefit from their structural integrity and dimensional stability, which reduces defects and rework in high‑precision molding processes. Furthermore, regulatory mandates for lightweight safety materials in transportation continue to prioritize rigid plastics over metal and glass alternatives.

The flexible segment is expected to grow at a significant CAGR of 5.0% through the forecast period. Growth in flexible films and sheets is being fueled by the rise of wearable technology and advanced packaging formats.

Companies are leveraging transparent, stretchable polymers in smart textiles and barrier laminates to balance user comfort with product protection. Enhanced formability and lower material consumption in roll‑to‑roll processing enable rapid scale‑up, bolstering cost efficiency for emerging applications.

Application Insights

Packaging led the market, accounting for a share of 37.93% in 2024 and is expected to grow at a CAGR of 5.6% through the forecast period. The broader shift toward premium retail experiences and online grocery channels is driving packaging to remain the largest application.

Transparent plastics empower brands to showcase product integrity while offering tamper‑evident features that build consumer trust. Simultaneously, investments in lightweight, mono‑material solutions reduce freight expenses and simplify recycling streams, appealing to both retailers and sustainability‑focused regulators.

The medical & healthcare segment is expected to expand at a substantial CAGR of 7.4% over the forecast period. Expanding requirements for single‑use diagnostic devices and sterile packaging are accelerating transparent plastics in medical markets.

Clarity is critical for visual inspection in fluid management systems and sample collection kits, prompting healthcare OEMs to favor polymers with proven biocompatibility and gamma‑sterilization resistance. Ongoing collaborations between resin suppliers and medical device manufacturers are unlocking novel formulations that meet stringent regulatory standards while improving patient safety.

Regional Insights

Asia Pacific transparent plastics market held the largest share of 43.52% in 2024. Environmental regulations and financial incentives across China, Japan, South Korea, and India are accelerating the uptake of CO₂‑based and bio‑sourced transparent polymers. Public‑private partnerships and R&D consortia are scaling up carbon capture utilization (CCU) technologies to produce low‑carbon resins, while booming consumer electronics and packaging sectors drive volume growth. The region’s holistic policy frameworks and investment in sustainable feedstock position it as the fastest‑growing transparent plastics market.

China Transparent Plastics Market Trends

China transparent plastics market is underpinned by its vast electronics and electric vehicle industries. OEMs specify clear polycarbonate and PMMA for lightweight display covers, headlamps and interior trim to improve energy efficiency and design flexibility. Concurrent infrastructure expansion-ranging from smart glazing in high‑rise buildings to clear plastic barriers in public transit-further cements domestic demand for advanced transparent resin grades.

North America Transparent Plastics Market Trends

The transparent plastics market in North America is driven by robust investments in chemical recycling infrastructure and stringent corporate sustainability targets. Leading converters are adopting next‑generation depolymerization techniques to meet regional circular economy goals while satisfying growing demand from the medical device and pharmaceutical packaging sectors. The recent rebound in U.S. residential construction is also fueling the use of polycarbonate and acrylic glazing for energy‑efficient windows, and Canada’s cold‑weather automotive components increasingly rely on impact‑resistant clear polymers.

The transparent plastics market in the U.S. is driven by the expansion of healthcare facilities and outpatient clinics, which is creating a surge in demand for high‑clarity, biocompatible plastics in diagnostic kits and surgical trays. Meanwhile, accelerated residential and commercial building activity is driving transparent polymer use in lightweight window systems and interior partitions. As of 2025, the American Hospital Association reports over 6,100 hospitals and 919,000 active construction sites, underscoring the sector’s role as a key growth engine for transparent plastics.

Europe Transparent Plastics Market Trends

The transparent plastics market in Europe is shaped by aggressive circularity mandates, including the EU’s requirement for 25% recycled content in PET bottles by 2025. Governments are subsidizing AI‑driven sorting and advanced recycling facilities, enabling converters to supply certified recycled‑content grades for automotive headlamps and architectural façade systems. This policy‑backed momentum is complemented by rising demand for sustainable materials in high‑end packaging and electronics applications.

Key Transparent Plastics Company Insights

Key players operating in the transparent plastics market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth.

Key Transparent Plastics Companies:

The following are the leading companies in the transparent plastics market. These companies collectively hold the largest market share and dictate industry trends.

- Dow, Inc.

- SABIC

- BASF SE

- Covestro AG

- PPG Industries, Inc.

- LyondellBasell Industries N.V.

- DuPont de Nemours, Inc.

- INEOS Group Limited

- LANXESS AG

- Berry Global

- Cosmo Films

- Amcor plc

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Dow, Inc.; SABIC; BASF SE

- Broad portfolios of transparent engineering plastics, packaging films, specialty resins, and optical-grade polymer solutions across packaging, healthcare, automotive, and electronics applications.

- Significant investment in recyclable transparent materials, lightweight glazing systems, and advanced polymer engineering technologies.

- Integrated manufacturing infrastructure and global supply capabilities supporting high-volume industrial demand.

- Strong polymer science expertise and advanced transparent material engineering capabilities.

- Established global manufacturing footprint and diversified end-use penetration.

- Large-scale production capabilities improve operational efficiency and supply reliability.

- High exposure to petrochemical feedstock and energy price volatility.

- Significant sustainability-related investment and regulatory compliance requirements.

- Dependence on packaging and consumer electronics demand cycles affects market stability.

Emerging Players: Berry Global; Cosmo Films

- Focus on specialty transparent films, flexible packaging solutions, and high-clarity industrial applications.

- Expansion into sustainable packaging technologies, recyclable film systems, and premium consumer packaging materials.

- Flexible manufacturing strategies supporting regional packaging and industrial demand requirements.

- Greater flexibility in specialty packaging and transparent film development.

- Strong positioning in high-clarity flexible packaging and industrial film applications.

- Faster responsiveness to evolving customer requirements and sustainability trends.

- Smaller integrated petrochemical and resin production capabilities compared with multinational polymer producers.

- Limited economies of scale in specialty raw material procurement and global distribution.

- Higher dependence on regional packaging and consumer goods demand conditions.

Recent Developments

-

In May 2024, Dow and SCG Chemicals (SCGC) signed a memorandum of understanding (MOU) to create a circularity partnership in the Asia Pacific region aimed at transforming 200,000 tons per annum (KTA) of plastic waste into circular products by 2030. The agreement focused on advancing technologies for both mechanical and advanced recycling to convert a broader range of plastic waste into high-value applications.

-

In March 2025, the Philippines launched the National Plastic Action Partnership (NPAP), to tackle its growing plastic waste crisis and promote a circular economy. Led by the Department of Environment and Natural Resources (DENR), NPAP united the government, private sector, civil society, academia, and development partners to develop inclusive, collaborative solutions to reduce the country's annual 2.7 million metric tons of plastic waste, a significant portion of which pollutes oceans.

Transparent Plastics Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 139.45 billion

Revenue forecast in 2033

USD 219.17 billion

Growth rate

CAGR of 5.8% from 2025 to 2033

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Volume in kilotons; revenue in USD million/billion, and CAGR from 2025 to 2033

Report coverage

Volume & revenue forecast, competitive landscape, growth factors, and trends

Segmentation covered

Polymer type, form, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S., Canada; Mexico; Germany; UK; France; Italy; Spain, China; India; Japan; South Korea, Australia Brazil; Argentina, Saudi Arabia, South Africa, UAE

Key companies profiled

Dow, Inc.; SABIC; BASF SE; Covestro AG; PPG Industries, Inc.; LyondellBasell Industries N.V.; DuPont de Nemours, Inc.; INEOS Group Limited; LANXESS AG; Berry Global; Cosmo Films; Amcor plc

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Transparent Plastics Market Report Segmentation

This report forecasts volume & revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global transparent plastics market report on the basis of polymer type, form, application, and region:

-

Polymer Type Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Polyethylene Terephthalate (PET)

-

Polyvinyl Chloride (PVC)

-

Polypropylene (PP)

-

Polystyrene (PS)

-

Polycarbonate (PC)

-

Polymethyl Methacrylate (PMMA)

-

Other Polymers

-

-

Form Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Rigid

-

Flexible

-

-

Applications Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Medical & Healthcare

-

Automotive

-

Consumer Goods

-

Packaging

-

Building & Construction

-

Electrical & Electronics

-

Other Applications

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Pricing Analysis

Delivered comprehensive pricing analysis for polycarbonate, acrylic, PET, transparent polypropylene, transparent films, and specialty optical plastics across major global regions. The study evaluated monomer pricing trends, energy cost impacts, regional supply-demand balances, production economics, logistics expenses, and downstream packaging and electronics demand fluctuations influencing transparent plastics pricing structures.

Supported procurement optimization and resin sourcing strategy development. Improved understanding of feedstock cost exposure, regional price variations, and profitability trends across transparent plastic categories. Assisted in supplier comparison, contract planning, and pricing risk management. Enabled proactive response to petrochemical market fluctuations and changing end-use demand conditions.

Competitive Benchmarking

Conducted detailed benchmarking analysis of leading transparent plastics manufacturers based on product portfolio breadth, production capacity, regional presence, technology capabilities, sustainability initiatives, end-use penetration, and strategic developments. The assessment compared company positioning across optical plastics, packaging films, automotive glazing materials, healthcare plastics, and specialty transparent polymer applications.

Supported competitive intelligence and strategic positioning analysis. Identified technology differentiation, operational strengths, and capability gaps among key market participants. Improved understanding of specialty transparent plastics positioning and regional manufacturing competitiveness. Enabled informed sourcing, partnership, and expansion planning decisions.

Cross-Segmentation

Delivered cross-segment analysis across polymer type, transparency grade, application, end-use industry, processing technology, and regional demand trends. The study evaluated interactions between premium packaging, medical devices, display technologies, automotive glazing systems, industrial films, recyclable transparent plastics, and specialty optical material applications.

Improved understanding of high-growth application intersections and premium-value transparent polymer opportunities. Supported product portfolio optimization and targeted commercialization planning. Enabled identification of emerging sustainability-driven demand combinations and advanced transparent material innovation opportunities across the transparent plastics value chain.

Frequently Asked Questions About This Report

The global transparent plastics market size was estimated at USD 132.54 billion in 2024 and is expected to reach USD 139.45 billion in 2025.

The global transparent plastics market is expected to grow at a compound annual growth rate (CAGR) of 5.8% from 2025 to 2033, reaching USD 219.17 billion in 2033.

Polyethylene terephthalate (PET) dominated the global transparent plastics market with a revenue share of 31.57% in 2024, owing to surging demand for sustainable beverage packaging as brand owners shift toward lightweight, fully recyclable containers to meet circular economy targets.

Some of the key players in the global transparent plastics market include Dow, Inc., SABIC, BASF SE, Covestro AG, PPG Industries, Inc., LyondellBasell Industries N.V., DuPont de Nemours, Inc., INEOS Group Limited, LANXESS AG, Berry Global, Cosmo Films, and Amcor plc

Key factors driving the global transparent plastics market are brands seeking clear, lightweight containers that showcase product quality and enhance shelf appeal.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins Research Team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Share this report with your colleague or friend.

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.