- Home

- »

- Next Generation Technologies

- »

-

Team Collaboration Software Market Size Report, 2026-2033GVR Report cover

![Team Collaboration Software Market (2026 - 2033)Report]()

Team Collaboration Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Deployment (Cloud, On-premise), By Software Type (Conferencing Software, Communication & Coordination Software), By Application (Retail, Healthcare, BFSI, IT & Telecom), By Region, And Segment Forecasts

Market Size, 2025

$40.2BMarket Estimate, 2026

$44.6BMarket Forecast, 2033

$85.2BCAGR, 2026–2033

9.7%Team Collaboration Software Market Summary

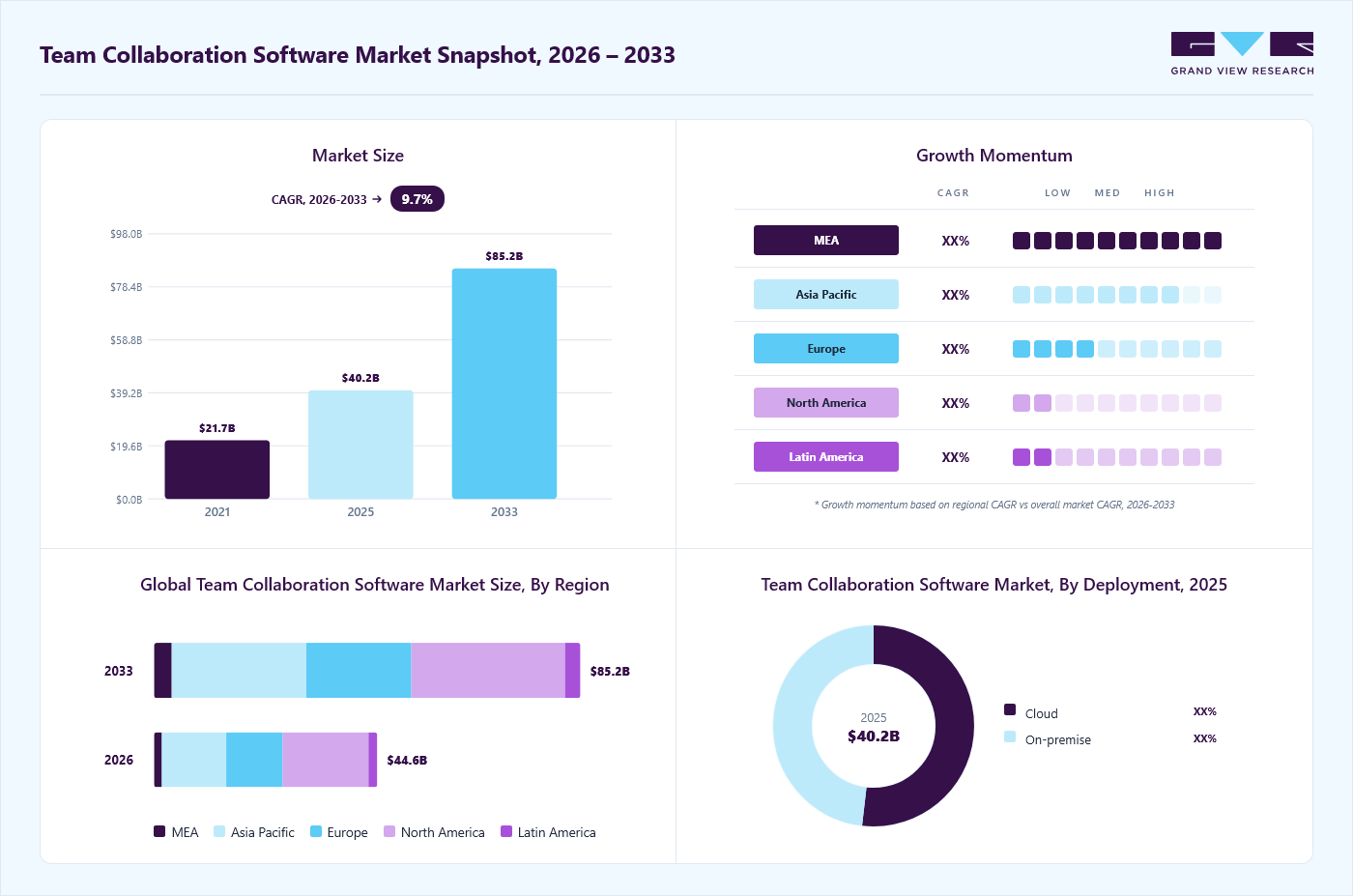

The global team collaboration software market size was valued at USD 40.2 billion in 2025 and is projected to grow from USD 44.6 billion in 2026 to USD 85.2 billion by 2033, at a CAGR of 9.7% from 2026 to 2033. North America dominated the global market with the largest revenue share of 38.8% in 2025. The growing shift toward unified digital workspaces is enabling remote and hybrid teams to collaborate more efficiently, with rising demand for real-time communication, document sharing, and integrated project management tools.

Key Market Trends & Insights

- By deployment: Cloud segment dominated the market, with a revenue share of 51.8% in 2025.

- By software type: Communication & Coordination Software segment held the largest revenue share in 2025.

- By application: IT &Telecom segment held the largest market share of 23.1% in 2025.

Regional Highlights

- Largest regional market: North America (38.8% revenue share, 2025)

- Fastest growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The team collaboration software market in the U.S. held the largest share in the North America region in 2025.

Market Size & Forecast

- Market size in 2025: USD 40.2 Billion

- Estimated market size in 2026: USD 44.6 Billion

- Projected market size by 2033: USD 85.2 Billion

- CAGR (2026-2033): 9.7%

The global team collaboration software market is experiencing increasing integration of artificial intelligence (AI) capabilities across collaboration platforms. AI-powered features such as automated task management, meeting summaries, and intelligent workflow recommendations are improving workplace productivity and efficiency. Organizations are adopting these solutions to streamline communication, reduce manual effort, and enhance team coordination across distributed work environments.")

The rise of AI-powered and automated features is transforming the team collaboration software market as organizations seek smarter, more efficient ways to work together. Collaboration platforms are embedding AI for automated meeting transcription and summarization, intelligent task assignment, and real-time language translation, while workflow automation tools streamline routine processes such as document approvals, notifications, and status updates without manual intervention. These capabilities reduce administrative overhead, accelerate decision‑making, and surface predictive insights on team performance. As businesses increasingly demand data-driven collaboration and hands-free task orchestration, AI and automation are reshaping the team collaboration software industry.

Additionally, the accelerating shift to hybrid and remote work models is a pivotal driver of market growth, as organizations seek unified platforms that support video conferencing, instant messaging, and shared workspaces across distributed teams. There is a rising emphasis on API integrations and workflow automation with HR systems enabling businesses to streamline operations, reduce manual tasks, and centralize data management. The adoption of AI-powered bots and low-code connectors is also gaining momentum, allowing companies to tailor workflows to dynamic business needs.

Furthermore, the integration of AI‑powered productivity and analytics features into collaboration suites, enabling smarter teamwork and data driven decision making. AI assistants automate task assignments, meeting summaries, and workflow optimizations, while built‑in analytics dashboards track team performance and project milestones in real time. These intelligent insights help managers identify bottlenecks, forecast resource needs, and streamline processes. As organizations seek more proactive, insight driven collaboration, demand for AI-enhanced team collaboration software continues to accelerate team collaboration software industry growth.

Moreover, the rising emphasis on seamless cross-platform interoperability is reshaping the market. Organizations now demand solutions that effortlessly integrate chat, video conferencing, file sharing, and task management across disparate tools and devices. Collaboration platforms are evolving to offer open APIs, prebuilt connectors, and unified interfaces that bridge legacy systems, SaaS applications, and on-premises infrastructure. This trend toward a cohesive digital workspace enhances user adoption, streamlines workflows, and reduces tool expansion. This shift drives higher adoption rates and propels the team collaboration software market expansion.

Market Dynamics

The global team collaboration software market is evolving with the growing integration of artificial intelligence into collaboration platforms. AI-powered capabilities such as automated meeting summaries, intelligent search, and task recommendations are improving workplace efficiency and streamlining daily workflows. Organizations are increasingly seeking solutions that reduce manual effort and enhance productivity across distributed teams. Software providers are continuously expanding AI functionality to deliver more personalized and context-aware user experiences. This development is contributing to greater adoption of advanced collaboration tools across enterprises of all sizes.

The growing demand for real-time communication and collaboration tools is a significant driver of the team collaboration software market. Organizations increasingly require instant messaging, video conferencing, and collaborative workspaces to support efficient communication among employees. Real-time collaboration enables teams to share information quickly, coordinate tasks effectively, and respond faster to business requirements. As workforces become more distributed, businesses are seeking platforms that facilitate seamless interactions regardless of employee location. Team collaboration software helps reduce communication delays and improves overall operational efficiency. This increasing reliance on instant and connected communication is supporting market growth across various industries.

The adoption of real-time collaboration tools is also helping organizations enhance productivity and decision-making processes. Employees can collaborate on documents, projects, and workflows simultaneously, reducing project completion times and improving transparency. These capabilities are particularly valuable for organizations managing cross-functional teams and global operations. Integration with communication channels, file-sharing applications, and business software further strengthens the value proposition of collaboration platforms. Enterprises are investing in advanced collaboration solutions to maintain workforce connectivity and support dynamic business environments.

User adoption and change management challenges act as a notable restraint for the team collaboration software market. Many employees are accustomed to traditional communication methods and may be reluctant to transition to new digital collaboration platforms. Resistance to change can reduce platform utilization and limit the expected productivity benefits. Organizations often need to invest in training programs and awareness initiatives to encourage adoption. The learning curve associated with advanced features can create difficulties for some users. These factors can slow implementation success and affect return on investment.

The effectiveness of collaboration software depends heavily on consistent usage across teams and departments. Inadequate user engagement can result in fragmented communication and underutilization of platform capabilities. Organizations may face challenges in establishing standardized workflows and collaboration practices. Differences in digital skills among employees can further complicate adoption efforts. Continuous support and change management strategies are often required to maintain long-term engagement. Consequently, user adoption barriers can hinder the full realization of collaboration software benefits and impact market growth.

The increasing adoption of team collaboration software among small and medium-sized enterprises (SMEs) presents a significant growth opportunity for the market. SMEs are increasingly recognizing the importance of digital collaboration tools to improve communication, project coordination, and operational efficiency. Cloud-based deployment models have made these solutions more affordable and accessible, reducing the need for extensive IT infrastructure. Subscription-based pricing options further enable SMEs to implement collaboration platforms according to their business requirements and budgets. As digital transformation initiatives expand across smaller businesses, demand for collaboration software is expected to increase. This trend is creating new revenue opportunities for software providers across emerging and developed markets.

Many SMEs are seeking scalable solutions that can support business growth and workforce expansion without substantial upfront investments. Team collaboration software helps these organizations streamline workflows, improve employee productivity, and enhance customer responsiveness. The growing use of remote and hybrid work arrangements among SMEs is further encouraging software adoption. Vendors are introducing simplified and industry-specific solutions to address the unique needs of smaller businesses. Increasing awareness of the benefits of digital workplace tools is supporting wider market penetration.

Market Concentration & Characteristics

The team collaboration software market exhibits a moderately concentrated structure, with a limited number of large vendors accounting for a substantial share of global market revenue. Major providers benefit from extensive customer bases, comprehensive product portfolios, and strong integration capabilities that support enterprise-wide deployments. Their platforms often serve as central hubs for communication, document sharing, workflow management, and virtual meetings. Significant investments in product development, cloud infrastructure, and ecosystem expansion have strengthened their market positions. These advantages create barriers for smaller vendors seeking to compete at scale.

Despite the influence of leading vendors, the market remains open to competition from numerous specialized software providers. Organizations often have diverse collaboration requirements that create opportunities for vendors offering industry-specific or feature-focused solutions. Smaller companies compete by addressing niche use cases, delivering customized functionality, or targeting underserved customer segments. Continuous innovation in areas such as workflow automation, employee engagement, and collaborative work management supports market participation from emerging providers. The availability of cloud-based software delivery models has also reduced entry barriers for new market participants.

Analyst Perspective

The global team collaboration software market remains highly attractive due to the increasing importance of digital workplace ecosystems and enterprise productivity solutions. Competition is expected to intensify as vendors expand platform capabilities and pursue deeper integration with broader business application environments. Market consolidation through partnerships and acquisitions is likely as providers seek to strengthen their customer reach and technology portfolios. Subscription-based business models and recurring revenue streams continue to enhance the market's long-term commercial potential. Over the forecast period, vendors that successfully balance innovation, security, and user experience are expected to gain a stronger competitive position.

Deployment Insights

Based on deployment, the cloud segment led the market with the largest revenue share of 51.8% in 2025. This growth is driven by enterprises seeking more control over their data and infrastructure, as on-premises solutions offer enhanced security, customization, and compliance capabilities. Companies in industries such as healthcare, finance, and government, where data privacy is critical, are increasingly opting for on-premises deployments to ensure tighter control over sensitive information while still benefiting from advanced collaboration features.

The cloud segment is expected to witness the highest CAGR of over 11% from 2026 to 2033, owing to the increasing demand for cloud-based platforms for effective team collaboration across enterprises, considering the rising number of people working remotely. Besides, these cloud platforms offer flexibility to access collaborative tools through smartphones. They also come with enriched features, including the capability of recording events to help review the proceedings later, thereby solidifying the dominance of this segment.

Software Type Insights

Based on software type, the communication & coordination software segment led the market with the largest revenue share of 54.6% in 2025. The widespread adoption of the Software as a Service (SaaS) model continues to transform how organizations implement and scale collaboration tools. SaaS-based solutions enable rapid deployment, lower dependency on internal IT infrastructure, and support continuous updates and innovation. This shift is enhancing the performance and reliability of team collaboration platforms, reducing latency, minimizing system downtime, and ensuring seamless communication and coordination across devices and geographies. As hybrid and distributed work environments become the norm, these trends are reinforcing the dominance of communication & coordination software in the market.

The conferencing software segment is expected to witness the fastest growth from 2026 to 2033, driven by the growing reliance on web conferencing as a primary mode of communication in modern organizations. A key trend is the widespread adoption of platforms like Microsoft Teams and Google Workspace, which have become essential tools for hosting virtual meetings and fostering collaboration. These solutions are at the forefront of workplace digital transformation, enabling real-time, organization-wide communication and enhancing productivity in remote and hybrid environments. The continued evolution of virtual meeting technologies and integration with broader collaboration ecosystems further drives this continued expansion.

Application Insights

Based on application, the IT &Telecom segment led the market with the largest revenue share of 23.1% in 2025, owing to robust unified‑communications platforms that leverage high-speed networks, 5G connectivity, and edge‑computing capabilities to enable real-time voice, video, and data collaboration. Integrated IoT device management and secure network orchestration streamline field‑service workflows and interdepartmental coordination, enhancing operational efficiency and driving continued demand across telecom carriers and enterprise IT organizations.

The healthcare segment is expected to grow at the highest CAGR from 2026 to 2033, driven by emerging trends in real-time data sharing and the growing need for connected, collaborative environments. Healthcare providers are increasingly adopting team collaboration software to enhance employee engagement and facilitate the seamless exchange of updates, feedback, and ideas across departments and facilities.

Regional Insights

North America dominated the Team Collaboration Software market with the largest revenue share of 38.8% in 2025, primarily driven by the region’s focus on rapid adoption of web conferencing solutions and collaboration portals by enterprises in the region. Moreover, easy access to high-speed internet is necessary for operating remote work models is expected to support the growth prospects of the regional market.

U.S. Team Collaboration Software Market Trends

The team collaboration software market in the U.S. held the largest share in the North America region in 2025, fueled by a relentless drive for innovation and digital modernization. The booming startup ecosystem, coupled with legacy enterprises accelerating cloud migrations and adopting agile workflows, is amplifying demand for unified collaboration platforms. Enhanced investment in remotework infrastructure and a growing emphasis on employee productivity tools further solidify the U.S. as a leading growth market.

Europe Team Collaboration Software Market Trends

Europe team collaboration software market is expected to grow at a CAGR of over 7% from 2026 to 2033, driven by a strong focus on digital transformation across both large enterprises and small-to-medium businesses. The shift towards remote and hybrid work models, especially post-pandemic, is driving the demand for advanced collaboration tools that facilitate seamless communication and productivity in the team collaboration software industry.

The U.K. product engineering services market is expected to experience the fastest growth in the coming years. The country benefits from a highly developed digital infrastructure and a strong focus on remote work adoption and hybrid working models. The U.K.'s advanced technology sectors, including finance, healthcare, and education, drive the demand for innovative team collaboration solutions that enhance productivity, streamline communication, and ensure seamless collaboration across geographically dispersed teams. As organizations in the U.K. increasingly prioritize digital transformation, the need for secure, scalable, and feature-rich collaboration platforms is intensifying, further driving market expansion.

The Germany team collaboration software market is fueled by the country’s strong industrial sectors, particularly manufacturing, automotive, and technology, which continue to drive the demand for advanced communication and collaboration tools. Additionally, Germany’s focus on digitalization and Industry 4.0 is pushing businesses to adopt integrated collaboration platforms that support remote work and seamless communication across geographically dispersed teams. This trend is creating significant opportunities for the market to evolve, providing solutions that enhance productivity, streamline workflows, and meet the growing demand for flexible and secure collaboration in the workplace.

Asia Pacific Team Collaboration Software Market Trends

The Asia Pacific team collaboration software market is expected to grow at a CAGR of over 8% from 2026 to 2033, driven by the ongoing digitization of businesses and the development of high-speed internet infrastructure in the region. Such developments are encouraging organizations to incorporate team collaboration software to optimize their workforce and facilitate effective interaction among employees. This demand for flexible, scalable solutions is further driving the need for customized collaboration platforms that cater to unique industry requirements, resulting in higher adoption rates across diverse sectors.Top of FormBottom of Form

The Japan team collaboration software market is gaining traction fueled by its technological innovation, particularly in sectors such as automotive, robotics, and electronics. The country’s strong focus on digital transformation, efficiency, and advanced automation drives the demand for specialized collaboration platforms that can enhance team productivity, streamline workflows, and improve communication across industries. Japan's emphasis on remote work solutions, coupled with its aging population, has also increased the need for intuitive, user-friendly software that supports accessibility and caters to diverse workforce needs, further boosting demand for personalized and innovative collaboration tools.

The China team collaboration software market is rapidly expanding. China’s focus on digital transformation and the growing adoption of remote and hybrid work models are significant drivers of the market. The government’s emphasis on technological innovation and digital infrastructure, combined with the push for smart cities, is accelerating the demand for advanced collaboration solutions. Additionally, efforts to improve data security and meet international standards are fostering market growth.

Key Team Collaboration Software Company Insights

Some of the key players operating in the market include Adobe and Cisco Systems, Inc.

-

Adobe has broadened its collaboration portfolio by embedding real-time co-editing and actionable review workflows across its Document Cloud and Creative Cloud platforms. By unifying seamless asset sharing with enterprise-grade security controls such as permissions management, audit trails, and encrypted cloud storage. Adobe enables cross-functional teams to iterate on content and documentation more efficiently. These enhancements position Adobe as a preferred collaboration solution for organizations prioritizing design excellence and secure, compliant workflows.

-

Cisco Systems, Inc. is a technology company providing services in networking, security, and collaboration solutions. Within the market, Cisco’s Webex suite offers a comprehensive platform that includes Webex Huddle for persistent virtual workspaces, Webex Desk Pro for integrated video and whiteboarding, and AI-driven noise suppression to enhance meeting quality. These tools enable seamless synchronization of whiteboards, files, and chat threads across meetings and channels, empowering organizations to streamline communication, boost productivity, and support hybrid work models

Zoom Video Communications, Inc. and Slack Technologies, LLC are some of the emerging market participants in the team collaboration software market.

-

Zoom Video Communications, Inc. delivers a unified collaboration platform that combines persistent messaging channels, advanced whiteboarding, and voice services. Zoom Workplace integrates persistent channels with Whiteboard 2.0,featuring AI-powered diagram recognition to facilitate ideation and visual collaboration. Coupled with integrated Zoom Phone archiving, the platform ensures seamless transitions between chat, voice, and collaborative sketching, empowering teams to maintain continuity and boost productivity in both hybrid and distributed work environments.

-

Slack Technologies, LLC is a provider of enterprise collaboration solutions, specializing in real-time messaging and workflow integration. Its enhanced “Threads+” feature organizes conversations into deep, nested discussions, while AI-driven summarization distills key points and action items automatically. With a broad ecosystem of app‑directory integrations and cross-workspace linking, Slack enables organizations to reduce email dependency, centralize operational notifications, and streamline team communications across disparate departments.

Key Team Collaboration Software Companies:

The following key companies have been profiled for this study on the team collaboration software market.

-

Adobe

-

Asana, Inc.

-

Avaya Inc.

-

AT&T, Inc.

-

Blackboard, Inc.

-

Cisco Systems, Inc.

-

Citrix Systems, Inc.

-

Google LLC

-

IBM Corporation

-

Microsoft

-

OpenText Corporation

-

Oracle

-

Slack Technologies, LLC

-

Zoom Video Communications, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Microsoft, Google LLC, Cisco Systems, Inc., Oracle, IBM Corporation

- Focus on ecosystem expansion, AI integration, enterprise customer retention, strategic acquisitions, and cross-platform integration.

- Large customer base, strong brand recognition, extensive partner ecosystems, broad product portfolios, and advanced security and compliance capabilities.

- Complex product ecosystems, slower feature rollout cycles, higher pricing, and challenges in maintaining platform flexibility.

Emerging Players: Zoom Video Communications, Inc., Asana, Inc., Slack Technologies, LLC

- Focus on product innovation, niche market targeting, competitive pricing, user experience enhancement, and customer acquisition.

- Greater agility, faster innovation cycles, specialized features, flexible deployment options, and stronger focus on user experience.

- Limited brand recognition, smaller customer base, fewer integration capabilities, and lower financial and operational resources.

Recent Developments

-

In April 2025, AT&T, Inc. expanded its Network Edge Collaboration service by integrating private 5G technology to enable ultra-low‑latency video conferencing and secure field‑site file sharing. This new initiative enhances the collaboration experience by offering faster, more reliable connections for remote teams, improving communication in high-demand environments. Through this upgrade, AT&T aims to support industries with greater security, efficiency, and real-time collaboration capabilities, further driving the growth of its enterprise-focused communication solutions.

-

In March 2025, Adobe announced a strategic collaboration with Amazon Web Services (AWS) aimed at enhancing its customer experience offerings. The collaboration, effective immediately, combines Adobe's expertise in Customer Experience Orchestration with AWS's advanced cloud services. This partnership is designed to help marketing and creative teams deliver customer experiences more quickly, precisely, and at scale, empowering businesses to meet the demands of the digital era better.

-

In March 2025, Cisco Systems, Inc. launched Webex Huddle, a persistent virtual workspace designed to automatically sync whiteboard sketches, files, and chat threads across meetings and channels. This new initiative enhances collaboration by offering seamless integration and real‑time updates, allowing teams to maintain continuity across discussions. With this update, Cisco aims to streamline communication, improve workflow efficiency, and provide a more cohesive experience for hybrid teams, further strengthening its position in the team collaboration software market.

Team Collaboration Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 40.2 billion

Market size value in 2026

USD 44.6 billion

Revenue forecast in 2033

USD 85.2 billion

Growth rate

CAGR of 9.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Deployment, software type, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S., Canada, Mexico, U.K., Germany, France, China, Japan, India, South Korea, Australia, Brazil, KSA, UAE, South Africa

Key companies profiled

Adobe; Asana, Inc.; Avaya Inc.; AT&T, Inc.; Blackboard, Inc.; Cisco Systems, Inc.; Citrix Systems, Inc.; Google LLC; IBM Corporation; Microsoft; OpenText Corporation; Oracle; Slack Technologies, LLC; Zoom Video Communications, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Team Collaboration Software Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest technological trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the team collaboration software market report based on deployment, software type, application, and region:

-

Team Collaboration Software Market Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud

-

On-premise

-

-

Team Collaboration Software Market Software Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Conferencing Software

-

Communication & Coordination Software

-

-

Team Collaboration Software Market Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Manufacturing

-

BFSI

-

IT & Telecom

-

Retail

-

Healthcare

-

Logistics & Transportation

-

Education

-

-

Team Collaboration Software Market Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa

-

UAE

-

KSA

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Deployment

Revenue capture definition

Cloud

This segment includes revenue derived from team collaboration software accessed through cloud-hosted environments. Revenue is generated through subscription plans and covers platform usage, communication features, collaboration tools, storage capabilities, software updates, technical support, and other services provided through the cloud.

On-premise

This segment comprises revenue earned from team collaboration software deployed within an organization's internal IT infrastructure. Revenue sources include perpetual or term-based software licenses, implementation and customization services, maintenance agreements, upgrades, training, and support services required for on-premise deployments.

Segment - Software Type

Revenue capture definition

Conferencing Software

This category captures revenue generated from software solutions designed to facilitate virtual meetings, video conferencing, webinars, and online presentations. Revenue includes subscription fees, licensing charges, premium meeting features, webinar hosting capabilities, recording services, and related support offerings.

Communication & Coordination Software

This category encompasses revenue derived from platforms that support team messaging, task coordination, project collaboration, file sharing, and workflow management. Revenue is generated through software subscriptions, user licenses, premium collaboration features, integration services, and associated maintenance and support offerings.

Segment - Application

Revenue capture definition

Manufacturing

This segment includes revenue generated from team collaboration software deployed by manufacturing organizations to support production planning, workforce coordination, project management, operational communication, and cross-functional collaboration across facilities and departments.

BFSI

This segment comprises revenue derived from team collaboration software utilized by banking, financial services, and insurance organizations for secure communication, document collaboration, workflow coordination, customer service management, and regulatory compliance activities.

IT & Telecom

This segment captures revenue generated from collaboration software adopted by information technology and telecommunications companies to facilitate project execution, software development coordination, team communication, knowledge sharing, and service management operations.

Retail

This segment includes revenue earned from collaboration platforms used by retail organizations for store coordination, inventory management communication, workforce collaboration, supplier engagement, and operational planning activities.

Healthcare

This segment encompasses revenue derived from team collaboration software implemented by healthcare providers and related organizations to support staff communication, care coordination, administrative workflows, document sharing, and operational management.

Logistics & Transportation

This segment captures revenue generated from collaboration solutions used within logistics and transportation organizations for fleet coordination, shipment management communication, workforce collaboration, route planning discussions, and supply chain operations management.

Education

This segment includes revenue earned from team collaboration software utilized by educational institutions and training organizations to facilitate communication, virtual learning support, administrative coordination, content sharing, and collaborative academic activities.

Estimation Model

Layer Name

Key Questions

Description

Workforce Digitalization Layer

Who requires collaboration solutions?

Identify organizations and employees that require digital communication, project coordination, document sharing, and workflow management capabilities. This layer establishes the total addressable demand for team collaboration software across industries and enterprise sizes.

Collaboration Software Adoption Layer

Who is adopting collaboration platforms?

Apply adoption rates for digital workplace and collaboration solutions across enterprises and SMEs. This layer estimates the active user base utilizing team collaboration software for business operations and workforce connectivity.

Platform Deployment Layer

Which collaboration solutions are being deployed?

Apply penetration rates across deployment models, software types, and end-user industries. This layer captures the implementation of conferencing, communication, coordination, and workflow collaboration platforms within organizations.

Revenue Generation Layer

How much revenue is generated?

Multiply deployed software subscriptions, licenses, and service contracts by their respective average revenue values. This layer estimates total market revenue generated from software subscriptions, implementation services, maintenance, support, and related collaboration solutions

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Product Positioning & Competitive Intelligence

Feature benchmarking across leading collaboration platforms

Pricing model and subscription tier analysis

Integration ecosystem and interoperability assessment

Competitor strategy, market share, and product roadmap evaluationStrengthened product differentiation and positioning

Supported pricing and packaging optimization

Identified competitive gaps and feature enhancement opportunities

Improved market competitiveness and customer acquisition strategiesTechnology & Innovation Assessment

AI, automation, and workflow innovation analysis

Emerging technology adoption and readiness assessment

Product development and innovation pipeline evaluation

Partnership, integration, and ecosystem mappingIdentified future growth and innovation opportunities

Supported product roadmap and technology investment decisions

Evaluated commercialization potential of new capabilities

Enhanced partnership and ecosystem development strategiesCustomer & End-User Insights Study

User adoption and usage behavior analysis

Purchase decision process and software selection criteria assessment

Customer satisfaction, retention, and loyalty evaluation

Workflow challenges and unmet collaboration needs identificationRevealed key adoption drivers and barriers

Supported customer-centric product development initiatives

Improved customer engagement and retention strategies

Identified upselling, cross-selling, and market expansion opportunitiesFrequently Asked Questions About This Report

The global team collaboration software market size was estimated at USD 36,114.2 million in 2024 and is expected to reach USD 40,159.0 million in 2025.

The global team collaboration software market is expected to grow at a compound annual growth rate of 7.4% from 2025 to 2030 to reach USD 57,403.8 million by 2030.

Some key players operating in the global team collaboration software market include Adobe; Asana, Inc.; Avaya Inc.; AT&T, Inc.; Blackboard, Inc.; Cisco Systems, Inc.; Citrix Systems, Inc.; Google LLC; IBM Corporation; Microsoft; OpenText Corporation; Oracle; Slack Technologies, LLC; Zoom Video Communications, Inc.

The on-premise segment accounted for the largest share of over 50% in 2024. This growth is driven by enterprises seeking more control over their data and infrastructure, as on-premises solutions offer enhanced security, customization, and compliance capabilities.

The communication & coordination software segment accounted for the largest market share in 2024, owing to the widespread adoption of the Software as a Service (SaaS) model, which continues to transform how organizations implement and scale collaboration tools.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.