- Home

- »

- Plastics, Polymers & Resins

- »

-

Polymethyl Methacrylate Market Size & Share Report, 2033GVR Report cover

![Polymethyl Methacrylate (PMMA) Market (2026 - 2033)Report]()

Polymethyl Methacrylate (PMMA) Market (2026 - 2033)

Size, Share & Trends Analysis Report By Form (Extruded Sheet, Cast Acrylic Sheet, Pellets, Beads), By Grade (General Purpose grade, Optical Grade), By End-use (Automotive, Healthcare, Signs & Displays, Construction), By Region, And Segment Forecasts

Market Size, 2025

$6.2BMarket Estimate, 2026

$6.5BMarket Forecast, 2033

$10.0BCAGR, 2026–2033

6.4%Polymethyl Methacrylate Market Summary

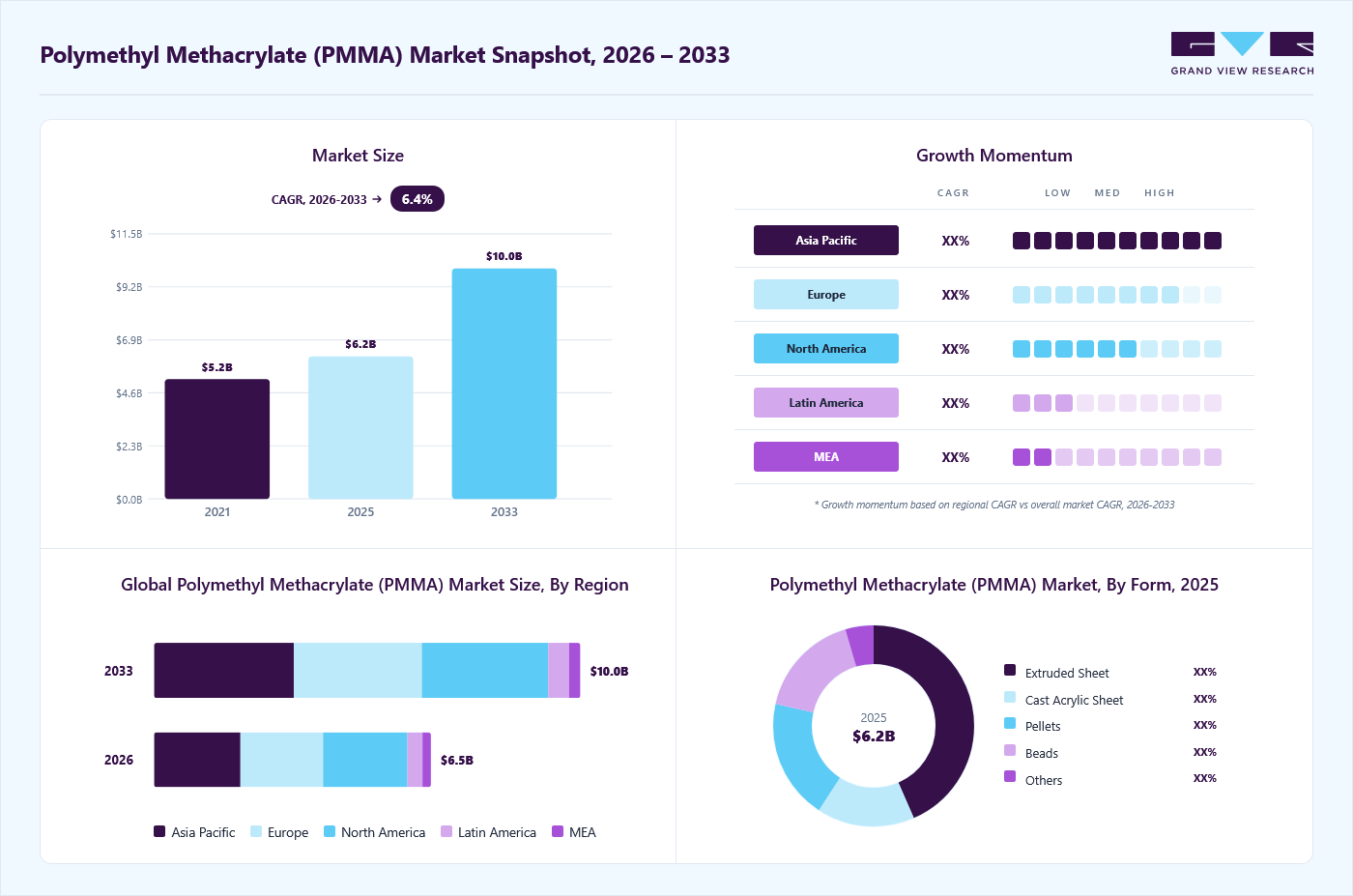

The global polymethyl methacrylate (PMMA) market size was valued at USD 6.0 billion in 2025 and is projected to grow from USD 6.5 billion in 2026 to USD 10.0 billion by 2033, at a CAGR of 6.4% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 31.0% in 2025. The increasing demand for lighter and more fuel-efficient vehicles in the automobile industry is one of the primary drivers for the growth of PMMA market.

Key Market Trends & Insights

- By form: the extruded sheet segment led the market with largest revenue share of 43.4% in 2025.

- By grade: the general-purpose grade segment led the market with the largest revenue share of 60.8% in 2025.

- By end-use: the signs & displays segment led the market with the largest revenue share of 32.6% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (31.0% revenue share, 2025)

- By country: The polymethyl methacrylate (PMMA) market in the China held the largest share in the Asia Pacific region in 2025.

Market Size & Forecast

- Market Size in 2025: USD 6.2 Billion

- Estimated Market Size in 2026: 6.5 Billion

- Projected Market Size by 2033: USD 10.0 Billion

- CAGR (2026-2033): 6.4%

The automotive and transportation industries have emerged as key growth drivers for the polymethyl methacrylate (PMMA) industry, primarily due to the increasing adoption of lightweight and durable materials aimed at improving fuel efficiency and design flexibility. PMMA, commonly known as acrylic or acrylic glass, is widely used in headlamps, taillights, dashboards, windshields, and interior trims as a substitute for glass and polycarbonate. Its superior optical clarity, UV resistance, and weatherability make it a preferred choice among automakers seeking materials that combine aesthetics with performance.As global automotive manufacturers transition toward electric vehicles (EVs) and energy-efficient mobility solutions, the demand for PMMA-based components is rising, given the material’s capability to reduce vehicle weight while maintaining safety and visibility standards.

")

Moreover, the trend toward electric and autonomous vehicles (EVs/AVs) is further accelerating PMMA usage in the transportation sector. PMMA is extensively employed in light-diffusing panels, illuminated logos, display screens, and advanced lighting systems that are integral to EV and AV designs. These applications benefit from PMMA’s high light transmittance and ease of molding into complex geometries, allowing for sleek and futuristic vehicle aesthetics.

The integration of advanced lighting systems, such as LED and OLED technologies, also complements PMMA’s optical properties, reinforcing its relevance in next-generation vehicle designs. As governments globally tighten emission standards and promote vehicle lightweighting through regulatory initiatives, PMMA is positioned as a critical enabler of sustainable automotive manufacturing.

In addition, PMMA’s recyclability and sustainability attributes contribute to its growing acceptance in the automotive industry, which is increasingly focusing on circular economy principles. Leading manufacturers are investing in the development of bio-based and recycled PMMA grades to meet OEM sustainability targets and regional environmental mandates, particularly in Europe and North America.

For instance, initiatives promoting eco-friendly acrylic sheets and resins have gained traction in line with stricter waste management directives. This evolution toward sustainable PMMA formulations is not only helping automakers meet regulatory compliance but also attracting eco-conscious consumers, thereby expanding the material’s market potential.

Market Dynamics

PMMA demand is anchored in optical clarity, weatherability, and lightweight substitution for glass, which supports steady consumption across signs and displays, lighting, automotive lighting, construction glazing, electronics, and medical parts. Revenue is typically captured through sheets, resins, and molding compounds, with premium value concentrated in optical and cast formats. Demand is structurally concentrated in Asia Pacific, North America, and Europe, by inference from downstream fabrication density and the global manufacturing footprint of leading suppliers. The commercial structure remains mixed, with integrated producers, sheet converters, and regional fabricators sharing volume, specification, and custom-order revenue.

The primary growth driver is the widening use of PMMA in applications where transparency, surface quality, and weather resistance directly influence product performance and brand presentation. Illuminated signs, retail displays, flat panel displays, lighting optics, automobile tail lights, and architectural glazing continue to support premium PMMA consumption because the material combines high light transmission with design flexibility. This keeps demand tied to sectors that value aesthetics, diffused lighting, and durable clarity rather than simple bulk substitution. In practice, PMMA is increasingly specified where end users want a glass-like appearance without the weight, breakage risk, or installation burden of mineral glass.

PMMA also benefits from continued product development in high-heat grades, color flexibility, and downstream customization, especially in automotive trim, lighting components, and premium display systems. Suppliers are using circularity and application-specific design to increase customer lock-in, since buyers in these segments prioritize optical consistency, ease of processing, and long service life. This supports value-led growth because specification depth, not only resin volume, determines supplier selection. As a result, producers with strong technical support, regional conversion capacity, and application engineering are better positioned to capture margin than commodity-oriented suppliers.

The main restraint is the persistent substitution pressure from lower-cost transparent alternatives, combined with margin compression in standard-grade sheet and resin supply. PMMA competes with polycarbonate, glass, and other transparent polymers in many end uses, which limits pricing power when performance requirements are moderate. At the same time, the market remains exposed to feedstock-linked cost swings because profitability depends on methyl methacrylate economics and conversion efficiency. This creates a structural squeeze in price-sensitive channels, where buyers can trade down quickly unless the PMMA supplier offers superior optical performance, fabrication support, or specialty grades.

A clear opportunity is the expansion of recycled and mass-balance PMMA into premium end uses. Chemical recycling can recover monomer quality that can re-enter automotive, lighting, and optical supply chains without material trade-offs, which strengthens the sustainability case for spec-driven buyers. This opens a route for producers to defend price premiums while meeting customer decarbonization targets and procurement requirements. The most attractive gains are likely to come from suppliers that pair circular feedstock with high-purity sheet, molding compound, and lighting-grade product lines.

Market Concentration & Characteristics

The polymethyl methacrylate (PMMA) industry exhibits cyclical growth patterns linked to macroeconomic and sectoral trends. Demand tends to fluctuate with the performance of construction and automotive industries, which together account for a substantial portion of global consumption. Regional growth dynamics are also notable, Asia Pacific dominates global production and consumption, driven by robust manufacturing infrastructure in China, Japan, and South Korea, while Europe and North America emphasize innovation and sustainable product development. Regulatory frameworks promoting recyclable and eco-friendly materials further influence industry evolution.

Industry Dynamics")

Technological advancement is another defining characteristic of the polymethyl methacrylate (PMMA) industry, particularly in the development of sustainable and high-performance grades. The industry is witnessing a shift toward bio-based PMMA and closed-loop recycling technologies to align with global sustainability goals. Manufacturers are also investing in the enhancement of optical and mechanical properties to expand PMMA’s usability in high-end applications such as LED lighting, electric vehicle components, and smart display technologies. The integration of nanotechnology and advanced polymer blending is further extending the performance boundaries of PMMA, enabling greater durability, scratch resistance, and environmental stability. Continuous R&D and patent innovation play a pivotal role in shaping competitive differentiation and market expansion.

Analyst Perspective

The PMMA market is moving from a broadly volume-led resin business toward a more segmented, value-led structure built on optical performance, circularity, and application engineering. Demand will continue to be anchored in signs and displays, lighting, automotive components, construction glazing, electronics, and healthcare, but winners will be those that can supply higher-purity grades, stable optical performance, and design-specific product formats. Sustainability will become a commercial filter rather than a branding add-on, especially where recycled content, monomer recovery, and lower-carbon supply chains can be proven. Competitive advantage will increasingly depend on vertical integration, regional conversion capacity, technical support, and partnerships with fabricators and downstream brands. Margin pressure will remain material because of substitution risk, raw material volatility, and intense price competition in standard grades, so the strongest players will be those able to differentiate beyond resin supply and into solution-led specification.

Form Insights

Based on form, the extruded sheet segment led the market with the largest revenue share of 43.4% in 2025. This outlook is due to its widespread use in signage, display panels, lighting fixtures, and protective barriers. Its superior optical clarity, surface uniformity, and cost-effectiveness make it the preferred form of PMMA for large-scale applications. In addition, growing demand from the construction and retail sectors for durable and aesthetically appealing transparent materials continues to strengthen the dominance of extruded PMMA sheets in the market.

The cast acrylic sheet segment anticipated to grow at a significant CAGR during the forecast period, driven by its exceptional optical clarity, surface hardness, and weather resistance. Unlike extruded sheets, cast acrylic offers greater thickness flexibility and superior chemical resistance, making it ideal for aquariums, skylights, sanitary ware, and premium display applications. Its ability to maintain dimensional stability and visual quality under varying environmental conditions continues to support its demand across architectural and high-end industrial uses.

Grade Insights

Based on grade, the general purpose grade segment led the market with the largest revenue share of 60.7% in 2025. This dominance is attributed to its versatility, cost-effectiveness, and balanced performance across a wide range of applications, including signage, lighting, automotive components, and construction materials. The increasing adoption of PMMA in everyday products requiring optical transparency, UV resistance, and durability continues to drive strong growth in this segment globally.

The optical grade segment is anticipated to grow at a significant CAGR during the forecast period, driven by its superior light transmission, low haze, and excellent surface finish. It is extensively used in optical lenses, LED light covers, display screens, and automotive lighting systems, where high clarity and precision are critical. The growing demand for high-performance optical materials in electronics and automotive applications continues to fuel the expansion of this segment, supported by advancements in precision molding and optical-grade PMMA formulations.

End Use Insights

Based on end-use, the signs & displays segment led the market with the largest revenue share of 32.6% in 2025, driven by the extensive use of PMMA sheets in advertising panels, illuminated signage, point-of-sale displays, and retail branding applications. PMMA’s superior light diffusion, weather resistance, and surface gloss make it an ideal material for both indoor and outdoor display solutions. The rapid expansion of the retail and advertising sectors, coupled with increasing demand for visually appealing and durable promotional materials, continues to reinforce the dominance of this segment in the polymethyl methacrylate (PMMA) industry.

The automotive segment is projected to grow at the fastest CAGR of 7.2% during the forecast period, driven by the rising adoption of lightweight and durable materials aimed at improving fuel efficiency and design flexibility. PMMA is increasingly used in headlights, taillights, interior trims, and glazing applications due to its excellent optical clarity, surface hardness, and weather resistance. The growing production of electric and autonomous vehicles, along with the trend toward aesthetic vehicle design and energy efficiency, is expected to further accelerate the use of PMMA in the automotive sector.

Regional Insights

The polymethyl methacrylate (PMMA) market in North America held a significant share in 2024, supported by strong demand from the automotive, construction, and medical device industries. The region’s focus on sustainable materials, advanced manufacturing technologies, and high-quality optical applications has driven the adoption of PMMA across diverse end uses. In addition, the growing presence of electric vehicle production, architectural glazing projects, and healthcare innovations continues to boost PMMA consumption. Ongoing R&D investments and regulatory emphasis on recyclable and bio-based polymers are further expected to strengthen North America’s market growth over the forecast period.

U.S. Polymethyl Methacrylate Market Trends

The polymethyl methacrylate (PMMA) market in the U.S. dominated the North American PMMA market in 2024, driven by strong demand from the automotive, construction, and electronics industries. The country’s advanced manufacturing infrastructure and growing focus on lightweight, energy-efficient materials have accelerated PMMA adoption in applications such as vehicle lighting systems, architectural glazing, and LED displays. Moreover, increasing investments in sustainable polymer innovation and the expansion of medical and consumer electronics sectors are expected to further strengthen the U.S. position as a key contributor to regional market growth over the forecast period.

Asia Pacific Polymethyl Methacrylate Market Trends

Asia Pacific dominated the polymethyl methacrylate (PMMA) market with the largest revenue share of 31.0% in 2025. The region’s leadership is driven by rapid industrialization, strong manufacturing capabilities, and expanding end-use industries such as automotive, construction, electronics, and signage. Countries like China, Japan, South Korea, and India are major contributors, supported by rising infrastructure investments, growing consumer electronics production, and increasing demand for lightweight materials in transportation and packaging applications.

The polymethyl methacrylate (PMMA) market in the China held the largest share in the Asia Pacific region in 2025, driven by its robust manufacturing base and high consumption across automotive, construction, and electronics sectors. The country’s strong presence in LED lighting, display panels, and consumer electronics production continues to fuel demand for optical-grade PMMA. In addition, rapid urbanization and infrastructure expansion, coupled with increasing adoption of lightweight and energy-efficient materials, are expected to keep China at the forefront of regional market growth throughout the forecast period.

Europe Polymethyl Methacrylate Market Trends

The polymethyl methacrylate (PMMA) market in Europe is anticipated to grow at a significant CAGR during the forecast period. The region’s emphasis on sustainability, circular economy principles, and high-performance materials has driven the adoption of recyclable and bio-based PMMA grades. Countries such as Germany, France, and the UK are key contributors, benefiting from advanced manufacturing capabilities and the presence of leading PMMA producers such as Röhm GmbH and Trinseo. In addition, growing applications in LED lighting, solar panels, and architectural design continue to reinforce Europe’s position as a technologically advanced and environmentally conscious market for PMMA.

Key Polymethyl Methacrylate (PMMA) Company Insights

The competitive environment of the polymethyl methacrylate (PMMA) industry is characterized by moderate consolidation and high technological differentiation, with a few global players dominating resin production and a wide base of regional converters and compounders serving localized demand. Major companies such as Mitsubishi Chemical Group, Röhm GmbH, Chi Mei Corporation, Trinseo, and Sumitomo Chemical hold significant market shares through strong vertical integration, extensive product portfolios, and global distribution networks.

Competition is primarily driven by innovation in bio-based and recycled PMMA grades, product quality, and optical performance enhancements, alongside cost optimization strategies. While entry barriers remain high due to capital-intensive production and proprietary polymerization technologies, regional manufacturers in Asia-Pacific continue to intensify competition by offering cost-effective extruded and cast sheet solutions. Strategic alliances, R&D collaborations, and capacity expansions are increasingly shaping the market landscape as players aim to strengthen their sustainability credentials and meet rising global demand across automotive, electronics, and construction applications.

Key Polymethyl Methacrylate (PMMA) Companies:

The following are the leading companies in the polymethyl methacrylate (PMMA) market. These companies collectively hold the largest market share and dictate industry trends.

- Dymatic chemicals, Inc.

- SK Geo Centric Co. Ltd.

- LG Chem

- Mitsubishi Chemical Group

- CHIMEI

- Asahi Kasei Corporation

- SABIC

- LOTTE Chemical CORPORATION

- Röhm GmbH

- Trinseo

- Sumitomo Chemical Co., Ltd.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Avery Dennison Corporation, 3M, ORAFOL Europe GmbH, Fedrigoni S.P.A, LLumar)

Expand premium product lines through broad distribution, installer networks, and specification-led channel coverage.

Use partnerships and localized launches to protect visibility in major markets.

Invest in technical performance, sustainability, and application support to defend pricing.

Strong brand recognition and deeper market presence.

Broader distribution reach and better channel control.

Higher ability to fund R&D, compliance, and service infrastructure.

Slower response to niche local demand shifts.

Higher overhead in price-sensitive channels.

More exposed to margin pressure when products become commoditized.

Emerging Players (Arlon Graphics LLC, KPMF, Vvivid Vinyl, Hexis S.A.S, CARBINS Film)

Compete through niche positioning, product novelty, and localized commercial execution.

Target specific customer groups with tailored designs, finishes, and value pricing.

Build visibility through digital marketing, distributor ties, and installer relationships.

Faster product launches and shorter response cycles.

Better fit for niche or regional preferences.

More flexible commercial positioning than larger peers.

Lower scale and weaker bargaining power.

Limited ability to absorb pricing pressure.

Smaller budgets for validation, promotion, and geographic expansion.

Recent Developments

-

In December 2024, NEXTCHEM (MAIRE) signed a toll manufacturing agreement with Röhm to advance the chemical recycling of polymethyl methacrylate (PMMA) at MyRemono’s industrial-scale facility. This partnership leverages NEXTCHEM’s proprietary NXRe PMMA technology to enable efficient and sustainable recycling processes, supporting circular economy initiatives in the plastics industry.

-

In June 2024, Trinseo launched its PMMA depolymerization facility in Rho, Italy, advancing its circular economy strategy. Using EU-backed MMAtwo technology, the plant converts pre- and post-consumer PMMA waste into high-purity recycled MMA (rMMA), equivalent in quality to virgin material. This innovation enables recycling of previously hard-to-recycle PMMA types and supports sustainable production across mobility, construction, and consumer goods, aligning with Trinseo’s 2030 sustainability goals.

-

In February 2024, Röhm expanded its global PMMA capacity with a new energy-efficient production line and colored PMMA compounding facility in Worms, Germany, reducing its carbon footprint and supporting sustainability goals. The company also upgraded its Wallingford (U.S.) and Shanghai (China) plants to boost output and serve global markets. With facilities across Asia, Europe, and North America, Röhm reinforces its leadership in PLEXIGLAS molding compounds and advances its goal to become the world’s leading methacrylate producer.

Polymethyl Methacrylate (PMMA) Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 6.2 billion

Estimated Market Size in 2026

USD 6.5 billion

Projected Market Size by 2033

USD 10.0 billion

Growth rate

CAGR of 6.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Form, grade, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; China; India; Japan; South Korea; Southeast Asia; Brazil; Argentina; GCC Countries; South Africa

Key companies profiled

Dymatic Chemicals, Inc.; SK Geo Centric Co. Ltd.; LG Chem; Mitsubishi Chemical Group; CHIMEI; Asahi Kasei Corporation; SABIC; LOTTE Chemical Corporation; Röhm GmbH; Trinseo; Sumitomo Chemical Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Polymethyl Methacrylate (PMMA) Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global polymethyl methacrylate (PMMA) market report based on form, grade, end use, and region:

Market Report Segmentation")

-

Form Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Extruded Sheets

-

Beads

-

Pellets

-

Cast Acrylic Sheets

-

Others

-

-

Grade Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

General Purpose grade

-

Optical Grade

-

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Signs & Displays

-

Automotive

-

Construction

-

Healthcare

-

Electronics

-

Lightning Fixtures

-

Marine

-

Agriculture

-

Consumer Goods

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Southeast Asia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

GCC Countries

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Form

Revenue capture definition

Extruded Sheet

Revenue is captured through high-volume continuous sheet sales to sign fabricators, display makers, construction converters, and glazing processors that require consistent gauge, formability, and price efficiency.

Cast Acrylic Sheet

Revenue is captured through premium sheet supply for optical, architectural, and decorative uses where clarity, edge finish, thickness range, and machining quality justify higher pricing.

Pellets

Revenue is generated through resin sales to compounders and molders that convert PMMA into automotive, electronics, lighting, and medical parts through injection molding or extrusion.

Beads

Revenue is captured at the polymerization or precursor stage, where bead-form PMMA is supplied to sheet and compound producers that value process control, purity, and narrow specification tolerance.

Others

Revenue is captured from rods, tubes, blocks, and customized stock shapes sold to niche fabricators in industrial, design, security, and specialty engineering applications.

Segment - Grade

Revenue capture definition

General Purpose Grade

Revenue is earned from standard transparency grades used in signage, partitions, consumer goods, and mass-market glazing, where processability and cost discipline outweigh premium optical requirements.

Optical Grade

Revenue is captured from high-purity grades sold into displays, lenses, lighting optics, and instrument covers that require low haze, high transmission, and color stability.

Segment – End Use

Revenue capture definition

Signs & Displays

Revenue is captured through illuminated signage, retail display panels, point-of-purchase structures, and backlit boards that value light diffusion, printability, and surface gloss.

Automotive

Revenue is captured through tail lights, instrument clusters, trims, glazing parts, and specialty covers that demand lightweight transparency and weathering resistance.

Construction

Revenue is generated through skylights, canopies, partitions, façades, windows, and barrier panels sold via fabricators and architectural distributors.

Lighting Fixtures

Revenue is captured through luminaires, diffusers, lamp covers, LED panels, and decorative lighting parts that require optical efficiency and dimensional stability.

Electronics

Revenue is earned from display covers, device windows, housings, keypad panels, and protective components where clarity and hardness are core requirements.

Marine

Revenue is captured from windows, enclosures, protective barriers, and instrument covers used in salt, UV, and moisture exposed environments.

Healthcare

Revenue is generated from device covers, diagnostic housings, dental and optical components, and laboratory parts where purity and sterilization compatibility matter.

Agriculture

Revenue is captured through greenhouse panels, protective covers, and machine enclosures that depend on weatherability, light transmission, and impact durability.

Consumer Goods

Revenue is earned from household, furniture, storage, and decorative items where appearance, surface finish, and moldability support brand differentiation.

Others

Revenue is captured from aerospace, security, industrial, and custom niche uses that buy smaller, specification-led volumes at premium margins.

Estimation Model

Layer Name

Key Question

Description

End-Use Base Layer

Which sectors consume films?

This layer anchors demand to actual fabrication volumes in signage, lighting, automotive, construction, and electronics, which set the consumption baseline.

Form Conversion Layer

What drives value realization?

This layer separates sheets, pellets, beads, and custom shapes because each format carries a different conversion path, margin profile, and volume realization.

Grade Premium Layer

How do grade specifications affect pricing?

This layer weights general-purpose and optical grades separately because purity, haze, and transmission requirements materially change pricing and buyer selection.

Regional Channel Layer

How is demand verified?

This layer reconciles distributor margins, fabricator density, and regional end-use clustering, which together determine how market revenue is finally captured.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Regional demand split by key consumption hubs

Added region-wise demand framing across Asia Pacific, North America, Europe, Latin America, and Middle East & Africa, with commentary on downstream end-use concentration and commercial intensity.

Improves regional prioritization and supports go-to-market focus.

Grade-wise revenue bridge

Added a clearer split between general purpose and optical grades, with revenue logic linked to specification depth, price realization, and downstream application value.

Helps position premium and standard product strategies.

End-use expansion by application cluster

Added a fuller end-use structure covering signs, automotive, construction, lighting, electronics, marine, healthcare, agriculture, consumer goods, and residual niches.

Strengthens segmentation depth for strategic planning.

Frequently Asked Questions About This Report

The polymethyl methacrylate market was estimated at around USD 6.2 billion in the year 2025 and is expected to reach around USD 6.5 billion in 2026.

The polymethyl methacrylate market is expected to grow at a compound annual growth rate of 6.4% from 2026 to 2033 to reach USD 10.0 billion by 2033.

Signs & displays segment led the market with the largest revenue share of 32.6% in 2025.

The key players in the polymethyl methacrylate market include Dymatic Chemicals, Inc.; SK Geo Centric Co. Ltd.; LG Chem; Mitsubishi Chemical Group; CHIMEI; Asahi Kasei Corporation; SABIC; LOTTE Chemical Corporation; Röhm GmbH; Trinseo; Sumitomo Chemical Co., Ltd.

Asia Pacific dominated thepolymethyl methacrylate market with the largest revenue share of 31.0% in 2025.

Based on form, the extruded sheet segment led the market with the largest revenue share of 43.4% in 2025.

Based on grade, the general purpose grade segment led the market with the largest revenue share of 60.8% in 2025.

PMMA demand is anchored in optical clarity, weatherability, and lightweight substitution for glass, which supports steady consumption across signs and displays, lighting, automotive lighting, construction glazing, electronics, and medical parts. Revenue is typically captured through sheets, resins, and molding compounds, with premium value concentrated in optical and cast formats.

The polymethyl methacrylate market is driven by the growing demand from automotive, construction, and electronics industries for lightweight, durable, and transparent materials.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.