- Home

- »

- Plastics, Polymers & Resins

- »

-

Nylon Market Size, Share And Trends Report, 2026-2033GVR Report cover

![Nylon Market (2026 - 2033)Report]()

Nylon Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Nylon 6, Nylon 66), By Application (Automobile, Electrical & Electronics, Engineering Plastics, Textile), By Region, And Segment Forecasts

Market Size, 2025

$38.4BMarket Estimate, 2026

$40.7BMarket Forecast, 2033

$68.4BCAGR, 2026–2033

7.7%Nylon Market Summary

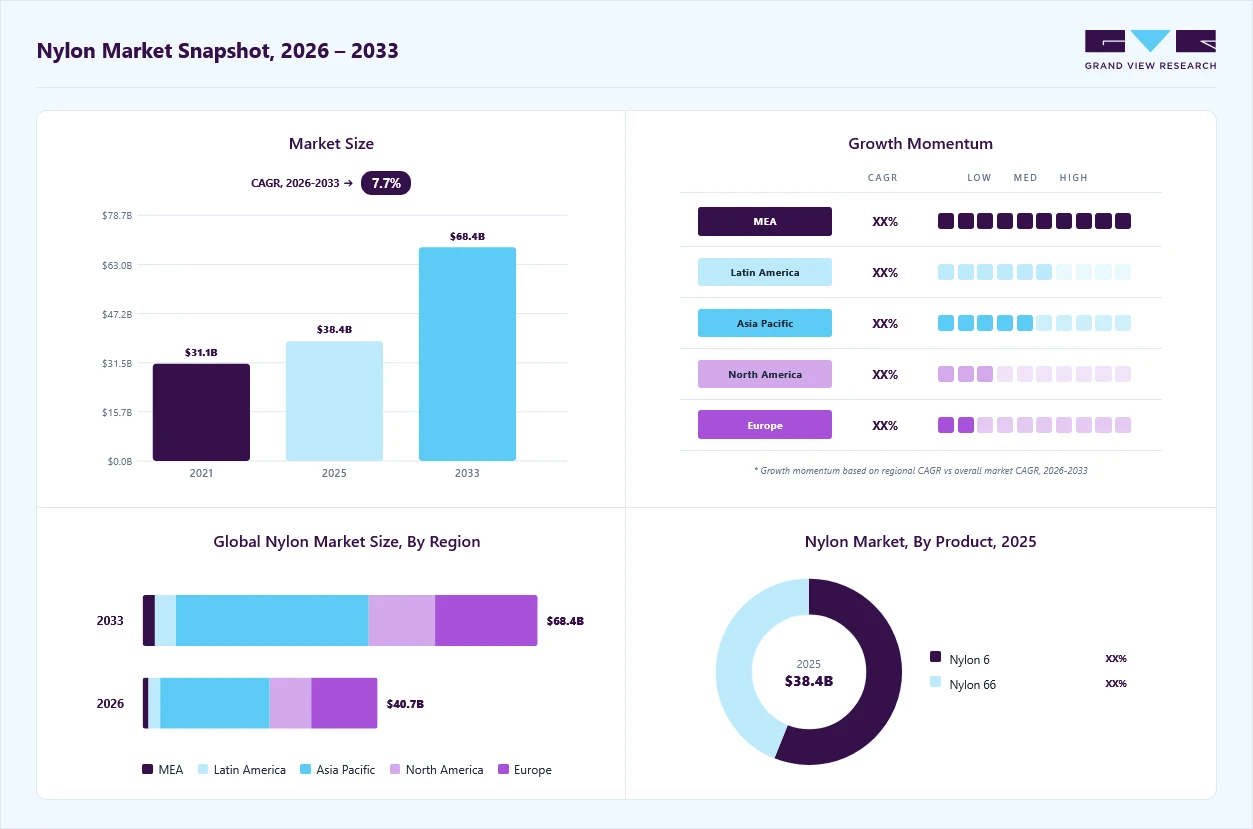

The global nylon market size was valued at USD 38.4 billion in 2025 and is projected to grow from USD 40.7 billion in 2026 to USD 68.4 billion by 2033, at a CAGR of 7.7% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 35.8% in 2025. The increasing demand for nylon in automotive applications is expected to propel the market growth.

Key Market Trends & Insights

- By product: The nylon 66 segment is expected to grow at the fastest CAGR of 7.9% from 2026 to 2033 in terms of revenue.

- By application: The automobile segment is expected to grow at the fastest CAGR of 8.2% from 2026 to 2033 in terms of revenue.

Regional Highlights

- Largest regional market: Asia Pacific (35.8% revenue share, 2025)

- The nylon industry in the China held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 38.4 Billion

- Estimated market size in 2026: USD 40.7 Billion

- Projected market size by 2033: USD 68.4 Billion

- CAGR (2026-2033): 7.7%

The automotive industry is highly concentrated. Even though the product range is high owing to a large number of market participants, approximately 49% of the market is dominated by top players, including GM, Toyota, Ford, and Volkswagen. Nylon is used in engine components such as bushings, bearing, oil containers, wire harness connectors, fuse boxes, cylinder head covers, crankcases, and timing belts.")

The production growth can mainly be attributed to a rapid increase in the China market, as well as the consistent growth of the European automotive industry. In recent years, the automobile industry has witnessed robust growth, especially in the Asia Pacific. Infrastructure development and improved socioeconomic trends are among the major factors that have contributed to the growth of this sector. Favorable regulations, a skilled workforce, and government initiatives to offer attractive FDI regulations have led major players to shift their manufacturing bases to regions such as China, India, and Indonesia.

Currently, raw materials account for over 45% of the vehicles' overall manufacturing cost. Steel and aluminum are the preferred raw materials in the automobile industry. However, owing to stringent regulations aimed at improving fuel efficiency and maintaining CO2 emissions at manageable levels, raw material trends are expected to change drastically. Nylon 6 is used as a film and coating to prevent raw materials from corroding.

These trends have led to the adoption of nylon in the automotive industry, as it is more environmentally friendly than plastics. Apart from being lightweight and versatile, the materials also enable greater design flexibility, allowing the production of advanced shapes without compromising the vehicle's safety and stability. Nylon is anticipated to play a key role in the development of the automobile industry over the forecast period.

Drivers, Opportunities & Restraints

The nylon industry is bolstered by its diverse range of properties, including high strength, heat resistance, durability, and chemical resistance, enabling widespread use across the automotive, electrical, and electronics sectors, industrial components, textiles, and consumer products. Ongoing initiatives to reduce weight and replace metals in automotive and industrial applications continue to enhance demand for reinforced and specialty nylon grades. In the market for nylon 6, demand is bolstered by the material's lower price, straightforward processing, and well-balanced mechanical properties compared to other polyamides, making it one of the most used engineering thermoplastics.

Market expansion is constrained by fluctuations in raw material costs, particularly for essential intermediates sourced from petrochemical feedstocks, which limit manufacturers' and processors' ability to predict expenses. Heightened regulatory oversight and growing sustainability demands pose additional hurdles, as traditional nylon manufacturing relies heavily on energy and fossil fuels. Moreover, competition from alternative engineering materials and high-performance polymers may limit the use of nylon in applications that require greater thermal or chemical resilience.

The market presents considerable opportunities as bio-based and recycled nylon solutions advance, driven by the circular economy's objectives and OEMs' sustainability goals. Innovations in high-performance, flame-retardant, and long-fiber-reinforced nylons are broadening the scope of applications across the automotive, electronics and electrical, and industrial sectors. Furthermore, rising demand from electric vehicles and renewable energy systems, along with ongoing manufacturing growth in developing countries, is expected to open new avenues for expansion. The markets for nylon 6 and nylon 6,6 offer significant prospects due to rising demand for sustainable materials, especially recycled and bio-based polyamides, as original equipment manufacturers in the automotive, electrical and electronics, and consumer goods sectors increasingly focus on low-carbon and circular material options.

Market Concentration & Characteristics

The market growth stage is medium, and the pace of growth is accelerating. The nylon market is characterized by a high degree of innovation owing to the rapid technological advancements.

The market is also characterized by a high level of merger and acquisition (M&A) activity by the leading players. This is due to several factors, including the desire to gain access to new production technologies and talent, need to consolidate in a rapidly growing market.

The nylon industry is also subject to increasing regulatory scrutiny. The global market is subject to numerous regulations, guidelines, and restrictions, such as OSHA (Occupational Safety & Health Administration) - Code of Federal Regulations, European registration, evaluation, authorization, and restriction of chemicals (REACH) standards, European Chemical Agency (ECHA), and NESHAP (National Emission Standard for Hazardous Air Pollutants), among others.

The threat of substitutes from other products, such as polypropylene, bioabsorbable polymers, para-aramid synthetic fibers, and polyvinylidene fluoride, is anticipated to hamper the growth of the global nylon market owing to their lower prices. PVF is gaining acceptance as a major substitute for nylon fishing lines. Other environmentally friendly substitutes, such as bioabsorbable polymers, pose a significant threat due to their biodegradability.

End-user concentration is a significant factor in the market. Automobile manufacturers are expected to use them on a larger scale owing to their environmental benefits, and the advantages offered by Nylon 6 align with the emission regulations laid down across the globe.

Product Insights

The nylon 6 product segment led the nylon market, accounting for 56.11% of global revenue in 2025. The unique properties of PA 6 make the product a cost-effective substitute for materials such as steel, bronze, brass, gunmetal, aluminum, plastics, and rubbers. These properties attract electrical protection device manufacturers to use PA 6 in their offerings. The use of nylon 6 in various applications over the past few years has established its reliability, utility, and economic viability, supported by cost and performance. The excellent surface finish of the product, even under reinforced conditions, makes it suitable for applications where aesthetics are important.

Nylon 6 also attracts substantial demand from the premium carpet industry, which is based in Europe. Turkey is one of the largest importers of nylon for its extensive nylon-based textile industry. The clothing and apparel industry is also witnessing staggering growth, driven by consumer preference for experimenting with various raw materials. Nylon 6 fabrics are smooth, dry quickly, and require minimal care.

They have low absorbency, which can be both advantageous and disadvantageous. The advantage is that water remains on the surface of the fabrics and runs off quickly. Nylon’s low permeability is a disadvantage, as the fabric feels clammy and uncomfortable in warm, moist weather. They also retain their shape after washing. All these factors make it a suitable fabric for apparel.

The automotive industry in China is expected to grow significantly over the forecast period. Nylon is gradually replacing metal components in light vehicles, making them lighter and more fuel-efficient. This trend also aligns with efforts to make vehicles compliant with environmental standards, where nylon components are a perfect fit. Fishing nets are another lucrative application segment of nylon 6. A key aspect that makes it an ideal fabric for fishing nets is its resistance to knotting, which enhances strength and durability.

Application Insights

The automobile application segment led the nylon industry, accounting for 37.05% of global revenue in 2025. Nylon composites are used to increase the environmental sustainability of automotive parts and to reduce the weight of automotive components. The composites are used to manufacture hydraulic clutch lines, headlamp bezels, automotive cooling systems, air intake manifolds, and airbag containers. They are also used in exterior parts such as wheel covers, fuel caps, tailgate handles, doors, front-end grilles, and exterior mirrors. Nylon composites are expected to drive demand in the automotive industry due to their excellent mechanical properties, wear resistance, and the growing need for lightweight vehicles to improve fuel efficiency.

Nylon has been widely used in the automotive engine compartment to replace steel parts, owing to its lower weight and greater design flexibility compared to traditional metals. The trend of engine downsizing has been prevalent in the automotive industry for a long time. It can be attributed to the ability of small-cylinder-capacity engines to toggle between air charge temperatures.

Several market participants have positively responded to this trend by developing oil & heat-resistant polymer compounds for a wide array of automotive designs. The Ultramid Endure produced by BASF SE is one such example of a glass fiber-reinforced PA66. Not only is the material highly resistant to continuous thermal loads, but it also offers good processability for under-hood automotive composites.

Regional Insights

Asia Pacific Nylon market dominated the global market in 2025, with a 46.34% revenue share, driven by robust demand from key industries such as automotive, construction, and consumer goods for TPEs. The region’s advanced manufacturing capabilities and emphasis on sustainable materials contribute to its dominance in the global market. Investment in innovation and product development also fuels growth.

U.S. Nylon Market Trends

The U.S. nylon industry dominated North America, accounting for 74.56% of the revenue share in 2025. The U.S. market exhibits consistent demand across the automotive, electrical and electronics, industrial, and consumer goods sectors, bolstered by the material's cost-effective, high-performance engineering thermoplastic properties. Key factors driving demand include automotive lightweighting, electrification, and the persistent use of nylon in under-the-hood and structural components.

Europe Nylon Market Trends

The Europe nylon industry held a substantial revenue share in 2025. Strong demand from the automotive, electrical and electronics, and industrial sectors is driving the market growth, with the region focusing on lightweight materials, high-performance options, and regulatory compliance. The production of automobiles, especially in powertrain and under-the-hood applications, and in components for electric vehicles, continues to be a significant application for nylon 6 and nylon 6,6.

The China nylon market dominated Asia Pacific in 2025, driven by the swift growth of local manufacturing in the automotive and electrical & electronics sectors, including electric vehicles. This growth is driving strong demand for nylon 6 and nylon 6,6 across components such as connectors, housings, under-the-hood parts, and industrial molded products.

Key Nylon Company Insights

Key companies are adopting a range of organic and inorganic growth strategies, such as new product development, mergers & acquisitions, and joint ventures, to maintain and expand their market share.

-

In September 2025, Australian startup Samsara Eco launched its inaugural plant for recycling nylon 66 and polyester through enzymatic processes in Jerrabomberra, New South Wales. This facility employs cutting-edge EosEco enzyme technology to dismantle and reassemble challenging nylon 66 textile waste, promoting circularity in synthetic fibers and preparing for future production expansions.

-

In March 2025, BASF launched operations at the first industrial facility globally that manufactures loopamid, a recycled polyamide 6 obtained from textile waste, located at its Shanghai Caojing site. This plant has an annual production capacity of 500 tonnes and produces recycled nylon 6 with characteristics comparable to those of virgin nylon 6, catering to the increasing demand for sustainable fibers in functional clothing, outdoor equipment, and related sectors.

Key Nylon Companies:

The following key companies have been profiled for this study on the nylon market.

- BASF SE

- Lanxess

- Huntsman International LLC

- AdvanSix

- Ube Industries Ltd.

- Domo Chemicals

- TORAY INDUSTRIES, INC.

- Ashley Polymers, Inc.

- Ascend Performance Materials

- TOYOBO CO., LTD.

- Goodfellow

Nylon Market Report Scope

Report Attribute

Details

Market size in 2025

USD 38.4 billion

Estimated market size in 2026

USD 40.7 billion

Projected market size by 2033

USD 68.4 billion

Growth rate

CAGR of 7.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in kilotons, revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, and region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; Netherlands; Norway; China; Japan; India; South Korea; Australia; Malaysia; Indonesia; Thailand; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

BASF SE; Lanxess; Huntsman International LLC; AdvanSix; Ube Industries Ltd.; Domo Chemicals; TORAY INDUSTRIES, INC.; Ashley Polymers, Inc.; Ascend Performance Materials; TOYOBO CO., LTD.; Goodfellow

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Nylon Market Report Segmentation

This report forecasts revenue & volume growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global nylon market report based on product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Nylon 6

-

Nylon 66

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Automobile

-

Electrical & Electronics

-

Engineering Plastics

-

Textiles

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Norway

-

Netherlands

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

Thailand

-

South Korea

-

Indonesia

-

Malaysia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Frequently Asked Questions About This Report

Some key players operating in the nylon market include BASF SE, LANXESS, Huntsman Corporation, AdvanSix Inc., Ube Industries Ltd., INVISTA, Domo Chemicals, Toray Industries, Inc., Ashley Polymers Inc., and Ascend Performance Materials LLC.

Key factors that are driving the nylon market growth include nylon application for travel accessories, clothing & apparel, hydraulic clutch lines, headlamp bezels, automotive cooling systems, air intake manifolds, and airbag containers.

The global nylon market is expected to grow at a compound annual growth rate of 7.7% from 2026 to 2033, reaching USD 68.4 billion by 2033.

Asia Pacific dominated with a 35.8% revenue share in 2025.

The nylon 6 product segment led with a 56.1% revenue share in 2025

Automobile application held the largest revenue share 37.1% in 2025.

The global nylon market size was estimated at USD 38.4 billion in 2025 and is expected to reach USD 40.7 billion in 2026.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.