- Home

- »

- HVAC & Construction

- »

-

Lawn Mowers Market Size And Share Report, 2026-2033GVR Report cover

![Lawn Mowers Market Size, Share & Trends Report]()

Lawn Mowers Market (2026 - 2033) Size, Share & Trends Analysis Report By Offering (Hardware, Software), By Propulsion Type (Electric, ICE), By Type, By Lawn Size (Small, Medium), By Level Of Autonomy, By Distribution Channel (Online, Retail), By End-use, By Region, And Segment Forecasts

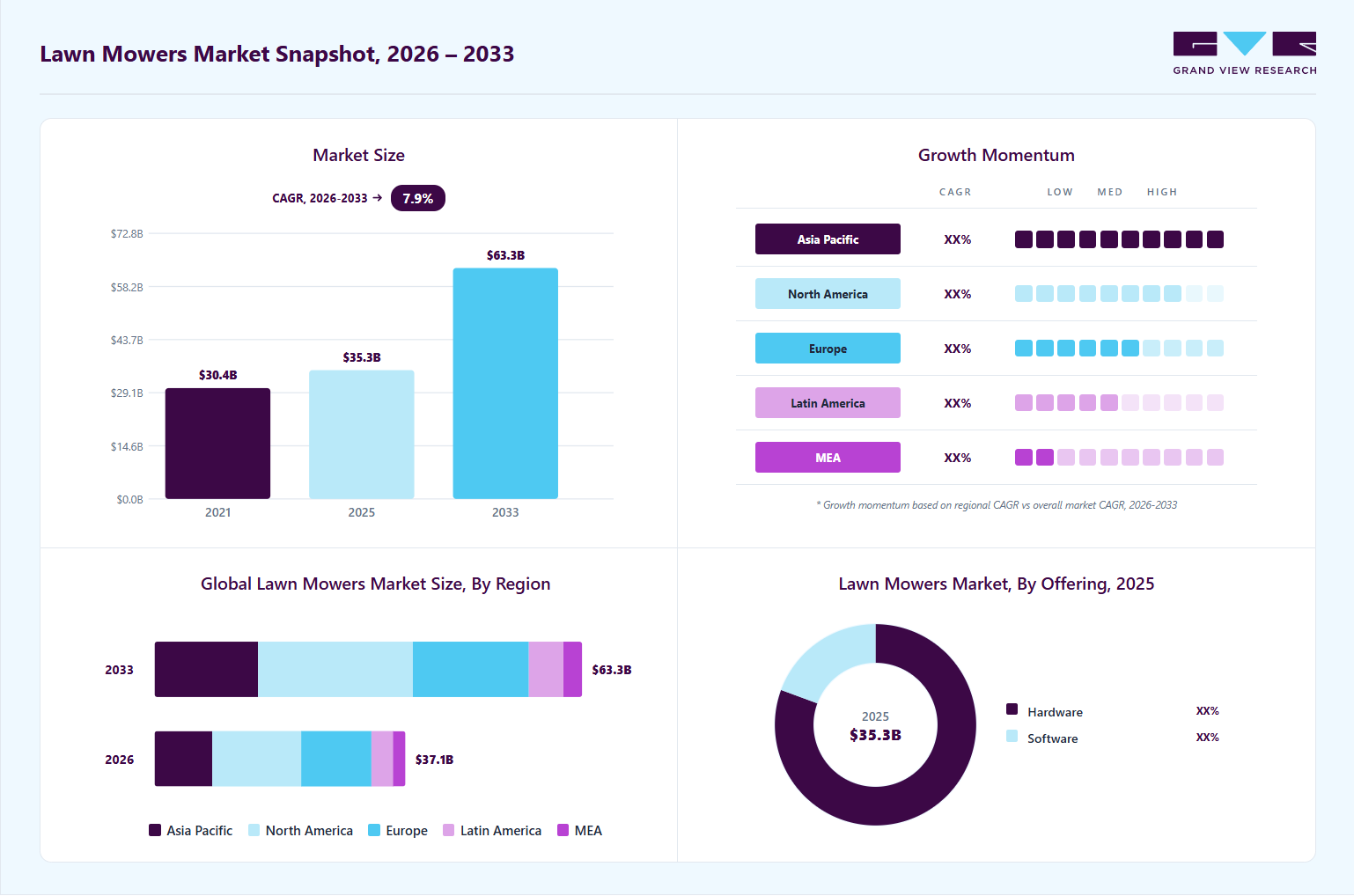

Market Size, 2025

$35.3BMarket Estimate, 2026

$37.1BMarket Forecast, 2033

$63.3BCAGR, 2026–2033

7.9%Lawn Mowers Market Summary

The global lawn mowers market size was estimated at USD 35.3 billion in 2025 and is projected to grow from USD 37.1 billion in 2026 to USD 63.3 billion by 2033, at a CAGR of 7.9% from 2026 to 2033. North America dominated the global market with the largest revenue share of 35.37% in 2025. Increasing awareness of environmental concerns is leading to a demand for eco-friendly, electric, and battery-powered mowers, reducing reliance on traditional gas-powered models.

Key Market Trends & Insights

- By offering: Hardware segment accounted for the largest share of 80.6% in 2025.

- By propulsion type: ICE segment held the largest market share of 53.6% in 2025.

- By type: Walk-behind lawn mowers segment dominated the market with share of 53.2% in 2025.

- By lawn size: Small segment dominated the market with share of 40.8% in 2025.

- By level of autonomy: Non-autonomous segment held the largest market share of 79.9% in 2025.

Regional Highlights

- Largest regional market: North America (35.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. Lawn Mowers industry held a dominant position in 2025.

Market Size & Forecast

- Market size in 2025: USD 35.3 Billion

- Estimated market size in 2026: USD 37.1 Billion

- Projected market size by 2033: USD 63.3 Billion

- CAGR (2026-2033): 7.9%

Consumer preferences for low-maintenance, easy-to-use, and durable lawn mowers also play a pivotal role in shaping the market, with manufacturers focusing on developing products that align with these expectations to gain a competitive edge in the industry. Moreover, with work from home, consumers have time to engage in activities like gardening, paving the way for the residential lawn mowers segment growth. In addition, households with increased disposable income have boosted consumer spending, raising demand for lawn maintenance activities.")

In China, the demand for lawn mowers is expected to reach above pre-COVID levels in 2022 as the Chinese government pushes for eco-city project developments, subsequently creating avenues for future growth. Further, leisure gardening in China is witnessing a steady rise, projected to favor growth over the next few years. Despite changing consumer preferences and patterns in spending power, aesthetic appeal and eco-awareness in the gardening sector of the household remain key drivers for the market. In 2021, the global market rebounded to pre-COVID levels due to increased demand for battery-powered lawn mowers, notably from North America and Europe. However, ongoing semiconductor shortage concerns, disruption in supply chain activities, rising raw material prices, and a surge in oil prices due to the Russian-Ukraine conflict are expected to slow down the market in 2022. Due to these unfavorable macroeconomic conditions, OEMs and dealers are expected to increase the Average Selling Prices (ASP) of lawn mowers in 2022. These developments are likely to be short-lived and are expected to come down by H2 2023.

The lawn mower market is undergoing a dynamic evolution, fueled by technological innovation, environmental concerns, and shifting consumer preferences. One of the most prominent trends is the rise of smart and autonomous mowing solutions. Robotic lawn mowers equipped with GPS, sensors, and AI capabilities are gaining traction among homeowners seeking convenience and precision. These machines can map lawn boundaries, avoid obstacles, and operate with minimal human intervention, significantly reducing maintenance time. Furthermore, integration with mobile apps allows users to control and schedule mowing remotely, aligning with the broader trend toward smart home ecosystems.

Simultaneously, environmental sustainability is becoming a key factor shaping product development and consumer choices. Demand is surging for electric and battery-powered mowers offering quieter operation and producing zero direct emissions-an attractive alternative to traditional gasoline-powered units. As regulatory pressures around noise and emissions increase, manufacturers are investing heavily in greener technologies. In addition, heightened interest in lawn aesthetics and outdoor living is driving demand for high-performance models that deliver consistent cutting quality and versatility across different lawn sizes and terrains. Together, these trends are redefining the lawn mower industry's competitive landscape and growth trajectory.

A surge in demand for smart, efficient, and eco-friendly solutions is reshaping the lawn mower market. Consumers are increasingly gravitating toward robotic and battery-powered mowers that offer low-noise, low-emission alternatives to traditional gas-powered models. Technological advancements such as GPS navigation, AI-based obstacle detection, and remote control via mobile apps are enhancing convenience and precision in lawn maintenance. At the same time, growing environmental awareness and stricter emissions regulations are pushing manufacturers to innovate cleaner, more sustainable products. As outdoor aesthetics gain importance and urban green spaces expand, the market is poised for steady growth driven by automation, sustainability, and user-centric design.

Market Dynamics

Growth in residential landscaping, increased investment in public parks, golf courses, and recreational infrastructure, and higher demand for efficient lawn-maintenance equipment are driving the global lawn mower market. Adoption of battery-powered and robotic lawn mowers is reshaping the industry by providing greater convenience, lower operating costs, and reduced environmental impact. Manufacturers are advancing technologies such as autonomous and energy-efficient designs to improve their market position. Although the high cost of advanced robotic models may limit adoption among price-sensitive consumers, continued innovation and a shift toward sustainable equipment are expected to drive long-term market growth.

The rising demand for residential landscaping and lawn care services is driving the global lawn mower market. Increasing urbanization and a growing emphasis on outdoor aesthetics are encouraging homeowners to invest more in professional landscaping and lawn maintenance services. This trend is further supported by the expansion of residential infrastructure and planned housing communities, where well-maintained green spaces are considered essential to the lifestyle and property value.

Moreover, commercial property managers and facility service providers are increasingly prioritizing efficient and time-saving lawn maintenance practices to manage large landscaped areas. This has led to greater adoption of advanced lawn care equipment and solutions that improve operational efficiency and reduce manual effort. Thus, sustained demand for structured, high-quality lawn maintenance services continues to drive the adoption of both conventional and technologically advanced lawn mowers across residential and commercial end-use segments.

High maintenance requirements and seasonal usage limitations are among the major challenges for the global lawn mower market. Traditional lawn mowers, particularly fuel-powered variants, require frequent servicing, replacement of parts, and regular upkeep, which increases the total cost of ownership for end users. This creates a barrier for cost-sensitive consumers, thereby limiting adoption, especially in price-competitive markets. In addition, the utilization of lawn mowers is largely dependent on climatic and seasonal conditions, with demand peaking during specific periods of the year in several regions. In colder or dry seasons, usage declines significantly, leading to underutilization of equipment and slower replacement cycles. This cyclical demand pattern restricts consistent revenue generation for manufacturers and hampers overall market growth momentum.

The rapid adoption of battery-powered and robotic lawn mowers creates a significant growth opportunity for the global lawn mowers market. Growing environmental awareness, along with stringent emission regulations, is accelerating the shift from conventional fuel-based equipment toward cleaner, energy-efficient alternatives. Battery-powered and robotic lawn mowers are increasingly preferred for their low noise and user-friendly operation, making them highly suitable for both residential and commercial applications.

This opportunity is further strengthened by continuous technological advancements and product innovation in smart outdoor equipment. Market players are actively expanding their offerings to integrate automation, AI, and IoT into lawn care solutions. For instance, in December 2025, Roborock, widely recognized for its innovation in intelligent home cleaning technology, launched its first robotic lawn mower. The product is designed to deliver intelligent, hands-free lawn care, reflecting the company’s expansion of automation capabilities beyond indoor cleaning solutions.

Analyst Perspective

Growth in residential landscaping and increased consumer interest in attractive outdoor spaces are driving the global lawn mowers market. Rising adoption of battery-powered and robotic models reflects demand for convenient, low-emission, and advanced solutions. Manufacturers are focusing on product innovation and automation to improve efficiency and user experience. Expansion of commercial landscaping and managed green spaces is also boosting demand across various sectors. These trends are expected to support sustained market growth over the forecast period.

Offering Insights

Based on offering, the hardware segment led the market with the largest revenue share of 80.6% in 2025. The hardware segment is undergoing significant transformation, driven by advancements in battery technology, increasing environmental awareness, and the integration of smart features. Battery-powered mowers are gaining traction due to their quiet operation, zero emissions, and reduced maintenance needs. Improvements in lithium-ion batteries have enhanced performance, offering longer runtimes and faster charging, making them more practical for both residential and commercial use. Manufacturers are also focusing on developing smart mowers equipped with GPS navigation, automated scheduling, and real-time monitoring, enhancing user convenience and efficiency. Despite the rise of electric models, petrol-powered mowers continue to dominate in scenarios requiring high power and extended operation times, particularly in large or rugged terrains.

The Software segment is expected to grow at a significant CAGR during the forecast period. The segment is experiencing rapid growth due to the integration of advanced technologies that enhance user convenience and operational efficiency. Modern robotic mowers are equipped with features such as GPS navigation, AI-driven obstacle detection, and real-time weather responsiveness, allowing for autonomous operation and adaptive mowing schedules. Smartphone applications enable users to remotely control and monitor their mowers, adjust cutting parameters, and receive maintenance alerts, contributing to a seamless lawn care experience. Furthermore, compatibility with voice assistants like Amazon Alexa and Google Assistant facilitates hands-free operation, aligning with the broader trend of smart home integration.

Propulsion Type Insights

Based on propulsion type, the ICE segment led the market with the largest revenue share of 53.6% in 2025. The Internal Combustion Engine (ICE) segment continues to dominate the lawn mower market due to its high power output, durability, and suitability for large or rugged terrains. These mowers are particularly favored by professional landscapers and commercial users who require extended operating hours and the ability to tackle thick or tall grass efficiently. The widespread availability of fuel, established servicing infrastructure, and relatively lower upfront costs contribute to the sustained demand for ICE-powered mowers. Moreover, ongoing enhancements in engine efficiency and emission control technologies are helping manufacturers meet tightening environmental regulations, thereby maintaining the relevance of ICE models in both developed and emerging markets.

The electric segment is projected to grow at the fastest CAGR over the forecast period. The electric lawn mower segment is rapidly emerging as a preferred choice among residential users, driven by growing environmental awareness, urbanization, and advances in battery technology. Lithium-ion batteries now offer longer runtimes and faster charging, making electric mowers more practical and reliable. These models are appreciated for their low noise, zero direct emissions, and minimal maintenance needs. Additionally, the integration of smart features such as mobile app connectivity, automated scheduling, and GPS-enabled navigation has enhanced their appeal among tech-savvy consumers. As regulatory pressures on emissions increase and sustainable living gains momentum, the electric segment is poised for significant growth and wider adoption.

Type Insights

Based on type, the walk-behind lawn movers segment led the market with the largest revenue share of 53.2% in 2025. These mowers are especially popular among residential users who prefer manual control for precise cutting, particularly in smaller to mid-sized lawns. Their broad range-from push mowers to self-propelled variants-caters to different user preferences and budgets. Additionally, manufacturers are enhancing these models with ergonomic designs, improved fuel efficiency, and electric start features, making them more convenient and appealing. The strong presence of ICE-powered models in this category further reinforces its dominance, particularly in markets where large outdoor spaces are common.

The robotic lawn mowers segment is projected to grow at the fastest CAGR over the forecast period. Robotic lawn mowers are rapidly gaining traction as an innovative and hassle-free solution for lawn maintenance. The segment is primarily driven by advancements in automation, AI, and smart connectivity. These mowers offer autonomous operation with features like GPS tracking, obstacle detection, and app-based controls. They are especially attractive to tech-savvy consumers and urban homeowners who seek minimal manual intervention and quiet, energy-efficient performance. The increasing emphasis on smart home integration and sustainable living is further accelerating the adoption of robotic mowers.

Lawn Size Insights

Based on lawn size, the small segment led the market with the largest revenue share of 40.8% in 2025. Consumers in this segment prioritize compact, lightweight, and easy-to-store mowing solutions that offer convenience and efficiency. Walk-behind electric and battery-powered mowers are especially popular, as they provide quiet operation, low maintenance, and sufficient power for smaller plots. Furthermore, the affordable products targeted at this segment makes them accessible to a broad consumer base. As housing developments continue to favor compact residential lots, demand for small-lawn mowers is expected to remain strong.

The medium segment is projected to grow at the fastest CAGR over the forecast period. The medium lawn segment is emerging as a key growth area, supported by expanding suburban developments and growing interest in larger home gardens and outdoor living spaces. Consumers with medium-sized lawns are increasingly seeking mowers that strike a balance between power and maneuverability. This is driving demand for more robust walk-behind models and the rising adoption of robotic and self-propelled mowers equipped with longer battery runtimes and wider cutting decks. The trend toward sustainable landscaping and reduced labor also aligns well with the features offered in this segment. As homeowners invest more in outdoor aesthetics and automation, the medium lawn segment is poised for steady expansion.

Level Of Autonomy Insights

Based on level of autonomy, the non-autonomous segment led the market with the largest revenue share of 79.9% in 2025. These traditional mowers, including both push and self-propelled types, offer reliable performance and are favored by homeowners who value hands-on mowing, especially for detailed or irregularly shaped lawns. Their mechanical simplicity, ease of maintenance, and established market trust contribute to sustained demand. Additionally, improvements in ergonomics, engine efficiency, and safety features have enhanced the user experience, reinforcing the non-autonomous mower's position as the go-to choice for both residential and professional applications.

The autonomous segment is projected to grow at the fastest CAGR over the forecast period. The segment is rapidly emerging as a transformative force in the lawn mower market, driven by advancements in robotics, AI, and smart home integration. Robotic mowers equipped with GPS navigation, sensor-based obstacle detection, and app-controlled scheduling are gaining popularity among tech-savvy and time-conscious consumers. These machines offer a set-it-and-forget-it convenience, operating quietly and efficiently with minimal human intervention. As battery technology and connectivity improve and prices become more accessible, autonomous mowers are increasingly seen as a smart investment for modern lawn care.

Distribution Channel Insights

Based on distribution channel, the retail segment led the market with the largest revenue share of 67.1% in 2025. The retail segment remains the dominant distribution channel in the lawn mower market, primarily due to the consumer preference for hands-on product evaluation before purchase. Many buyers appreciate the opportunity to inspect mowers in person, compare different models directly, and get instant assistance from sales representatives. These factors are especially crucial when investing in high-performance equipment. Brick-and-mortar outlets, including home improvement stores and garden centers, also offer after-sales support, in-store promotions, and bundled services like assembly or delivery. This tactile shopping experience, brand loyalty, and immediate product availability continue to drive strong sales through the retail channel.

The online segment is projected to grow at the fastest CAGR over the forecast period. The online segment is rapidly emerging as a significant growth channel, driven by increasing internet penetration, evolving consumer behavior, and the convenience of digital shopping. E-commerce platforms offer a wide variety of models, detailed product descriptions, user reviews, and competitive pricing, enabling informed decision-making from the comfort of home. The rise of direct-to-consumer brands, digital marketing, and seasonal online promotions further accelerates online adoption. Additionally, advancements in virtual tools like 3D product views, video demonstrations, and AI-powered recommendations are enhancing the online shopping experience.

End Use Insights

Based on end-use, the residential segment led the market with the largest revenue share of 55.3% in 2025. The segment dominates the lawn mower market, driven by widespread homeownership and the increasing emphasis on outdoor aesthetics and personal landscaping. Homeowners, particularly in suburban and urban areas with small to mid-sized lawns, seek affordable, compact, and easy-to-use mowers that require minimal maintenance. This demand has led to a surge in battery-powered and walk-behind models, which offer quiet operation, environmental benefits, and user-friendly features like push-button starts and height adjustments. As more consumers invest in home improvement and gardening during seasonal months, the residential segment continues to see strong, consistent growth.

The commercial segment is expected to grow at a significant CAGR during the forecast period. The segment is emerging as a key growth driver in the lawn mower market, fueled by expanding demand for professional landscaping services in public parks, sports facilities, corporate campuses, and residential complexes. Commercial users prioritize durability, high performance, and efficiency, leading to growing adoption of zero-turn mowers, ride-on models, and increasingly, autonomous and connected equipment for large-area maintenance. As sustainability goals and labor shortages become more pressing, businesses are also exploring electric and robotic options to reduce operating costs and improve productivity. These trends are expected to propel the commercial segment forward as landscaping becomes more structured and technology-driven.

Regional Insights

North America dominated the lawn mowers market with the largest revenue share of 35.3% in 2025. The growth of the segment is driven by high consumer spending on outdoor equipment, large residential lawn areas, and widespread adoption of power tools. The U.S. leads the region, fueled by suburban housing trends and a strong do-it-yourself (DIY) culture. Established players are innovating with battery-powered models, while robotic mower adoption is rising in tech-forward households. Retail giants and e-commerce platforms have expanded product availability and aftersales services, enhancing consumer reach and engagement.

U.S. Lawn Mowers Market Trends

The lawn mowers market in the U.S. held the largest share in the North America region in 2025. Gasoline-powered walk-behind mowers remain the mainstay for medium to large lawns, while electric and robotic mowers are gaining traction due to noise regulations and sustainability awareness. Federal and state-level incentives on electric garden tools in eco-conscious states like California and Oregon have accelerated battery mower adoption.

Europe Lawn Mowers Market Trends

The Lawn Mowers industry in Europe was identified as a lucrative region in 2024. Germany, France, and the UK are key growth engines, with robotic mowers becoming mainstream in residential areas and gated communities. Germany’s "GreenTech" initiatives have incentivized electric and autonomous mower purchases, especially in Bavaria and Baden-Württemberg, while EU emission norms continue to phase out traditional two-stroke engines. The UK is focusing on smart gardening tools through initiatives like the “Digital Garden” pilot in suburban London, where robotic mowers are being tested with smart irrigation systems.

The lawn movers market in UK is witnessing steady growth, driven by a rising focus on garden aesthetics, sustainability, and smart home integration. Consumers are increasingly shifting from traditional petrol mowers to electric and robotic models, spurred by environmental regulations and a growing preference for low-maintenance, quiet solutions.

Asia Pacific Lawn Mowers Market Trends

The Asia-Pacific region is experiencing rapid growth in the Lawn Mowers market. The Asia-Pacific region is the fastest-growing lawn mower market, led by expanding urbanization, rising disposable incomes, and increased landscaping activity in residential and commercial areas. Japan, Australia, and China are at the forefront of adoption. Japan is advancing with robotic mowers for compact urban gardens and promoting automation through partnerships between municipal governments and smart tech firms. China’s urban greening initiatives in cities like Shanghai and Guangzhou are driving sales of battery-powered mowers, especially among landscaping service providers.

The lawn movers market in China is experiencing robust growth, propelled by rapid urbanization, expanding middle-class households, and government-led green infrastructure initiatives. As cities invest in beautifying urban landscapes and public parks, demand for efficient, high-performance mowers-particularly in the commercial and municipal segments-is accelerating.

Key Lawn Mowers Company Insights

Some of the major players in the lawn mowers market include Deere & Company, American Honda Motor Co., Inc., Husqvarna Group, and MTD Products. These companies are at the forefront of transforming lawn care through advanced technology, sustainability, and smart automation. By investing in research and development, and forming strategic partnerships across battery technology, robotics, and IoT ecosystems, they are redefining user expectations in both residential and commercial segments. Their scalable product portfolios-ranging from high-efficiency walk-behind mowers to AI-enabled robotic units-are designed to enhance performance, reduce environmental impact, and improve user convenience.

-

American Honda Motor Co., Inc. offers nearly 70 models of power equipment in its product lines such as lawnmowers, snow blowers, generators, pumps, trimmers, and tillers. The company’s prominent products are assembled at more than 11 Honda manufacturing facilities across the globe.

-

Deere & Company has operation centers located in 30 countries across the globe. The company offers its products through various third-party dealers, some of which include Austin Turf & Tractor, Storm Lawn & Garden, LLC, United Ag & Turf, Lawn Land, Ag-Pro Texas, LLC, and Shoppa's Farm Supply, Inc.

Key Lawn Mowers Companies:

The following key companies have been profiled for this study on the lawn mowers market.

-

American Honda Motor Co., Inc.

-

Ariens Company

-

Briggs Stratton

-

Deere & Company

-

Falcon Garden Tools

-

Fiskars

-

Husqvarna Group

-

MTD Products

-

Robert Bosch GmbH

-

Robomow Friendly House

-

The Toro Company

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Established Players: Deere & Company, Husqvarna Group, The Toro Company, Robert Bosch GmbH, American Honda Motor Co., Inc., Ariens Company, MTD Products, Briggs & Stratton

- Focus on broad product portfolios covering walk-behind, riding, zero-turn, and robotic lawn mowers.

- Invest heavily in R&D to develop battery-powered, autonomous, and smart-connected mowing solutions.

- Strengthen global distribution networks through dealers, retailers, and e-commerce channels.

- Strong brand recognition and customer trust built over decades.

- Extensive global manufacturing, distribution, and service infrastructure.

- Large R&D budgets supporting continuous product innovation.

- Higher operational and manufacturing costs compared to smaller competitors.

- Slower decision-making processes due to complex organizational structures.

- Dependence on mature markets with relatively slower growth rates.

Emerging Players: Robomow Friendly House, Falcon Garden Tools, Fiskars

- Focus on specialized segments such as robotic, lightweight, and eco-friendly lawn mowers.

- Leverage digital sales channels and direct-to-consumer business models.

- Target underserved customer groups with innovative and cost-effective products.

- Greater flexibility in responding to changing consumer preferences.

- Strong focus on innovation within specific product niches.

- Lower organizational complexity enabling faster product development cycles.

- Limited brand awareness compared to established industry leaders.

- Smaller distribution and service networks.

- Lower financial resources for large-scale R&D and expansion initiatives.

Recent Developments

-

In February 2025, Eufy, a brand under Anker Innovations, has launched two new robotic lawn mowers-the Eufy Robot Lawn Mower E15 and E18-offering exclusive pre-sale access to current users in North America via the Eufy app until February 28. The products will be available for full retail sale on eufy.com and Amazon in April. Known for its smart home devices, Eufy is expanding into the lawn care market, aiming to bring the same innovation and convenience seen in its vacuums and security systems. The new mowers feature Eufy’s Vision Full-Self Driving (V-FSD 1.0) technology, enabling them to detect and avoid obstacles, identify lawn edges, and follow paths precisely. This move reinforces Eufy’s commitment to simplifying home maintenance through advanced automation.

-

In January 2025, John Deere launched its latest innovation a fully electric, battery-powered autonomous zero-turn, stand-on mower. Featuring a 60-inch rear-discharge deck, the mower can operate both autonomously and manually with an operator. It includes integrated batteries, off-board charging options, and significantly reduces noise and emissions. Equipped with multiple cameras, GPS antennas, and wheel odometry, it ensures accurate navigation and object detection. Deere developed the mower by adapting its agricultural technology and collaborating with landscaping professionals to meet commercial needs.

Lawn Mowers Market Report Scope

Report Attribute

Details

Market size in 2025

USD 35.3 billion

Estimated market size in 2026

USD 37.1 billion

Projected market size by 2033

USD 63.3 billion

Growth rate

CAGR of 7.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Offering, propulsion type, type, lawn size, level of autonomy, distribution channel, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

American Honda Motor Co., Inc.; Ariens Company; Briggs Stratton; Deere & Company; Falcon Garden Tools; Fiskars; Husqvarna Group; MTD Products; Robert Bosch GmbH; Robomow Friendly House; The Toro Company

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Lawn Mowers Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global lawn mowers market report based on offering, propulsion type, type, lawn size, level of autonomy,distribution channel, end use, and region.

-

Offering Outlook (Revenue, USD Million, 2021 - 2033)

-

Hardware

-

Ultrasonic Sensors

-

Lift Sensors

-

Tilt Sensors

-

Motors

-

Microcontrollers

-

Batteries

-

-

Software

-

-

Propulsion Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Electric

-

ICE

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Riding Lawn Movers

-

Walk-behind Lawn Movers

-

Robotic Lawn Movers

-

-

Lawn Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Small

-

Medium

-

Large

-

-

Level of Autonomy Outlook (Revenue, USD Million, 2021 - 2033)

-

Autonomous

-

Non-autonomous

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Online

-

Retail

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Residential

-

Commercial

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Research Methodology

(a) Segment Definition

Segment - Offering

Revenue capture definition

Hardware

The hardware segment includes digital textile printing machines, such as direct-to-fabric and direct-to-garment printers, as well as key components such as printheads, ink systems, and curing units. Revenue is generated mainly through the sale of new equipment and replacement parts to textile and apparel manufacturers.

Software

The software segment includes design, color management, workflow automation, AI-based optimization, and IoT-enabled monitoring solutions used in digital textile printing systems. Revenue is generated through software licensing, subscriptions, and digital service integrations that improve efficiency and print quality.

Segment – Propulsion Type

Revenue capture definition

Electric

The electric segment includes battery-powered and corded digital textile printing systems that operate using rechargeable batteries or a direct power supply. Revenue is generated from the sale of energy-efficient printing equipment and associated systems, driven by demand for low-emission, sustainable production solutions.

ICE (Internal Combustion Engine)

The ICE segment includes conventional fuel-powered systems used in certain heavy-duty or industrial printing setups that require continuous, high-output operation. Revenue is generated through equipment sales and maintenance services, though its growth is gradually constrained by sustainability shifts and environmental regulations.

Segment – Type

Revenue capture definition

Riding Lawn Mowers

The riding segment includes high-capacity, operator-driven digital textile printing systems designed for large-scale production environments with wider output capability and enhanced operational efficiency. Revenue is generated through the sale of premium high-throughput machines and related system integrations used in industrial textile manufacturing.

Walk-behind Lawn Mowers

The walk-behind segment comprises manually operated or semi-automated digital textile printing machines for small- to medium-scale production and customized printing needs. Revenue is driven by high-volume sales to SMEs and commercial users, driven by affordability and ease of operation.

Robotic Lawn Mowers

The robotic segment includes fully automated digital textile printing systems integrated with AI, IoT, and advanced control technologies, enabling minimal human intervention and high-precision output. Revenue is generated through premium equipment sales and the adoption of smart manufacturing.

Segment – Lawn Size

Revenue capture definition

Small

The small segment includes compact residential lawns that require lightweight, easy-to-use digital textile printing solutions. Revenue is generated through high-volume sales of entry-level and compact systems driven by urban and home-based demand.

Medium

The medium segment covers suburban and small commercial applications requiring moderate-capacity printing systems. Revenue is driven by steady demand for mid-range solutions and regular equipment replacement cycles.

Large

The large segment includes industrial-scale applications, such as estates and commercial facilities, that require high-performance printing systems. Revenue is generated through premium equipment sales and bulk installations driven by large-scale production needs.

Segment – Level of Autonomy

Revenue capture definition

Autonomous

The autonomous segment includes AI-enabled, automated digital textile printing systems that operate with minimal human intervention, leveraging smart sensors, IoT, and advanced software integration. Revenue is generated through premium system sales and smart feature adoption.

Non-autonomous

The non-autonomous segment includes manually operated and conventional digital textile printing systems requiring direct operator control. Revenue is driven by high-volume equipment sales and replacement demand across residential, commercial, and small- to medium-scale manufacturing applications.

Segment – Distribution Channel

Revenue capture definition

Online

The online segment includes digital platforms and brand websites used for purchasing digital textile printing systems and related solutions. Revenue is generated through direct-to-consumer and business-to-business online sales, driven by increasing digital adoption and wider product accessibility.

Retail

The retail segment includes physical dealer networks, showrooms, and specialty equipment distributors for digital textile printing systems. Revenue is generated through in-store purchases and channel partnerships, supported by customer interaction, product demonstration, and after-sales services.

Segment – End Use

Revenue capture definition

Residential

The residential segment includes household users managing private lawns, gardens, and small outdoor spaces, with demand driven by urbanization and growing interest in home aesthetics. Revenue is generated through high-volume sales of compact, easy-to-use, and cost-effective mowers.

Commercial

The commercial segment includes professional landscaping companies, municipal bodies, golf courses, and large property managers requiring high-performance equipment for large-area maintenance. Revenue is generated through bulk purchases and the adoption of premium-grade mowers, supported by infrastructure development and the outsourcing of landscaping services.

(b) Estimation Model

Layer No.

Layer Name

Key Question

Description

01

Product Adoption Layer

Who can and is willing to adopt lawn mowers?

Establish the total potential demand analysis by identifying all users, facilities, assets, or entities that currently own, operate, or could require the equipment. This serves as the foundation for market sizing before any market-specific filters are applied.

02

Addressable Market Layer

Who can realistically be reached and served?

Refine the total universe into the realistically serviceable market by applying geographic, industry, infrastructure, regulatory, and operational filters. This helps determine the portion of the installed base that can actually purchase or adopt the equipment.

03

Purchase & Replacement Layer

Who is actively purchasing, replacing, or upgrading equipment?

Estimate the annual demand generation by evaluating replacement cycles, equipment aging, fleet expansion, new installations, technology upgrades, and adoption trends. This converts the addressable installed base into yearly purchasing activity.

04

Revenue Monetization Layer

How much revenue is generated from this demand?

Convert equipment demand into market revenue by applying average selling prices (ASP), product mix, aftermarket sales, maintenance contracts, spare parts, consumables, software, and other recurring revenue streams where applicable.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Sr No.

Client Request

Customization Delivered

Value Adds

01

Competitive Benchmarking of Key Lawn Mower Manufacturers

Comparative analysis of product portfolios, pricing, and regional presence of selected competitors.

Evaluation of strategic initiatives including product launches, partnerships, and acquisitions.SWOT analysis of key market participants.

Competitive positioning matrix and estimated market share assessment.02

Country-Level Demand Assessment

Country-specific analysis of lawn mower demand drivers, consumer behavior, and landscaping trends.

Assessment of regulatory policies, urban green space development, and distribution networks.Country attractiveness ranking and opportunity mapping.

Import-export analysis and forecast of future demand potential.03

Robotic and Battery-Powered Lawn Mower Opportunity Analysis

Evaluation of adoption trends for robotic and battery-powered lawn mowers across key regions.

Analysis of consumer preferences and technology developments.Technology roadmap highlighting future innovation opportunities.

Investment opportunity assessment and growth potential by market segment.Frequently Asked Questions About This Report

Some key players operating in the lawn mowers market include Deere and Company; MTD products; American Honda Motor Co., Inc.; Robert Bosch GmbH; STIGA S.p.A.; Robomow Friendly House; Husqvarna Group; and AriensCo.

North America dominated with a 35.37% revenue share in 2025.

Asia Pacific is the fastest growing over the forecast period.

The global lawn mowers market size was estimated at USD 35.3 billion in 2025 and is expected to reach USD 37.1 billion in 2026.

The global lawn mowers market is expected to grow at a compound annual growth rate of 7.9% from 2026 to 2033 to reach USD 63.3 billion by 2033.

The walk-behind lawn mowers segment led with a 53.2% revenue share in 2025, while robotic lawn mowers is the fastest-growing segment.

Growth in residential landscaping, increased investment in public parks, golf courses, and recreational infrastructure, and higher demand for efficient lawn-maintenance equipment are driving the global lawn mower market.

The hardware segment led with a 80.6% revenue share in 2025, and is the fastest growing segment.

The ICE segment led with a 53.6% revenue share in 2025, and electric is the fastest growing segment.

About the Author(s)

HVAC & Construction Research Team

Technology · HVAC & ConstructionThis report was authored by the hvac & construction research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the hvac & construction segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.