- Home

- »

- Advanced Interior Materials

- »

-

Injection Molding Market Size And Share Report, 2026-2033GVR Report cover

![Injection Molding Market (2026 - 2033)Report]()

Injection Molding Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Plastics, Metals), By Application (Packaging, Consumables & Electronics, Automotive & Transportation), By Region And Segment Forecasts

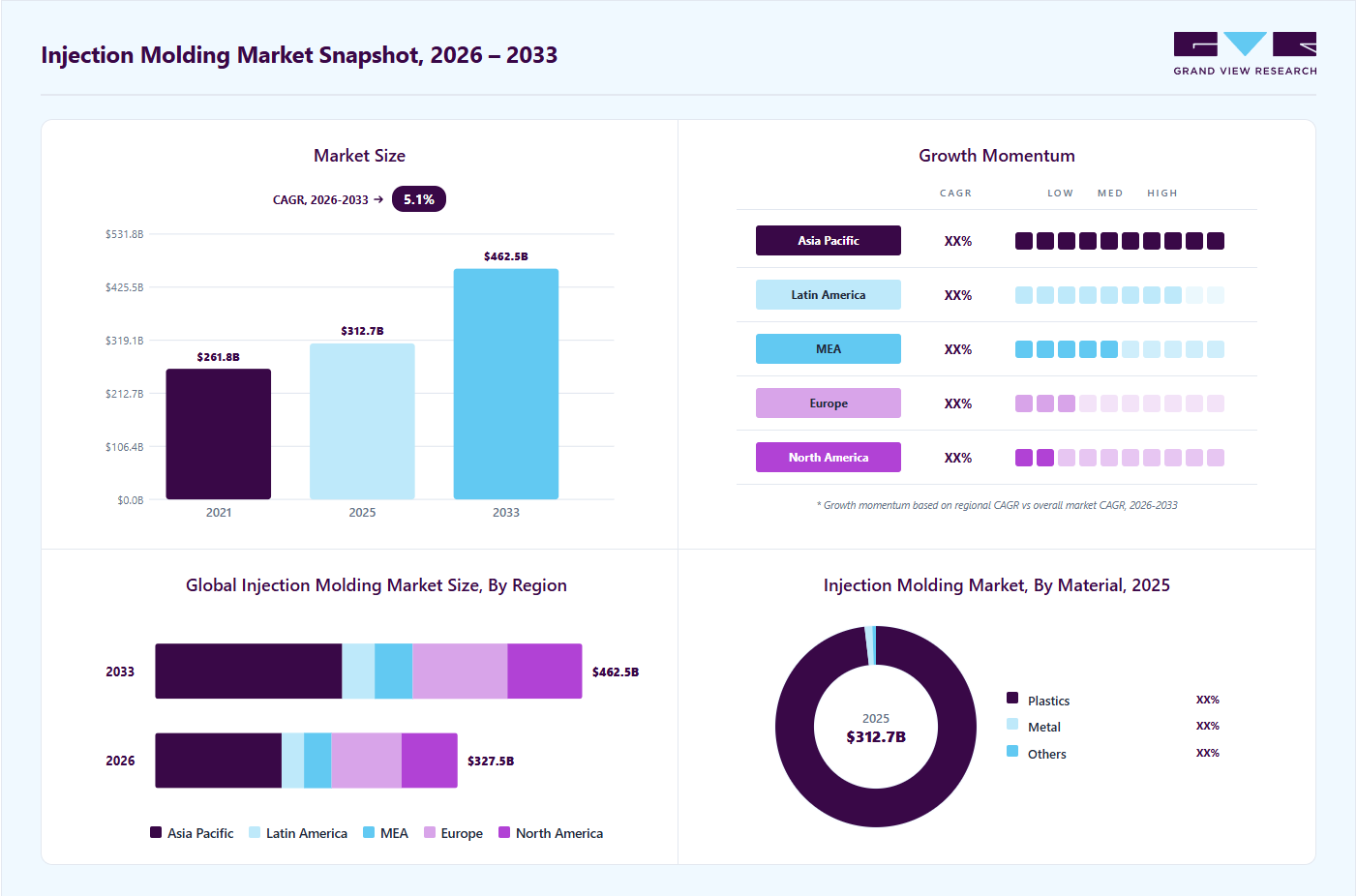

Market Size, 2025

$312.7BMarket Estimate, 2026

$327.5BMarket Forecast, 2033

$462.5BCAGR, 2026–2033

5.1%Injection Molding Market Summary

The global injection molding market size was valued at USD 312.7 billion in 2025 and is projected to grow from USD 327.5 billion in 2026 to USD 462.5 billion by 2033, growing at a CAGR of 5.1% from 2026 to 2033. The Asia Pacific market held the largest share of 41.2% of the global market in 2025. The growing demand for lightweight and durable plastic products across the automotive, packaging, and consumer goods sectors is fueling the injection molding market.

Key Market Trends & Insights

- By material: The plastics segment led the market with the largest revenue share of 98.2% in 2025.

- By application: The packaging segment led the market with the largest revenue share of 32.1% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (41.2% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 312.7 Billion

- Estimated market size in 2026: USD 327.5 Billion

- Projected market size by 2033: USD 462.5 Billion

- CAGR (2026-2033): 5.1%

Advancements in high-precision molding technology allow manufacturers to produce complex components efficiently. Rising adoption of automation and robotics in production lines enhances speed and reduces labor costs.")

Increasing use of bio-based and recycled plastics supports sustainability initiatives, driving market growth. The expansion of end-use industries in emerging economies boosts the demand for cost-effective molding solutions. Continuous innovation in materials, including engineering plastics, enables versatile product applications. Growing e-commerce and packaging requirements further create a steady demand for injection-molded components globally.

Market Dynamics

The injection molding market is influenced by manufacturing activity across automotive, packaging, medical, consumer goods, and electronics industries, where high-volume production of plastic components remains essential. Demand is shaped by increasing adoption of lightweight and complex molded parts, advancements in engineering polymers, and growing requirements for precision manufacturing. Market growth is also affected by investments in automation, all-electric molding machines, and smart factory technologies that improve productivity and reduce operating costs. Additionally, sustainability initiatives promoting recyclable materials, bio-based polymers, and energy-efficient production processes are influencing both equipment purchases and material selection, while fluctuations in resin prices, industrial output, and capital expenditure trends continue to impact overall market dynamics.

The increasing demand for packaged food, beverages, personal care products, and household goods is a major factor supporting growth in the injection molding market. Injection molding is widely used to manufacture packaging components such as caps, closures, containers, dispensers, and thin-wall packaging products due to its ability to deliver high production volumes, consistent quality, and cost efficiency. Rising urbanization, changing consumer lifestyles, and the expansion of e-commerce are further driving the need for durable and lightweight packaging solutions, contributing to increased demand for injection molded products.

Fluctuations in the prices of plastic resins and other raw materials present a significant challenge for injection molding manufacturers. Resin costs are influenced by crude oil prices, supply-demand imbalances, feedstock availability, and geopolitical developments, creating uncertainty in production costs and profit margins. Frequent price variations can affect purchasing decisions, contract negotiations, and overall operational planning, particularly for manufacturers serving highly competitive end markets with limited ability to pass increased costs to customers.

The rapid expansion of electric vehicle (EV) production is creating substantial opportunities for the injection molding market. Automotive manufacturers are increasingly utilizing injection molded plastic components to reduce vehicle weight, improve energy efficiency, and extend driving range. Applications include battery housings, interior components, connectors, under-the-hood parts, and structural elements manufactured from advanced engineering plastics. As vehicle electrification accelerates globally, demand for lightweight, durable, and precision-molded components is expected to increase, supporting greater adoption of advanced injection molding technologies and materials.

Market Concentration & Characteristics

The global injection molding machine market is highly fragmented, with a large number of regional and international players competing across different geographies. While a few leading companies hold notable shares through advanced technology, global distribution networks, and strong brand recognition, the presence of numerous small and medium-sized manufacturers intensifies competition. This results in a diverse and fragmented industry landscape, where innovation, pricing, and service capabilities play critical roles in market positioning.

The injection molding industry demonstrates a moderate to high degree of innovation, driven by advancements in automation, robotics, and precision molding technologies. Companies continuously develop new materials, energy-efficient processes, and complex product designs. Innovations in additive manufacturing and smart factory integration are also shaping the market. This focus on R&D enables manufacturers to meet evolving customer demands and industry standards.

The market experiences a steady level of mergers and acquisitions, primarily aimed at expanding product portfolios, geographic reach, and technological capabilities. Leading players often acquire specialized firms to enhance their expertise in medical, automotive, or high-precision molding segments. These transactions strengthen competitive positioning and operational efficiency. M&A activity also accelerates market consolidation in key regions.

Strict regulatory standards, particularly in the medical, pharmaceutical, and food packaging sectors, heavily influence market operations. Compliance with ISO, FDA, and REACH regulations is essential for product approval and market entry. Companies must invest in certified facilities, quality control, and documentation processes. Regulatory oversight ensures product safety but can increase operational complexity and costs.

Analyst Perspective

The injection molding market continues to benefit from its position as one of the most versatile and cost-efficient manufacturing processes for producing complex components at scale. Demand remains closely tied to growth in packaging, automotive, consumer goods, healthcare, and electronics industries, where manufacturers increasingly require lightweight, durable, and precision-engineered parts. The market is also being influenced by broader industry trends such as automation, smart manufacturing, and sustainability, with processors investing in advanced molding technologies to improve productivity, reduce material waste, and enhance operational efficiency. While packaging remains a key demand driver, opportunities are expanding in high-value applications such as medical devices, electric vehicles, and electronic components. Looking ahead, the ability to process recycled and engineered materials, coupled with increasing demand for customized and high-performance products, is expected to strengthen the role of injection molding as a critical manufacturing technology across both mature and emerging industries.

Material Insights

Based on material, the plastics segment led the market with the largest revenue share of 98.2% in 2025., due to their lightweight, versatile, and cost-effective properties. They are widely used across automotive, packaging, consumer goods, and medical sectors. Advanced polymers and engineered plastics allow for complex designs and high-performance applications. Ongoing innovations in recyclable and bio-based plastics further strengthen their market position.

Metal injection molding (MIM) is emerging as the fastest-growing segment, driven by demand for high-strength, precision components. It is increasingly applied in medical devices, electronics, and aerospace industries. MIM enables complex shapes and high-volume production with excellent dimensional accuracy. Growth is supported by technological advancements and increasing adoption in specialized applications.

Application Insights

Based on application, the packaging segment led the market with the largest revenue share of 32.1% in 2025, driven by demand for lightweight, durable, and cost-effective solutions. Plastics are extensively used for food, beverage, and consumer product packaging. High-speed production and customizable designs make injection molding ideal for mass-market packaging needs. Sustainability trends, including recyclable and biodegradable materials, further support this segment.

The medical sector is the fastest-growing application area due to the increasing demand for precision components and disposable devices. Injection molding is widely used for syringes, diagnostic devices, surgical instruments, and drug delivery systems. Regulatory compliance, biocompatible materials, and high-quality standards drive specialized production. Technological advancements and rising healthcare expenditure continue to fuel growth in this segment.

Regional Insights

Asia Pacific dominated the injection molding market with the largest revenue share of 41.2% in 2025. Strong demand from the medical, automotive, and packaging industries supports market expansion. Adoption of automation and smart factory solutions enhances production efficiency. Strict regulatory standards ensure quality and reliability in manufactured components.

U.S. Injection Molding Market Trends

The U.S. dominates the North American injection molding market and accounted for 81.7% share, due to advanced manufacturing infrastructure and technological expertise. Strong demand from automotive, medical, and packaging sectors drives production. High adoption of automation and precision molding enhances efficiency and quality. Regulatory compliance and innovation in materials further strengthen market leadership.

Mexico is experiencing significant growth as a manufacturing hub for cost-effective injection-molded components. Expansion in automotive, electronics, and consumer goods industries fuels regional demand. Proximity to the U.S. market supports exports and supply chain integration. Investments in modern facilities and skilled labor contribute to steady market expansion.

Europe Injection Molding Market Trends

Europe’s market grows due to advanced engineering capabilities and a focus on sustainable production practices. The automotive and medical device sectors are key contributors to demand. Investment in Industry 4.0 technologies and high-quality manufacturing drives competitiveness. Regulatory compliance and innovation in materials further support growth.

Germany dominates the European injection molding market due to its strong industrial base and advanced engineering capabilities. High demand from the automotive, medical, and packaging sectors drives production. Investment in automation, precision molding, and Industry 4.0 technologies enhances efficiency and product quality. Regulatory standards and innovation in materials further reinforce Germany’s market leadership.

Italy is experiencing steady growth in injection molding, supported by the automotive, consumer goods, and packaging industries. Small and medium-sized enterprises play a key role in regional production. Adoption of modern manufacturing technologies improves productivity and precision. Government support and increasing exports contribute to Italy’s expanding market presence.

Asia Pacific Injection Molding Market Trends

Asia Pacific is the dominating region and accounts for 41.0% share in 2024 of the global injection molding market, driven by strong industrial growth, large-scale manufacturing, and a growing automotive and consumer goods sector. Countries like China and India drive demand with cost-effective production capabilities and abundant labor. Rapid urbanization and expanding infrastructure further boost market growth. Advanced manufacturing technologies and government support also reinforce the region’s dominance.

The injection molding market in China held the largest share in the Asia Pacific region in 2025. Strong demand from the automotive, electronics, and consumer goods sectors drives growth. Rapid industrialization and urbanization further boost the need for molded components. Investments in advanced machinery and automation enhance efficiency and product quality.

India is witnessing significant growth in injection molding, driven by expanding automotive, packaging, and consumer goods industries. Increasing foreign investment and the establishment of modern manufacturing facilities support market expansion. Adoption of advanced technologies, including automation and precision molding, improves productivity. Rising domestic demand and exports contribute to India’s growing market presence.

Middle East & Africa Injection Molding Market Trends

The Middle East and Africa market is growing due to industrialization, energy, and the construction sector demand. Healthcare and automotive applications are driving the adoption of molded components. Investment in automation and advanced manufacturing enhances production efficiency. Regional infrastructure development and industrial diversification support market growth.

Saudi Arabia dominates the Middle East & Africa injection molding market due to rapid industrialization and investments in advanced manufacturing. Strong demand from the construction, automotive, and energy sectors drives growth. Adoption of automation and precision molding technologies enhances production efficiency. Government initiatives and infrastructure development further support market expansion in the region.

Latin America Injection Molding Market Trends

Latin America shows increasing demand driven by industrial expansion and rising consumer product consumption. Automotive and packaging industries are major end-users of injection-molded components. Investments in modern facilities and machinery improve production capacity. The region benefits from growing urbanization and supportive government initiatives.

Brazil dominates the Latin American injection molding market due to its well-established industrial base and strong manufacturing capabilities. High demand from the automotive, packaging, and consumer goods sectors fuels market growth. Investment in modern machinery and automation enhances production efficiency and product quality. Supportive government policies and growing domestic consumption further strengthen Brazil’s market position.

Key Injection Molding Company Insights

Some of the key players operating in the market include C&J Industries, All-Plastics, and Biomerics.

-

C&J Industries specializes in high-precision plastic injection molding and contract manufacturing, serving diverse sectors such as medical devices, pharmaceuticals, telecommunications, industrial, consumer products, and transportation. The company is FDA registered and ISO 13485:2016 certified, ensuring compliance with stringent medical device manufacturing standards. Their capabilities include high cavitation molds, overmolding, and complex assemblies, catering to both low and high-volume production needs. C&J Industries also offers comprehensive services like product validation, sterilization packaging, and cleanroom manufacturing. Their expertise extends to producing components like syringes, bone graft filters, and pipette holders, demonstrating versatility across various applications.

-

All-Plastics is a Texas-based custom injection molder focusing on precision and scientific molding techniques. The company serves key industries including pharmaceuticals, medical devices, industrial, consumer products, and packaging. Their services encompass product and mold design, prototyping, tool building, and precision molding, utilizing advanced technologies like RJG eDART Quality Molding. All-Plastics has enhanced its capabilities with the addition of new injection molding machines, robots, and a white room for micro-component molding. The company emphasizes cost-effective solutions and on-time delivery, aiming to reduce manufacturing costs while improving product quality.

Key Injection Molding Companies

The following are the leading companies in the injection molding market.

-

C&J Industries

-

All-Plastics

-

Biomerics

-

HTI Plastics

-

The Rodon Group

-

EVCO Plastics

-

Majors Plastics, INC

-

Proto Labs

-

Tessy Plastics

-

Currier Plastics, Inc.

-

Formplast GmbH

-

H&K Müller GmbH & Co. KG

-

Hehnke GmbH & Co KG

-

TR PLAST GROUP

-

D&M Plastics, LLC

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (e.g., C&J Industries, Tessy Plastics, The Rodon Group)

- Mature players focus on high-volume production, operational efficiency, and long-term customer relationships across automotive, packaging, consumer goods, electronics, industrial, and healthcare sectors.

- Their strategies emphasize automation, capacity expansion, advanced molding technologies, and geographic diversification to support large-scale manufacturing programs and improve cost competitiveness.

- These companies benefit from extensive manufacturing footprints, established customer bases, broad material processing capabilities, and strong expertise in complex and high-volume molding applications.

- Their investments in automation, tooling, process optimization, and quality systems enable consistent production performance and scalability across multiple industries.

- Large-scale operations can result in higher fixed costs and reduced flexibility when serving niche or low-volume projects.

- Mature players are also more exposed to fluctuations in industrial production, automotive demand, and capital-intensive expansion cycles across major end-use sectors.

Emerging & Regional Players (e.g., Biomerics, Hehnke GmbH & Co KG, regional players)

- Emerging players typically pursue growth through specialization, customer-focused manufacturing solutions, and expansion into high-growth application areas.

- Many focus on precision molding, engineering plastics, rapid prototyping, low-to-medium volume production, and value-added services to differentiate themselves from larger competitors.

- These companies often demonstrate greater agility, faster response times, and stronger customization capabilities.

- Their ability to serve niche applications, support product development cycles, and adopt new materials or molding technologies quickly allows them to compete effectively in evolving market segments..

- Emerging players generally have smaller production capacities, more limited geographic reach, and fewer financial resources than established manufacturers.

- They may also face challenges in securing large-scale supply agreements and competing on cost in highly commoditized, high-volume molding applications.

Recent Developments

-

In May 2025, HTI Plastics will showcase its pharmaceutical injection molding expertise at CPHI North America 2025. The company specializes in high-precision, quality components for pharmaceutical applications. Their services include design, prototyping, and manufacturing of critical drug delivery and medical device parts. Attendees can visit Booth 1741 to explore HTI Plastics’ advanced capabilities.

-

In April 2025, C&J Industries increased its medical-grade plastic injection molding capacity by adding a 12,000-square-foot Class 8 cleanroom. The facility features all-electric Toshiba molding presses and automated 3-axis robots for efficient production and inspection. This expansion significantly boosts the company’s ability to supply high-quality medical components to meet growing demand.

-

In October 2024, Biomerics launched Metal Injection Molding (MIM) services, offering precision metal components for medical devices. The company provides end-to-end solutions, from design and prototyping to full-scale production. This expansion enhances quality, reduces lead times, and strengthens Biomerics’ capabilities for the medical industry.

Injection Molding Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 312.7 billion

Estimated market size in 2026

USD 327.5 billion

Projected market size by 2033

USD 462.5 billion

Growth rate

CAGR of 5.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, application, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Spain; Italy; China; India; Japan; Australia; South Korea; Brazil; Argentina; Saudi Arabia; UAE

Key companies profiled

C&J Industries, All-Plastics, Biomerics, HTI Plastics, The Rodon Group, EVCO Plastics, Majors Plastics, Inc., Proto Labs, Tessy Plastics, Currier Plastics, Inc., Formplast GmbH, H&K Müller GmbH & Co. KG, Hehnke GmbH & Co. KG, TR PLAST GROUP, D&M Plastics, LLC

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Injection Molding Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global injection molding market report based on material, application and region.

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastics

-

Metal

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Packaging

-

Consumables & Electronics

-

Automotive & Transportation

-

Building & Construction

-

Medical

-

Other

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

Italy

-

Spain

-

UK

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

UAE

-

-

Research Methodology

Segment Definition

Segment - Material

Revenue Capture Definition

Plastic

This segment captures revenue generated from injection molded components manufactured using thermoplastics, thermosets, engineering plastics, and specialty polymer materials. It represents the largest material category and serves applications across packaging, automotive, medical, consumer goods, electronics, and industrial sectors.

Metal

This segment comprises revenue generated from metal injection molded (MIM) components produced using metal powders and binders. The segment primarily serves applications requiring high strength, precision, and complex geometries across automotive, medical, industrial, aerospace, and electronics industries.

Others

This segment captures revenue generated from injection molded components manufactured using alternative materials such as rubber and ceramics. These materials are primarily utilized in applications requiring specialized properties including flexibility, wear resistance, thermal stability, electrical insulation, and chemical resistance.

Segment - End Use

Revenue Capture Definition

Packaging

This segment captures revenue generated from injection molded products used in packaging applications, including caps, closures, containers, dispensers, thin-wall packaging, and other packaging components for consumer and industrial products.

Consumables & Electronics

This segment comprises revenue generated from injection molded components used in consumer products, household goods, electrical devices, electronic housings, connectors, appliances, and related applications.

Automotive & Transportation

This segment includes revenue generated from injection molded parts supplied to automotive, commercial vehicle, rail, aerospace, and transportation industries for interior, exterior, structural, and functional applications.

Building & Construction

This segment captures revenue generated from injection molded products used in residential, commercial, and industrial construction applications, including fittings, fixtures, insulation components, conduits, and other building materials.

Pharmaceutical

This segment comprises revenue generated from injection molded products used in healthcare applications, including medical devices, diagnostic equipment, drug delivery systems, laboratory consumables, and disposable medical products.

Others

This segment comprises revenue generated from injection molded components supplied to aerospace & defense, personal care, marine, and safety equipment applications. Demand is driven by requirements for lightweight components, durability, precision manufacturing, product customization, and regulatory compliance across these end-use sectors.

Estimation Model

Layer Name

Key Question

Description

End-Use Demand Layer

Where is injection molding demand generated?

Analyze demand across key end-use industries including packaging, automotive, consumer goods, electronics, healthcare, construction, and industrial manufacturing. Assess production volumes of molded components, lightweight material adoption trends, and manufacturing output to establish the addressable demand base.

Manufacturing Capacity Expansion Layer

Where is new molding capacity being added?

Evaluate investments in manufacturing facilities, production line expansions, and new product development initiatives. Assess capacity additions by molders, OEMs, and contract manufacturers, along with regional industrialization trends and reshoring activities driving equipment and processing demand.

Material & Application Adoption Layer

Which materials and applications are driving market growth?

Segment demand by material type and application. Apply adoption rates for plastics, metals, and specialty materials across packaging, automotive, consumer goods, healthcare, and electronics sectors.

Revenue Layer

How is market revenue generated?

Estimate molded component production volumes by material and application. Apply average selling prices based on material type, part complexity, production scale, and end-use requirements.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Competitive Benchmarking

The report provided a competitive assessment of established injection molding companies, evaluating their relative positions based on manufacturing capacity, financial strength, service portfolio, geographic presence, end-use industry exposure, and strategic initiatives. The analysis also examined the competitive structure of the market and the contribution of major players across key application segments.

Enabled stakeholders to gain a comprehensive understanding of the competitive landscape, identify market leaders and emerging challengers, and benchmark performance against industry peers. The insights supported strategic decision-making related to partnerships, acquisitions, competitive positioning, and long-term growth planning.

Regional Segmentation

The study delivered an expanded regional analysis covering market size, manufacturing activity, end-use demand trends, material consumption patterns, and investment activity across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

The analysis provided insights into regional manufacturing hubs, evolving demand centers, and industry-specific growth drivers. It enabled stakeholders to evaluate geographic expansion opportunities, assess regional competitiveness, and prioritize investments in high-growth markets.

Opportunity Assessment

The report identified high-potential growth areas across materials, end-use industries, and geographic markets. The assessment evaluated emerging demand trends, evolving manufacturing requirements, technology adoption patterns, and application-specific developments influencing future market expansion.

The assessment helped clients identify attractive investment areas, evaluate future demand shifts, and align business strategies with emerging industry trends. It also provided actionable insights into segments expected to create new revenue opportunities over the forecast period.

Frequently Asked Questions About This Report

Some of the key players operating in the global injection molding market include C&J Industries, All-Plastics, Biomerics, HTI Plastics., The Rodon Group, EVCO Plastics, Majors Plastics, INC, Proto Labs, Tessy Plastics, Currier Plastics, Inc., Formplast GmbH, H&K Müller GmbH & Co. KG, Hehnke GmbH & Co KG, TR PLAST GROUP, D&M Plastics, LLC.

Rising demand for high-performance, durable, and lightweight chemical-resistant components drives market growth. Advancements in precision molding, automation, and specialized materials enhance efficiency and product quality. Expanding applications across automotive, healthcare, and industrial sectors further fuel global adoption.

Asia Pacific is anticipated to be one of the fastest-growing regional markets over the forecast period, supported by expanding manufacturing activities, rising consumer goods production, and increasing industrial investments.

The plastics segment led the market with the largest revenue share of 98.2% in 2025.

The packaging segment accounted for the largest revenue share of 32.1% in 2025.

Key trends include increasing adoption of automation and smart manufacturing technologies, growing use of recycled and bio-based materials, rising demand for lightweight components, and advancements in precision molding capabilities.

The global injection molding market size was estimated at USD 312.7 billion in 2025 and is expected to be USD 327.5 billion in 2026.

The global injection molding market, in terms of revenue, is expected to grow at a compound annual growth rate of 5.1% from 2026 to 2033 to reach USD 462.5 billion by 2033.

Asia Pacific dominated the injection molding market with the largest revenue share of 41.2% in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.