- Home

- »

- Biotechnology

- »

-

Immune Cell Engineering Market Size Report, 2026-2033GVR Report cover

![Immune Cell Engineering Market (2026 - 2033)Report]()

Immune Cell Engineering Market (2026 - 2033)

Size, Share & Trends Analysis Report By Cell Type (T Cells, NK Cells, Dendritic Cells, Tumor Cells, Stem Cells), By Product (Consumables, Instruments, Software), By Disease Indication, By End-use, By Region, And Segment Forecasts

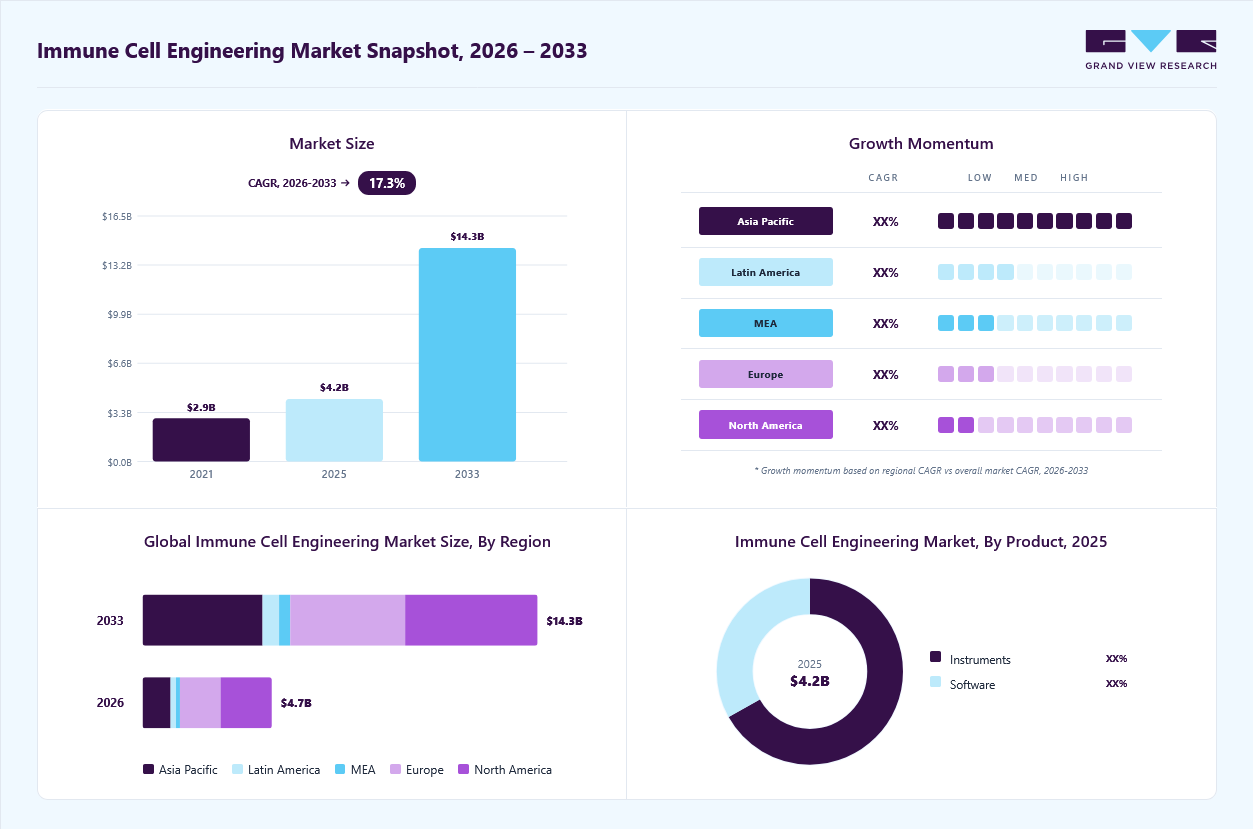

Market Size, 2025

$4.2BMarket Estimate, 2026

$4.7BMarket Forecast, 2033

$14.3BCAGR, 2026–2033

17.3%Immune Cell Engineering Market Summary

The global immune cell engineering market size was valued at USD 4.2 billion in 2025 and is projected to grow from USD 4.7 billion in 2026 to USD 14.3 billion by 2033, at a CAGR of 17.3% from 2026 to 2033. The market in North America dominated with a revenue share of 40.2% in 2025. This growth is driven by the increasing adoption of engineered immune cell therapies for cancer and autoimmune disease treatment, rising investments in cell and gene therapy research, and continuous advancements in technologies such as CRISPR and CAR-T cell engineering.

Key Market Trends & Insights

- By product: Consumables segment held the largest market share of 54.4% in 2025.

- By end-use: Pharmaceutical & biotechnology companies segment held the largest market share of 44.9% in 2025.

- By cell type: T cells segment held the largest market share of 41.2% in 2025.

- By disease indication: Cancer segment held the largest market share of 41.2% in 2025.

Regional Highlights

- Largest regional market: North America (40.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 4.2 Billion

- Estimated market size in 2026: USD 4.7 Billion

- Projected market size by 2033: USD 14.3 Billion

- CAGR (2026-2033): 17.3%

")

Advancements in Gene-Editing and Cell Therapy Technologies

Advancements in gene-editing and cell therapy technologies are driving the immune cell engineering market by enabling more precise and personalized immunotherapies. Tools such as CRISPR-Cas9, TALENs, and improved viral and non-viral delivery systems enhance the genetic modification of immune cells, such as T cells and NK cells, thereby improving their ability to target cancer cells. In addition, innovations in CAR-T and TCR-T therapies are increasing treatment efficacy, reducing off-target effects, and expanding applications to solid tumors and autoimmune diseases.

The current state of cell and gene therapies

Category

Details

Total CGT approvals

76 CGTs have been launched globally

Key therapeutic focus

Mainly cancer and rare diseases; expanding into broader indications

Recent therapeutic expansion

New CGTs developed for type 1 diabetes (Lantidra) and Duchenne muscular dystrophy (Elevidys) in 2023

Market outlook

The CGT market is expected to exceed USD 40 billion by 2027

FDA approval trend

~10% of all FDA new approvals in 2023 were CGTs, rising from 2021-2022 levels

UK market trend

Approved CGTs increased from 11 (2023) to 14 (2024)

Regulatory insight (UK)

UK is recognized as a key hub for CGT development and commercialization

Recent approvals

Includes therapies for hematological malignancies and hemophilia A

Landmark approval

Casgevy (CRISPR-Cas9-based therapy) approved by MHRA for β-thalassemia and sickle cell disease

Technology milestone

First global approval of a CRISPR-based gene-editing therapy (Casgevy)

Source: News Medical Lifesciences, Secondary Research, Grand View Research

A research study published in Nature in September 2025 further demonstrated significant progress in this field, particularly through CRISPR-enhanced CAR-T cell therapies that showed improved tumor targeting and longer persistence in patients. These developments are strengthening treatment precision and durability, making immune cell-based therapies more effective for difficult-to-treat cancers and supporting the overall expansion of the market.

Expanding Clinical Trials for Engineered Immune Cell Therapies

Expanding clinical trials for engineered immune cell therapies are driving the growth of the immune cell engineering market. Increasing research into CAR-T, CAR-NK, TCR-T, and other engineered immune cell therapies is accelerating the development of advanced treatments for cancer, autoimmune disorders, and infectious diseases. Pharmaceutical and biotechnology companies are increasingly investing in clinical studies to evaluate the safety, efficacy, and long-term therapeutic potential of these therapies, which further supports innovation and product development in the market.

Moreover, the growing number of clinical trials focused on solid tumors and hematological malignancies is broadening the scope of application for immune cell engineering while supporting regulatory approvals and commercialization. For instance, a research study published in Springer Nature in March 2025 highlighted a global pipeline of more than 120 CAR-NK clinical trials targeting cancer and autoimmune diseases, reflecting the rising research activity and investment in next-generation immune cell therapies.

Market Concentration & Characteristics

The immune cell engineering industry is characterized by high innovation in gene-editing technologies, cell modification platforms, and manufacturing processes. Advanced technologies such as CRISPR-Cas9, CAR-T, CAR-NK, and non-viral gene delivery systems are improving the precision, efficacy, and scalability of engineered immune cell therapies. In addition, the growing focus on allogeneic “off-the-shelf” therapies and automated cell manufacturing platforms is accelerating the development of cost-effective and personalized immunotherapies. These innovations are reducing production timelines, enhance treatment safety, and expand therapeutic applications beyond hematological cancers to solid tumors and autoimmune diseases.

The immune cell engineering industry is experiencing moderate to high levels of mergers and acquisitions, driven by growing demand for advanced cell therapy technologies, expansion of immunotherapy pipelines, and strengthening of research and manufacturing capabilities. Companies are increasingly engaging in strategic acquisitions and collaborations to deepen their expertise in gene editing, CAR-T and CAR-NK therapies, in vivo cell engineering, and RNA delivery technologies. These activities also support the development of scalable, cost-effective immune cell therapies while accelerating clinical development and commercialization. For instance, in June 2025, AbbVie acquired Capstan Therapeutics for up to USD 2.1 billion to strengthen its immunology portfolio through in vivo CAR-T therapies and targeted lipid nanoparticle (tLNP) RNA delivery technologies for autoimmune diseases.

Regulations significantly influence the immune cell engineering industry by guiding therapy development pathways, manufacturing standards, clinical trial approvals, and commercialization processes. Compliance with GMP, FDA, EMA, and other regulatory guidelines ensures the safety, efficacy, and consistency of engineered immune cell therapies, including CAR-T and CAR-NK treatments. Although stringent regulations increase development costs and approval timelines, they improve product reliability, support global market access, and encourage innovation in standardized and safer immune cell engineering technologies.

Product expansion in the immune cell engineering industry is driven by increasing demand for advanced, personalized immunotherapies for cancer and autoimmune diseases. Companies are expanding their portfolios with next-generation CAR-T, CAR-NK, TCR-T, and allogeneic “off-the-shelf” cell therapies to improve treatment efficacy, scalability, and accessibility. In addition, the growing focus on non-viral engineering technologies and simplified manufacturing workflows is accelerating innovation in immune cell therapy development. For instance, in January 2025, CellFE launched T-Rest, a first-in-class resting T cell kit designed for non-viral CAR-T cell manufacturing workflows, supporting safer and more potent cell therapy development through improved gene-editing efficiency and streamlined manufacturing processes.

The immune cell engineering industry expansion is driven by the growing adoption of advanced immunotherapies, rising clinical research activity, and increasing investments in cell and gene therapy infrastructure across both developed and emerging regions. Leading companies are strengthening their presence in high-growth regions such as Asia-Pacific, Latin America, and the Middle East & Africa through strategic collaborations, manufacturing expansions, and clinical trial initiatives to address rising demand and comply with regional regulatory requirements. Expansion into these markets enables companies to leverage improvements in healthcare infrastructure, rising cancer prevalence, and growing government support for advanced therapy development, while enhancing patient access to innovative immune cell therapies.

Cell Type Insights

The T cells segment accounted for the largest market share of 41.2% in 2025 and is expected to maintain its dominance over the forecast period. This growth is primarily driven by the global adoption of T cell-based engineering approaches, particularly CAR-T and TCR-T therapies, for the treatment of cancer and autoimmune diseases. T cells are globally used in immune cell engineering due to their strong tumor-targeting ability, long-term persistence, and proven effectiveness in cancer treatment. In addition, rising investments in T cell therapy research, expanding clinical trials, and advancements in gene-editing and cell manufacturing technologies are supporting segment growth.

The NK cells segment is expected to grow at the fastest CAGR during the forecast period, driven by increasing interest in NK cell-based immunotherapies for cancer treatment. NK cells offer advantages such as a lower risk of graft-versus-host disease, strong anti-tumor activity, and the potential to develop allogeneic “off-the-shelf” therapies, which support broader clinical application and scalability. In addition, growing investments in CAR-NK research, expanding clinical trials, and advancements in gene-editing and cell expansion technologies are further accelerating segment growth.

Product Insights

The consumables segment dominated the market in 2025 with an 54.4% share and is also expected to grow at the fastest CAGR during the forecast period, driven by the high demand for reagents, media, cytokines, antibodies, and gene-editing materials used in immune cell engineering workflows. The increasing development of CAR-T, CAR-NK, and TCR-T therapies, along with rising clinical trials and cell therapy manufacturing activities, continues to support segment growth.

The instruments segment is expected to grow significantly over the forecast period, driven by the increasing adoption of automated cell processing systems, flow cytometry instruments, cell sorters, and gene-editing platforms in immune cell engineering workflows. The growing focus on personalized immunotherapies and large-scale cell therapy manufacturing is increasing demand for advanced instruments that improve precision, scalability, and workflow efficiency, thereby supporting broader adoption of immune cell engineering technologies across research and clinical applications.

Disease Indication Insights

The cancer segment dominated the market in 2025 with a share of 41.2% and is also expected to grow at the fastest CAGR from 2026 to 2033, driven by the increasing adoption of engineered immune cell therapies such as CAR-T, CAR-NK, and TCR-T for cancer treatment. The rising global burden of cancer, growing demand for personalized immunotherapies, and expanding number of clinical trials for hematological malignancies and solid tumors are significantly supporting segment growth. In addition, advancements in gene-editing technologies and increasing regulatory approvals for cell-based cancer therapies continue to strengthen the segment’s leading position.

The neurological diseases segment is expected to grow significantly over the forecast period, driven by increasing research into engineered immune cell therapies for neurodegenerative and neuroinflammatory disorders. The growing ability of immune cell engineering technologies to modulate immune responses and target disease-specific pathways has expanded their application in neurological disease research and the development of treatments, supporting segment growth.

End-use Insights

The pharmaceutical & biotechnology companies segment dominated the market in 2025 with a 44.9% share and is also expected to grow at the fastest CAGR during the forecast period. The growth can be attributed to the increasing investments in cell and gene therapy research and the growing development of engineered immune cell therapies for cancer and autoimmune diseases. In addition, strategic collaborations, rising R&D expenditure, and advancements in gene-editing and cell manufacturing technologies continue to strengthen the segment’s leading position.

The hospitals & clinics segment is expected to grow significantly over the forecast period, driven by the increasing adoption of immune cell engineering technologies in cancer immunotherapy, regenerative medicine, and personalized treatment approaches. Hospitals and clinical centers are expanding their capabilities in CAR-T cell therapy, stem cell transplantation, and engineered immune cell-based therapies to improve patient outcomes. In addition, rising clinical trials, increasing healthcare investments, and growing collaborations with biotechnology and pharmaceutical companies are accelerating segment growth in the immune cell engineering market.

Regional Insights

North America immune cell engineering market dominated the global market, accounting for 40.2% in 2025, driven by advanced healthcare infrastructure, strong investments in cell and gene therapy research, and the presence of leading biotechnology and pharmaceutical companies with established manufacturing capabilities. High adoption of CAR-T and other engineered immune cell therapies, increasing clinical trial activity, and growing focus on personalized immunotherapies have strengthened the region’s position as a major innovation hub for immune cell engineering technologies.

U.S. Immune Cell Engineering Market Trends

The U.S. immune cell engineering market is highly competitive and innovation-driven, supported by a strong life sciences ecosystem and increasing adoption of advanced cell and gene therapy technologies. The market is strongly focused on CAR-T, CAR-NK, TCR-T, and gene-editing platforms for cancer and autoimmune disease treatment. Rising prevalence of chronic diseases, increasing regulatory approvals for cell-based therapies, and significant investments in precision medicine and immunotherapy research continue to support market growth and technological advancement in the country.

Europe Immune Cell Engineering Market Trends

The Europe immune cell engineering market is witnessing rapid growth, driven by increasing investments in CAR-T, gene editing, and personalized immunotherapy research, along with strong government and institutional support for advanced cancer therapies. The region is also benefiting from rising collaborations between research institutes and biotechnology companies to accelerate innovation in immune cell engineering. For instance, in November 2025, the European Research Council awarded EUR 14 million to the Europe-led PRECISION-ImmunoRad project, which aims to advance CAR-T cell engineering, ion-beam therapy, and personalized cancer vaccines for therapy-resistant solid tumors.

Immune cell engineering market the UKis driven by a strong focus on translational research and increasing integration of cell and gene therapies into healthcare and clinical research. The growing adoption of CAR-T therapies, rising investments in immuno-oncology, and expanding collaborations among academic institutions, research organizations, and biotechnology companies are supporting market growth and innovation in immune cell engineering technologies.

The Germany immune cell engineering market is experiencing robust growth, supported by strong research capabilities and a well-established biotechnology ecosystem. Increasing adoption of CAR-T, CAR-NK, and gene-editing technologies across research and clinical settings, along with rising investments in cancer immunotherapy and cell therapy manufacturing infrastructure, is further driving market growth.

Asia Pacific Immune Cell Engineering Market Trends

Asia-Pacific is expected to witness the fastest growth, with a CAGR of 23.1% during the forecast period, driven by rising investments in cell and gene therapy research, expanding healthcare infrastructure, and increasing adoption of personalized immunotherapies. Growing demand for CAR-T, CAR-NK, and iPSC-derived immune cell therapies, along with increasing clinical research activities and advancements in off-the-shelf cell therapy platforms, is further supporting regional market growth. For instance, in September 2025, Cartherics received the “Most Promising iPSC Therapy Pipeline in Asia Pacific” award for advancing off-the-shelf iPSC-derived NK cell therapies targeting ovarian cancer, endometriosis, and other solid tumors.

Immune cell engineering market in China is growing rapidly, driven by rising investment in biotechnology, immuno-oncology, and cell & gene therapy research. The increasing demand for advanced cancer immunotherapies, such as CAR-T, is driving the adoption of scalable, automated cell engineering platforms. Strong government support for precision medicine and the expanding domestic biopharma industry are further accelerating market growth.

The Japan immune cell engineering market is advancing due to a well-established clinical research ecosystem and early adoption of regenerative and cell-based therapies. Increasing integration of AI-enabled bioprocessing and closed-system manufacturing is enhancing production precision and reducing variability. Strong regulatory support for regenerative medicine and rising clinical application of engineered immune cells are further supporting market expansion.

Middle East & Africa Immune Cell Engineering Market Trends

The MEA immune cell engineering market is gradually expanding due to improving healthcare infrastructure and rising focus on advanced cancer therapies. Increasing collaborations with global biotech companies and growing investments in biomanufacturing are supporting technology adoption.

Immune cell engineering market in Kuwait is witnessing steady growth, driven by healthcare investments and rising adoption of cancer immunotherapies. Government support for precision medicine and expanding biotechnology research is further supporting market growth.

Key Immune Cell Engineering Company Insights

The immune cell engineering market is characterized by established biotechnology and life sciences companies competing through advanced technology platforms and expanding cell therapy portfolios. Major players such as Thermo Fisher Scientific Inc., Merck KGaA, Danaher Corporation, Lonza, and Miltenyi Biotech maintain strong market positions through extensive manufacturing capabilities, broad product offerings, and investments in gene-editing and automated cell-processing technologies.

In addition, companies such as Takara Bio Inc., Sartorius AG, Agilent Technologies, Inc., Bio-Techne, and Bio-Rad Laboratories, Inc. are strengthening their market presence by offering specialized solutions for immune cell isolation, cell expansion, gene delivery, and analytical workflows. Their focus on innovation, strategic collaborations, and support for research and clinical applications enables them to gain traction alongside established market leaders.

Market leaders in the immune cell engineering market maintain their dominance by leveraging advanced technologies such as CRISPR-based gene editing, CAR-T and CAR-NK engineering platforms, automated cell manufacturing systems, and high-throughput analytical tools. Their market position is further supported by strong investments in research and development, strategic partnerships, and expanding clinical pipelines to improve the safety, efficacy, and scalability of immune cell therapies.

Key Immune Cell Engineering Companies:

The following key companies have been profiled for this study on the immune cell engineering market.

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Danaher Corporation

- Lonza

- Miltenyi Biotec

- Takara Bio Inc.

- Sartorious AG

- Agilent Technologies, Inc.

- Bio-Techne

- Bio-Rad Laboratories, Inc.

Recent Developments

-

In March 2026, Gilead Sciences acquired Ouro Medicines to strengthen its inflammation portfolio by advancing a BCMAxCD3 T cell engager therapy for autoimmune diseases. The deal aimed to accelerate the development of immune reset-based treatments offering durable remission and improved clinical outcomes.

-

In February 2026, Eli Lilly acquired Orna Therapeutics to advance in vivo CAR-T and circular RNA-based cell therapies targeting B-cell-driven autoimmune diseases. The acquisition aimed to strengthen genetic medicine capabilities and expand innovative immune cell engineering platforms.

"Early autologous CAR-T studies have shown the promise of cell therapy for patients with autoimmune diseases, but the complexity, cost, and logistics of ex vivo approaches make it challenging to deliver these breakthroughs to the broader population of patients who need them"

-Francisco Ramírez-Valle, M.D., Ph.D., Senior Vice President, Head of Immunology Research and Early Clinical Development.

Immune Cell Engineering Market Report Scope

Report Attribute

Details

Market size in 2025

USD 4.2 billion

Estimated market size in 2026

USD 4.7 billion

Projected market size by 2033

USD 14.3 billion

Growth rate

CAGR of 17.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Cell type, product, disease indication, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; India; China; Japan; Australia; South Korea; Thailand; Brazil; Argentina; Saudi Arabia; UAE; South Africa; Kuwait

Key companies profiled

Thermo Fisher Scientific Inc.; Merck KGaA; Danaher Corporation; Lonza; Miltenyi Biotec; Takara Bio Inc.; Sartorious AG; Agilent Technologies, Inc.; Bio-Techne; Bio-Rad Laboratories, Inc.

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Immune Cell Engineering Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global immune cell engineering market report based on cell type, product, disease indication, end-use, and region:

-

Cell Type Outlook (Revenue, USD Million, 2021 - 2033)

-

T Cells

-

NK Cells

-

Dendritic Cells

-

Tumor Cells

-

Stem Cells

-

Others

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumables

-

Instruments

-

Software

-

-

Disease Indication Outlook (Revenue, USD Million, 2021 - 2033)

-

Cardiovascular Diseases

-

Respiratory Diseases

-

Infectious Diseases

-

Cancer

-

Neurological Diseases

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Pharmaceutical & Biotechnology Companies

-

Hospitals & Clinics

-

Academic & Research Institutes

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

T cells segment led with a 41.2% revenue share in 2025, while NK cells is the fastest-growing type.

The consumables segment led with a 54.4% revenue share in 2025, and is the fastest-growing product.

The cancer segment led with a 41.2% revenue share in 2025, and is the fastest-growing disease indication.

Pharmaceutical & biotechnology companies segment held the largest share (over 44.0%) in 2025, and is the fastest-growing segment.

The growth is driven by the increasing adoption of engineered immune cell therapies for cancer and autoimmune disease treatment, rising investments in cell and gene therapy research, and continuous advancements in technologies such as CRISPR and CAR-T cell engineering.

The global immune cell engineering market size was valued at USD 4.2 billion in 2025 and is estimated at USD 4.7 billion for 2026.

The global immune cell engineering market is expected to grow at a CAGR of 17.3% from 2026 to 2033, reaching USD 14.3 billion by 2033.

North America dominated the immune cell engineering market, accounting for 40.2% in 2025, driven by advanced healthcare infrastructure, strong investments in cell and gene therapy research, and the presence of leading biotechnology and pharmaceutical companies with established manufacturing capabilities.

Key players include Thermo Fisher Scientific Inc.; Merck KGaA; Danaher Corporation; Lonza; Miltenyi Biotec; Takara Bio Inc.; Sartorious AG; Agilent Technologies, Inc.; Bio-Techne; Bio-Rad Laboratories, Inc.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.