- Home

- »

- HVAC & Construction

- »

-

Excavator Attachments Market Size Report, 2026-2033GVR Report cover

![Excavator Attachments Market (2026 - 2033)Report]()

Excavator Attachments Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Steel, Rubber, Polyurethane, High-Strength Composite Materials, Advanced Alloys), By Attachment Type (Buckets, Couplers), By Excavator Size, By Region, And Segment Forecasts

Market Size, 2025

$8.7BMarket Estimate, 2026

$9.2BMarket Forecast, 2033

$14.8BCAGR, 2026–2033

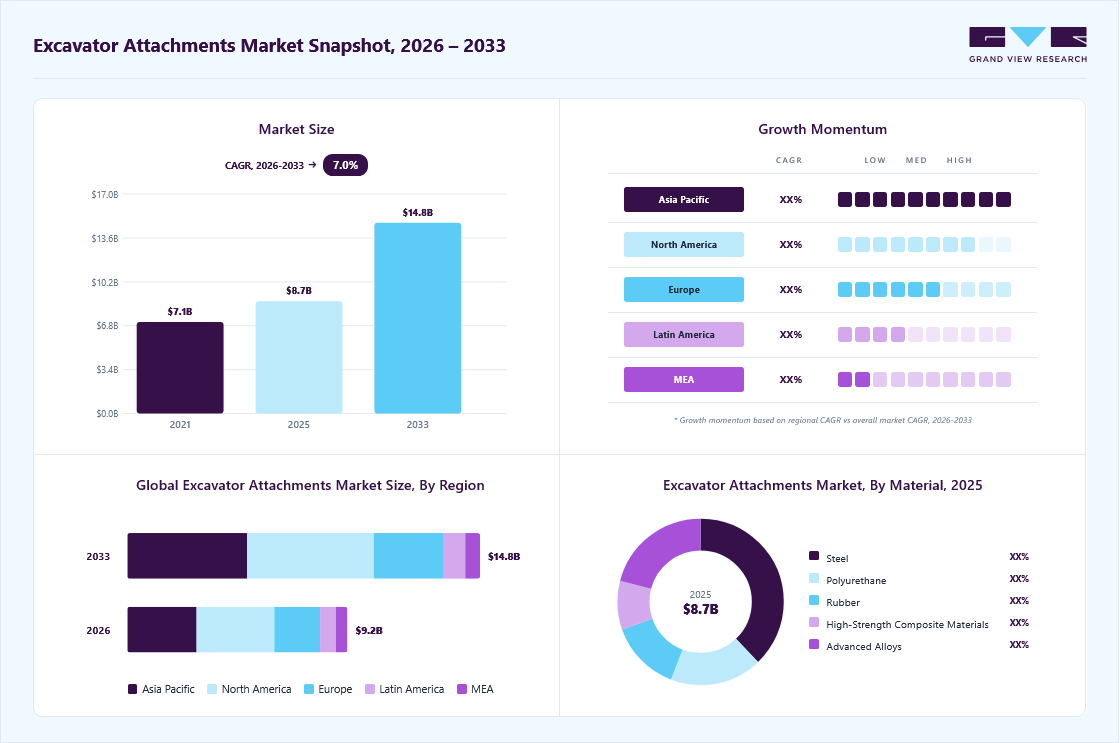

7.0%Excavator Attachments Market Summary

The global excavator attachments market size was valued at USD 8.7 billion in 2025 and is projected to grow from USD 9.2 billion in 2026 to USD 14.8 billion by 2033, at a CAGR of 7.0% from 2026 to 2033. The market in North America dominated with a revenue share of 35.3% in 2025. Rapid growth in the global construction sector is driving demand for excavator attachments, including buckets, hammers, grapples, couplers, and other tools.

Key Market Trends & Insights

- By material: Steel segment held the largest market share of 37.8% in 2025.

- By attachment type: Buckets segment held the largest market share in 2025.

- By excavator size: Medium-sized excavator (15-30t) segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (35.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 8.7 Billion

- Estimated market size in 2026: USD 9.2 Billion

- Projected market size by 2033: USD 14.8 Billion

- CAGR (2026-2033): 7.0%

These attachments are essential for a wide range of construction activities, such as digging, material handling, demolition, and site preparation. The market growth can be attributed to the increasing demand for versatile, multi-functional equipment. Excavator attachments allow operators to perform tasks such as digging, lifting, drilling, and demolition, by reducing the need for multiple machines and improving equipment utilization. In addition, the expansion of the construction equipment rental market is further supporting market growth, as rental companies prefer machines compatible with multiple attachments to cater to diverse project requirements. This trend improves operational efficiency and enables end users to run various applications.")

Technological advancements play a critical role in transforming the market, with a strong focus on telematics, artificial intelligence, electric and hybrid attachments, and advanced sensor technologies. The integration of telematics enables real-time monitoring of attachment performance, location, and usage, thus improving fleet management and predictive maintenance. AI is increasing precision and control, allowing operators to complete complex tasks with greater accuracy. Furthermore, the industry is also adopting electric and hybrid attachments to reduce emissions, noise, and fuel consumption. Moreover, advanced sensors provide real-time feedback on soil conditions, attachment positioning, and obstacles, thereby increasing safety and operational decisions.

The market continues to grow as manufacturers expand their product portfolios to meet changing customer needs and improve equipment versatility. Companies are introducing advanced, application-specific excavator attachments across various sizes and industries to strengthen their market position. For instance, in June 2025, Geith International Ltd., a manufacturer of premium-quality excavator attachments, launched a 1-2T tilting quick coupler, expanding its range to seven models for excavators weighing 1-25 tonnes. This move addresses rising demand for hydraulic and tilting couplers, especially in Australia, the UK, France, and Spain, where adoption has shifted from pin-on buckets to manual, hydraulic, and now tilting quick couplers. The new attachment offers 180° tilting (90° in each direction), making it ideal for landscaping and construction in confined spaces. Such initiatives are expected to support the overall market growth.

The regulatory landscape plays a crucial role in shaping the market by establishing stringent safety and compliance standards for its design and operation. Regulatory authorities and industry bodies are prioritizing risk reduction, especially accidental detachment, by requiring secure locking mechanisms, fail-safe systems, and regular inspections. For instance, in February 2025, ISO 13031:2016/Amd 1:2025 regulation was updated to strengthen safety requirements for quick couplers used in earth-moving machinery. The amendment introduced automatic mechanical locking systems, operator warning alerts, and lift-prevention mechanisms to ensure that attachments are securely engaged before use. Thus, regulatory changes are raising operational safety standards, reducing workplace accidents, and prompting manufacturers to adopt advanced safety and monitoring features.

The market faces several export-related challenges that affect global trade efficiency and supplier competitiveness. International buyers and suppliers encounter logistical, regulatory, and commercial barriers that directly impact delivery timelines, cost structures, and long-term partnerships. For instance, compliance with regional regulations remains a critical challenge, as different markets require specific certifications such as CE conformity in Europe, local safety standards in the Middle East, and customs documentation in Africa and Latin America. In addition, the heavy, oversized, and irregular design of attachments creates complexities in container optimization, port handling, and inland transportation, often increasing transit time and risk, particularly in landlocked or developing regions. Such challenges are expected to increase operational complexity and may limit market expansion globally.

Market Dynamics

Growing mining and quarrying activities are significantly driving the market as global demand for minerals, aggregates, and construction raw materials continues to rise. Mining and quarrying operations rely heavily on excavators equipped with multiple attachments such as buckets, breakers, rippers, and grapples to perform tasks including excavation, material extraction, and loading. The rising need for operational efficiency in harsh, high-volume environments is prompting operators to adopt advanced attachments that improve productivity and reduce equipment changeover time.

Many countries are undertaking mining expansion and modernization projects, which are increasing the use of high-capacity excavators with advanced hydraulic attachments for large-scale mineral extraction. For instance, in May 2026, Elevra Lithium Limited announced the expansion of its North American Lithium (NAL) mine to significantly emphasize annual concentrate production. This development highlights the growing global focus on scaling critical mineral output, thereby driving higher deployment of advanced excavator attachments in large-scale mining operations.

The upfront investment required for advanced attachments, such as quick couplers and hydraulic systems, is relatively high due to complex engineering, precision manufacturing, and the use of durable materials. This may limit adoption, particularly among small- and medium-sized contractors operating under limited budget constraints.

In addition, ongoing maintenance expenses further add to the total cost of ownership. Regular servicing, replacement of worn components, and maintenance of hydraulic systems increase operational costs over time. These combined financial burdens make it difficult for some end users to justify large-scale adoption, thereby restraining market growth in certain cost-sensitive segments.

The growing focus on sustainability in construction and mining operations presents a significant opportunity for the market. Increasing environmental regulations and corporate sustainability goals are driving demand for eco-friendly and energy-efficient attachment solutions that reduce fuel consumption, emissions, and overall environmental impact during operations. Thus, manufacturers are developing lightweight, durable, and low-emission compatible attachments to support greener construction practices.

In addition, the rising adoption of electric and hybrid excavators is accelerating the need for sustainable attachment systems optimized for lower energy use and higher efficiency. Recyclable materials, reduced hydraulic leakage designs, and improved operational efficiency features are becoming key areas of innovation. Thus, eco-friendly excavator attachments are expected to gain significant adoption across infrastructure, mining, and urban development projects worldwide.

Market Concentration & Characteristics

The excavator attachments industry is moderately fragmented, with global, regional, and local manufacturers competing across various categories. Major companies, including Caterpillar Inc., Komatsu Ltd., and Epiroc AB, maintain significant market shares through broad product portfolios and strong dealer networks. Competition remains intense as specialized manufacturers target niche applications, including demolition, recycling, forestry, trenching, and material handling. The availability of customized products and aftermarket solutions further fragments the market.

The market is driven by ongoing technological innovation, increased adoption of hydraulic and smart attachments, and rising demand for multifunctional equipment in construction and mining. Global demand is further supported by infrastructure development and large-scale excavation projects. Thus, manufacturers are prioritizing quick-coupler systems, fuel-efficient designs, telematics integration, and enhanced durability to improve efficiency and minimize downtime. Moreover, strategic partnerships among OEMs and equipment rental companies are expanding the market, while evolving emissions and safety regulations are prompting the development of advanced, environmentally compliant solutions.

Material Insights

The steel segment dominated the market in 2025 and accounted for the largest share of 37.80%. The segment growth is primarily driven by the availability of different grades of high-strength and alloy steel, which enable manufacturers to improve product performance while maintaining structural integrity under demanding operating conditions. In addition, its superior strength and durability make it highly suitable for heavy-duty applications, as it can withstand high-impact forces, heavy loads, and abrasive environments commonly encountered in construction and mining activities, thereby ensuring extended service life and reliable performance.

The advanced alloys segment is expected to grow at a substantial CAGR during the forecast period. The segment growth is attributed to increasing demand for high-performance materials that offer enhanced strength-to-weight ratios and improved resistance to wear, corrosion, and extreme operating conditions. These materials are increasingly being adopted in excavator attachments to improve efficiency and extend service life, particularly in demanding applications such as mining and heavy construction. In addition, ongoing advancements in material engineering and metallurgy are enabling the development of more durable and specialized alloy compositions, further supporting their adoption across a wide range of high-intensity applications.

Excavator Size Insights

The medium-sized excavator (15-30t) segment accounted for the largest market share in 2025. The segment growth is propelled by its versatility across multiple applications and its ability to handle heavy-duty operations efficiently. These excavators are widely used in construction, mining, and infrastructure projects, as they offer sufficient power for demanding tasks while remaining adaptable for various attachment types, thus enabling operators to perform multiple functions with a single machine. In addition, their high productivity and operational efficiency make them a preferred choice for large and mid-scale projects, as they can manage substantial workloads with reduced downtime, thereby increasing demand for compatible attachments.

The mini excavator (below 6t) segment is expected to grow at the fastest CAGR during the forecast period. The segment growth is driven by the rising demand for compact equipment in urban and space-constrained environments, along with increasing adoption in landscaping and utility applications. Mini excavators are particularly well-suited for operations in narrow construction sites and residential areas where larger machines are not feasible, thus contributing to their growing adoption. Furthermore, their expanding use in landscaping and utility work, such as trenching, digging, and site preparation, is further supporting segment growth. This trend is driving strong demand for compatible and versatile excavator attachments.

Attachment Type Insights

The buckets segment dominated the market in 2025. The segment growth is attributed to its broad applicability across core construction and excavation activities, including digging, trenching, grading, and material handling. Buckets are considered fundamental attachments in both construction and mining operations due to their versatility and continuous usage across projects of varying scales, from small residential developments to large infrastructure projects. In addition, the availability of multiple bucket types, such as general-purpose, heavy-duty, rock, and ditching buckets, enables operators to select attachments based on specific soil conditions and operational requirements. This flexibility, combined with their cost-effectiveness and ease of use, further strengthens their dominant position in the market.

The hammers segment is expected to grow at a substantial CAGR during the forecast period. The increasing demand for demolition, mining, and infrastructure redevelopment across both developed and emerging economies is driving the segment growth. Hydraulic hammers are essential for breaking concrete, rocks, and other hard materials, thus making them widely used in applications such as road construction and urban redevelopment. In addition, the growing focus on upgrading infrastructure and expanding transportation networks is further increasing adoption, as these projects require efficient and high-performance breaking equipment to shorten project timelines and improve operational efficiency.

Regional Insights

North America dominated the excavator attachments market and accounted for a share of 35.26% in 2025. The region’s growth is propelled by rising demand for advanced construction equipment and the rapid adoption of technology-driven solutions such as smart attachments, telematics integration, and automated coupling systems that enhance operational efficiency and safety. Rising large-scale infrastructure development is further driving the demand for advanced excavator attachments across the region. For instance, large-scale infrastructure initiatives such as the U.S. Infrastructure Investment and Jobs Act (also known as the Bipartisan Infrastructure Law) are encouraging the use of efficient, versatile equipment, thereby emphasizing demand for advanced excavator attachments across construction and public works projects.

U.S. Excavator Attachments Market Trends

The excavator attachments market in the U.S. held a dominant position in the region in 2025. The country’s adoption of excavator attachments is driven by increasing use of rental equipment and the growing preference for multi-attachment solutions among contractors to improve cost efficiency and operational flexibility. Ongoing highway expansion and urban redevelopment projects in states such as Texas and California are further driving demand for excavator attachments. For instance, the High-Speed Rail Project in California is increasing the use of specialized attachments such as hydraulic hammers and grapples, thereby enabling faster project execution and improved on-site productivity.

Asia Pacific Excavator Attachments Market Trends

The excavator attachments market in the Asia Pacific is expected to grow at the fastest CAGR during the forecast period. The region’s growth is propelled by rapid urbanization and large-scale infrastructure development across emerging economies such as China and India. Governments in the region are increasingly investing in transportation networks, smart cities, and energy projects, which is significantly increasing the demand for construction equipment and compatible attachments. For instance, ongoing initiatives such as India’s Smart Cities Mission, which aim to improve the quality of life in 100 cities by providing efficient services and robust infrastructure, are accelerating the adoption of advanced, versatile excavator attachments.

China excavator attachments market held a significant market share in 2025. The country’s strong manufacturing base and the presence of domestic equipment producers are enabling the widespread availability of cost-effective and application-specific excavator attachments. In addition, ongoing national infrastructure programs and expansion of transportation networks are contributing to steady demand for excavator attachments across construction and industrial projects.

The excavator attachments market in India is expected to grow at the fastest rate during the forecast period. The country’s growth is propelled by increasing mechanization in the construction sector, which is accelerating the adoption of advanced and efficient excavator attachments to improve productivity and project efficiency. In addition, the expansion of the equipment rental market is enabling contractors to access cost-effective, multifunctional machinery, thereby supporting the wider adoption of excavator attachments across various construction applications.

Europe Excavator Attachments Market Trends

The excavator attachments market in Europe is expected to register a moderate CAGR from 2026 to 2033. The region’s growth is supported by ongoing infrastructure upgrades and a strong shift toward sustainable construction in both developed and developing economies. Governments and industry stakeholders are prioritizing environmentally responsible methods and accelerating the adoption of modern, energy-efficient equipment. Increased emphasis on circular economy principles, along with stricter emission regulations, is encouraging the use of advanced excavator attachments compatible with low-emission machinery.

The UK excavator attachments market is expected to grow at a significant rate during the forecast period. The market growth in the country is propelled by increasing demand for advanced solutions such as tiltrotators, quick couplers, and hydraulic attachments, particularly for compact machines used in urban construction, where flexibility and precision are critical. In addition, the adoption of smart technologies, including telematics and IoT-enabled systems, is enhancing equipment monitoring, improving operational efficiency, and enabling better control over construction processes, thereby supporting the overall market growth.

The excavator attachments market in Germany held a substantial market share in 2025. The country’s growing emphasis on industrial automation and precision engineering in construction is driving market growth. The growth is further supported by increasing investments in renewable energy infrastructure, including wind and solar projects, which require specialized excavator attachments for efficient foundation work and site preparation.

Key Companies & Market Share Insights

Some of the key companies in the excavator attachments include Caterpillar Inc., Komatsu Ltd., and Volvo Construction Equipment, among others. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Caterpillar Inc. is an American multinational manufacturer of construction and mining equipment. The company operates through multiple segments, including construction, resource, and energy & transportation, supported by a global manufacturing and dealer network spanning over 100 facilities worldwide. The company offers a broad range of excavator attachments, including buckets, hydraulic hammers, grapples, and quick couplers, designed to improve machine versatility and performance across various applications such as construction, mining, and infrastructure development.

-

Komatsu Ltd. is a global manufacturer known for its engineering expertise and technologically advanced construction equipment solutions. The company provides a comprehensive range of excavator attachments tailored for diverse end-use applications, including earthmoving, demolition, and material handling. Komatsu emphasizes the integration of smart technologies, such as IoT-enabled systems, machine control solutions, and predictive maintenance tools, to improve equipment performance and reduce operational costs.

Key Excavator Attachments Companies:

The following key companies have been profiled for this study on the excavator attachments market.

- Caterpillar Inc.

- Komatsu Ltd.

- Volvo Construction Equipment

- Hitachi Construction Machinery Co., Ltd.

- Doosan Infracore

- JCB Ltd.

- Epiroc AB

- Sandvik AB

- Liebherr Group

- Paladin Attachments

Recent Developments

-

In March 2026, Caterpillar Inc. announced a range of new Cat attachments (Heavy Duty Multipurpose (HD MP) buckets, Retrieval winch, Ripper/Scarifier, Bite-Limiter Mulchers, Grading beams, Tilting ditch cleaning buckets), aimed at increasing application flexibility for its next-generation skid steer loaders (SSL), compact track loaders (CTL), mini hydraulic excavators, and select backhoe loader models. The newly introduced attachments were designed to deliver reliable performance in demanding field conditions and to optimize the capabilities of next-generation machines across various applications, including land reclamation, grading, construction, demolition, agriculture, snow removal, and trenching.

-

In January 2026, Geith International Ltd. launched a new range of S-type hydraulic couplers, along with digging, grading, and tilting buckets for S40, S45, S50, and S60 pickup configurations. The newly introduced S-Type quick coupler utilizes the company’s triple-locking safety design compliant with ISO 13031, similar to its existing variable pin center pickup couplers. These couplers were manufactured using QT690 high-yield material, ensuring enhanced strength, flexibility, weldability, and durability for demanding construction applications.

Excavator Attachments Market Report Scope

Report Attribute

Details

Market size in 2025

USD 8.7 billion

Estimated market size in 2026

USD 9.2 billion

Projected market size by 2033

USD 14.8 billion

Growth rate

CAGR of 7.0% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, excavator size, attachment type, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; UAE; South Africa

Key companies profiled

Caterpillar Inc.; Komatsu Ltd.; Volvo Construction Equipment; Hitachi Construction Machinery Co., Ltd.; Doosan Infracore; JCB Ltd.; Epiroc AB; Sandvik AB; Liebherr Group; Paladin Attachments

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Excavator Attachments Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global excavator attachments market report based on material, excavator size, attachment type, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Steel

-

Polyurethane

-

Rubber

-

High-strength Composite Materials

-

Advanced Alloys

-

-

Excavator Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Mini Excavator (below 6t)

-

Small Excavator (6-15t)

-

Medium-sized Excavator (15-30t)

-

Large-sized Excavator (Above 30t)

-

-

Attachment Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Buckets

-

Hammers

-

Couplers

-

Grapples

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

France

-

Germany

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Excavator Attachments Industry Opportunity Assessment

Country/region-wise market sizing and forecasts Volume estimates Identification of high-growth regions and investment hotspots Analysis of demand, adoption trends, and regulatory landscape

Supported expansion and go-to-market strategy Enabled informed regional investment decisions Identified region-specific growth opportunities

Cross-Segmentation Analysis for the Excavator Attachments Industry

Demand and adoption assessment across key segments Criss-cross market analysis by material, by excavator size, by attachment type Segment attractiveness and growth potential benchmarking

Identified high-potential market segments Improved customer and segment prioritization Supported targeted product positioning and marketing strategy

Competitive Benchmarking and Strategic Positioning in the Excavator Attachments Industry

Benchmarking of key competitors across products, pricing, partnerships, and innovation Comparative assessment of market share, capabilities, and strategies Analysis of competitive strengths, gaps, and differentiation areas

Identified competitive white spaces and growth gaps Supported strategic positioning and differentiation Enabled data-driven competitive strategy development

Frequently Asked Questions About This Report

Rapid growth in the global construction sector is driving demand for excavator attachments, including buckets, hammers, grapples, couplers, and other tools. These attachments are essential for a wide range of construction activities, such as digging, material handling, demolition, and site preparation.

The global excavator attachments market size was valued at USD 8.7 billion in 2025 and is estimated at USD 9.2 billion for 2026.

The global excavator attachments market is expected to grow at a CAGR of 7.0% from 2026 to 2033, reaching USD 14.8 billion by 2033.

North America dominated with a 35.3% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Buckets segment dominated the market and accounted for the largest revenue share in 2025.

The medium-sized excavator (15-30t) segment held the largest revenue share in 2025, while the mini excavator (below 6t) segment is the fastest-growing.

The steel segment dominated the market in 2025 and accounted for the largest share of 37.8%. The segment’s growth is primarily driven by the availability of different grades of high-strength and alloy steel, which enable manufacturers to improve product performance while maintaining structural integrity under demanding operating conditions.

Key players include Caterpillar Inc.; Komatsu Ltd.; Volvo Construction Equipment; Hitachi Construction Machinery Co., Ltd.; Doosan Infracore; JCB Ltd.; Epiroc AB; Sandvik AB; Liebherr Group; Paladin Attachments.

About the Author(s)

HVAC & Construction Research Team

Technology · HVAC & ConstructionThis report was authored by the hvac & construction research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the hvac & construction segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.