- Home

- »

- Automotive & Transportation

- »

-

Logistics Market Size, Share & Growth Report, 2026 - 2033GVR Report cover

![Logistics Market (2026 - 2033)Report]()

Logistics Market (2026 - 2033)

Size, Share & Trends Analysis Report By Service, By Category (Conventional Logistics, E-Commerce Logistics), By Model, By Type, By Operation, By Mode Of Transport, By Application, By Region, And Segment Forecasts

Market Size, 2025

$4,109.1BMarket Estimate, 2026

$4,334.3BMarket Forecast, 2033

$8,496.1BCAGR, 2026–2033

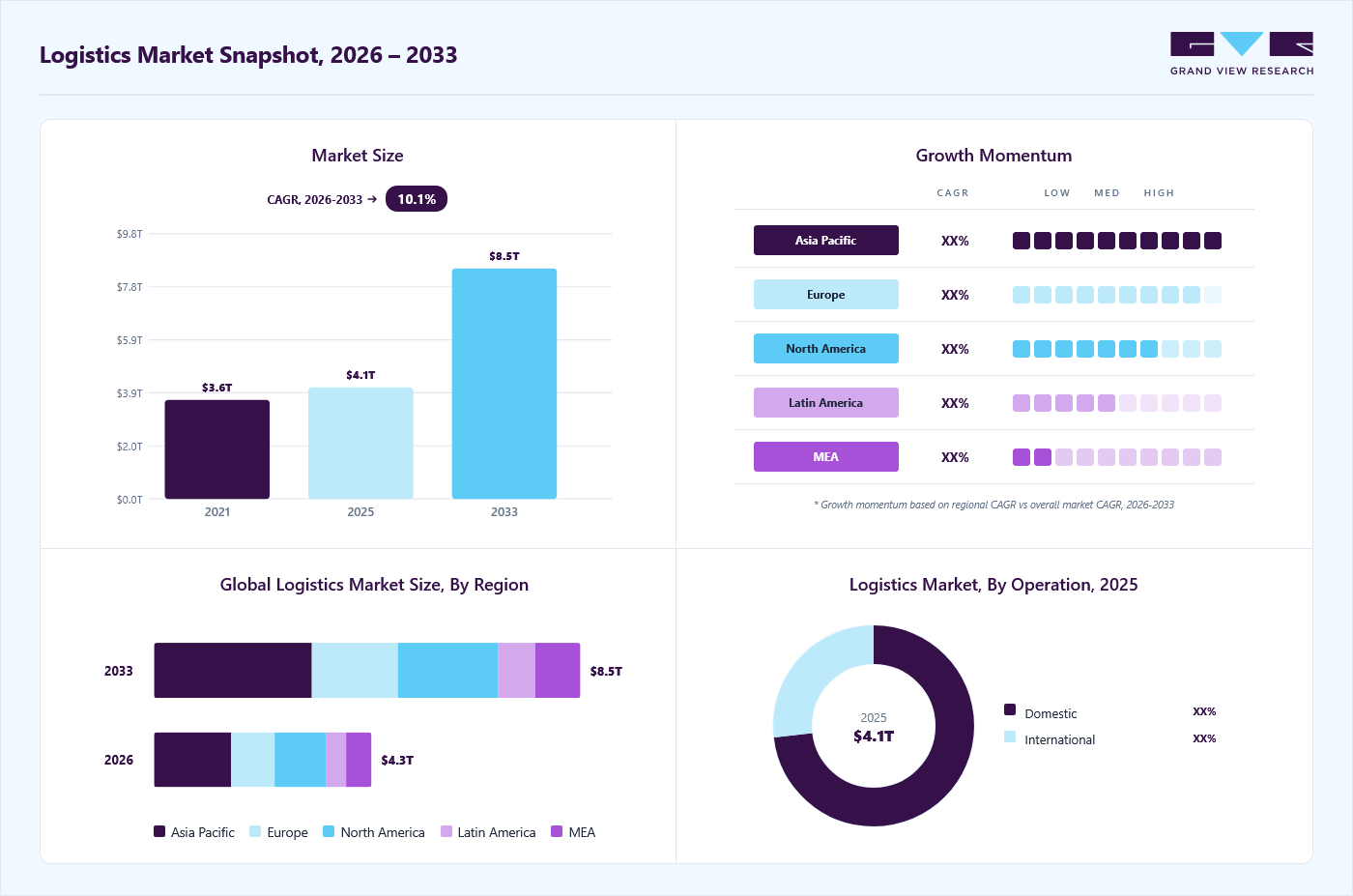

10.1%Logistics Market Summary

The global logistics market size was valued at USD 4,109.1 billion in 2025 and is projected to grow from USD 4,334.3 billion in 2026 to USD 8,496.1 billion by 2033, at a CAGR of 10.1% from 2026 to 2033. Asia Pacific held the largest global revenue share of 35.3% in 2025. The rapid expansion of e-commerce has significantly increased the volume and frequency of shipments, thus creating strong demand for efficient warehousing, last-mile delivery, and i006Etegrated supply chain solutions.

Key Market Trends & Insights

- By service: Transportation services held the largest revenue share of 31.9% in 2025.

- By category: Conventional logistics held the largest revenue share of 73.3% in 2025.

- By model: 3PL/contract logistics held the largest revenue share in 2025.

- By type: Forward logistics held the largest revenue share in 2025.

- By operation: Domestic segment held the largest revenue share in 2025.

- By mode of transport: Road segment held the largest revenue share in 2025.

- By application: Retail & e-commerce segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (35.3% revenue share, 2025)

- By country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 4,109.1 Billion

- Estimated market size in 2026: USD 4,334.3 Billion

- Projected market size by 2033: USD 8,496.1 Billion

- CAGR (2026-2033): 10.1%

In addition, technological advancements such as automation, artificial intelligence, real-time tracking, and advanced warehouse management systems are improving operational efficiency and reducing delivery times. The rapid growth of online retail has significantly influenced the target market, driving the need for efficient services, especially in last-mile delivery. This segment, crucial for transporting goods from distribution centers to consumers, has seen innovations such as drones and autonomous vehicles to meet the demand for faster, more reliable deliveries. Warehousing has also evolved to meet the needs of online retailers, with larger, automated warehouses becoming essential for managing inventory and fulfilling orders promptly.")

The growth of online retail has propelled the logistics industry towards more efficient and technologically advanced solutions. This transformation aims to meet the evolving demands of modern consumers for faster and more convenient delivery options. The logistics sector plays a critical role in the global economy by facilitating the movement of goods across various industries and geographical regions. Moreover, as online shopping continues to grow, the target market is expected to further innovate and adapt to meet the increasing demand for efficient, reliable services. This evolution is likely to lead to further advancements in technology and supply chain practices, driving the industry toward greater efficiency and sustainability.

Customer demand for faster deliveries is a significant driver of growth in the logistics industry. As consumers increasingly expect quick and reliable delivery of goods, logistics companies are compelled to innovate and optimize their operations to meet these expectations. This demand has led to the development of new delivery models, such as same-day and next-day delivery services, which require more efficient supply chain processes. To meet these demands, logistics companies are investing in technologies such as route optimization software, automated warehouses, and advanced tracking systems. Meeting customer expectations for faster deliveries not only drives the growth of the target market but also fosters customer loyalty and satisfaction. These factors are crucial for repeat business.

However, inadequate transportation infrastructure can limit supply chain efficiency by constraining the capacity of transportation networks and operations. This limitation can lead to delays in the movement of goods, increased transportation costs, and difficulties in accessing certain locations. Moreover, inadequate infrastructure can hinder the ability of logistics companies to meet customer demands for timely deliveries, impacting customer satisfaction. Addressing these infrastructure challenges is crucial to improving supply chain efficiency and ensuring the smooth flow of goods.

Market Dynamics

The logistics market is experiencing steady growth due to the adoption of AI-powered solutions that improve efficiency, enhance supply chain visibility, and enhance decision-making. Logistics 4.0 and smart supply chain transformation are creating additional opportunities by integrating automation, IoT, robotics, and data-driven systems. However, rising costs for fuel, labor, warehousing, and fleet maintenance continue to impact profitability. Despite these challenges, continued investment in digitalization, smart warehousing, and advanced technologies is expected to drive long-term market expansion.

Logistics companies are adopting AI-powered solutions to improve operational efficiency, optimize supply chain planning, and enhance decision-making through real-time data analysis. AI technologies enable businesses to forecast demand, identify operational bottlenecks, and streamline transportation activities, helping organizations reduce costs while improving service quality. The growing complexity of global supply chains and rising customer expectations for faster deliveries are further accelerating the adoption of AI-driven logistics solutions.

AI is also transforming warehouse management, fleet operations, and customer service functions within the logistics industry. Advanced AI algorithms optimize delivery routes, improve vehicle utilization, and support predictive maintenance, reducing transportation delays and operational downtime. In warehouses, AI-powered robotics and intelligent inventory management systems enhance order accuracy, inventory visibility, and fulfillment efficiency. In additional, AI-driven tracking systems, predictive analytics, and automated customer support tools improve supply chain transparency and customer experience. As businesses increasingly focus on automation, operational agility, and data-driven logistics management, AI adoption is expected to remain a key driver of market growth.

Increasing operational expenses represent a major restraint for the logistics market, significantly affecting profitability and cost management across the supply chain ecosystem. Logistics providers face continuous pressure from rising fuel prices, labor costs, warehouse leasing expenses, vehicle maintenance charges, and technology implementation costs. In addition, the growing need for investment in automation, warehouse digitalization, fleet modernization, and sustainability initiatives further adds to financial burdens.

Fuel price volatility remains a significant challenge for the logistics industry, as transportation modes such as trucking, air freight, maritime shipping, and rail operations are highly dependent on fuel consumption. Fluctuations in crude oil prices increase freight rates, delivery costs, and overall operational expenses, making cost management and long-term planning more difficult for logistics providers. Rising geopolitical tensions in key trade routes, such as the Strait of Hormuz, have further intensified shipping and transportation costs, while supply constraints and increasing fuel prices continue to strain logistics operations globally. Thus, higher freight expenses, surcharges, and rising ocean freight rates are increasing supply chain costs and creating additional pressure on manufacturers, retailers, and global trade networks.

Logistics 4.0 is reshaping logistics operations through the integration of advanced technologies, digitalization, and automation across the supply chain. Closely connected with Industry 4.0, or the Fourth Industrial Revolution, the concept is driving transformation not only in production environments but also across warehousing, transportation, inventory management, and distribution networks. Logistics 4.0 enables companies to manage logistics processes more intelligently, connectedly, and coordinately by leveraging modern technologies that enhance productivity, operational visibility, and decision-making. As digital transformation continues to redefine business operations, Logistics 4.0 marks a new phase in supply chain management, characterized by the widespread adoption of connected technologies, data-driven systems, and smart logistics solutions. Logistics 4.0 focuses on the comprehensive digitalization and seamless interconnection of logistics activities to improve efficiency, flexibility, and responsiveness across supply chains.

Market Concentration & Characteristics

The logistics market is fragmented, with a mix of large multinational logistics providers and numerous regional and local operators. Global companies such as DHL Group, Kuehne + Nagel, DSV A/S, FedEx, and United Parcel Service (UPS) hold significant market shares due to their extensive transportation networks, integrated service portfolios, advanced technology capabilities, and strong international presence. However, the market remains highly competitive, with numerous small- and medium-sized logistics providers operating across domestic transportation, warehousing, freight forwarding, and last-mile delivery. The presence of numerous regional players limits overall market concentration, particularly in developing economies where local expertise and distribution networks play a critical role.

The logistics industry is characterized by increased investment in digitalization, automation, and supply chain optimization. Logistics providers are adopting artificial intelligence, IoT tracking, warehouse automation, robotics, and cloud-based transportation management to improve efficiency and customer service. Strategic partnerships, mergers and acquisitions, and network expansion are becoming more common as companies seek to strengthen their positions and broaden their reach. The rising importance of e-commerce fulfillment, cold chain logistics, and value-added services is reshaping competition, prompting providers to offer integrated, technology-driven solutions that improve visibility and flexibility.

Analyst Perspective

Strong growth in the logistics market is driven by rapid e-commerce expansion, global trade, and increased investment in supply chain modernization. Advanced technologies, including artificial intelligence, IoT, robotics, and warehouse automation, are improving operational efficiency, visibility, and service quality. Rising demand for faster deliveries and integrated logistics solutions is prompting companies to enhance their transportation and warehousing capabilities. While challenges such as fuel price volatility and geopolitical disruptions remain, ongoing technological and infrastructure advancements continue to support market expansion. As businesses focus on supply chain resilience and agility, the logistics market is expected to sustain positive growth over the forecast period.

Mode of Transportation Insights

The road segment dominated the logistics market, accounting for the largest revenue share of 43.4% in 2025. The segment is primarily driven by increasing domestic freight transportation demand and expanding regional distribution networks across retail, manufacturing, e-commerce, healthcare, and industrial sectors. Rapid urbanization and growing consumer expectations for faster deliveries are significantly increasing reliance on road transportation for first-mile, middle-mile, and last-mile logistics operations. Additionally, the flexibility and door-to-door delivery capabilities offered by road transport make it the preferred mode for short- and medium-distance freight movement. Rising investments in highway infrastructure, industrial corridors, and smart transportation systems are further improving connectivity and reducing transit times across logistics networks.

The ocean segment is expected to grow at the fastest CAGR during the forecast period. The segment is primarily driven by increasing global trade activities and rising movement of bulk and containerized cargo across international markets. The expansion of import-export operations across industries such as manufacturing, automotive, consumer goods, chemicals, and food & beverages is significantly increasing demand for cost-efficient maritime transportation solutions. The growing containerization of freight and the increasing reliance on global sourcing and production networks are further supporting the expansion of ocean logistics services. Additionally, rising investments in port infrastructure, smart terminals, and shipping connectivity are improving cargo handling efficiency and strengthening international trade routes.

Category Insights

The conventional logistics segment dominated the logistics industry in 2025. The segment's growth is supported by rising industrial production, global trade expansion, and increased freight movement across the manufacturing, automotive, chemicals, food & beverages, and construction sectors. Traditional business-to-business (B2B) supply chains continue to rely heavily on conventional logistics networks for bulk transportation, warehousing, freight forwarding, and distribution operations. Growing international trade and the expansion of industrial supply chains are further increasing demand for standardized transportation and cargo-handling services. Additionally, infrastructure development projects such as ports, highways, rail corridors, and industrial zones are strengthening freight connectivity and improving logistics efficiency.

The e-commerce logistics segment is expected to witness the fastest growth over the forecast period. The segment is witnessing rapid growth driven by the continued expansion of online retail platforms and rising consumer preference for digital purchasing channels. Rising demand for fast, flexible, and last-mile delivery services is significantly driving investments in fulfillment centers, parcel transportation networks, and urban delivery infrastructure. Growth in cross-border e-commerce transactions is also increasing the need for integrated international logistics and reverse logistics solutions. Additionally, increasing smartphone penetration, digital payment adoption, and internet accessibility are expanding the global customer base for online retail.

Service Insights

The transportation services segment dominated the logistics market in 2025. Expansion of e-commerce, retail distribution networks, and manufacturing operations is significantly increasing freight transportation volumes across road, rail, air, and ocean modes. Businesses are increasingly focusing on reducing delivery timelines and improving supply chain responsiveness, thereby driving demand for integrated transportation solutions. Additionally, advancements in fleet management systems, route optimization technologies, and real-time shipment tracking are improving operational efficiency and freight visibility. Government investments in transportation infrastructure, such as highways, ports, rail corridors, and airports, are further strengthening logistics connectivity.

The warehousing and distribution Services segment is expected to witness the fastest growth over the forecast period. Expansion of omnichannel retailing and rising consumer expectations for faster delivery are encouraging businesses to establish strategically located warehousing facilities. Growing cross-border trade and supply chain globalization are also increasing the need for efficient cargo handling and distribution networks. Additionally, the adoption of warehouse automation technologies, such as robotics, automated storage and retrieval systems (ASRS), and warehouse management systems (WMS), is improving operational productivity and inventory accuracy. Increasing investments in cold storage infrastructure for pharmaceuticals and perishable goods are further supporting market growth.

Type Insights

The forward logistics segment dominated the logistics industry in 2025. The segment is primarily driven by increasing global trade activities, expanding manufacturing output, and rising demand for efficient product movement from production facilities to end customers. Growth in e-commerce, retail distribution, and omnichannel supply chains is significantly increasing the need for streamlined transportation, warehousing, and last-mile delivery operations. Businesses are increasingly focusing on improving delivery speed, order accuracy, and supply chain visibility to enhance customer satisfaction and operational efficiency. Additionally, advancements in transportation management systems, warehouse automation, route optimization, and real-time shipment tracking technologies are strengthening forward logistics capabilities.

The reverse logistics segment is expected to witness significant growth over the forecast period. The reverse logistics segment is witnessing substantial growth driven by rising product returns, increasing e-commerce transactions, and greater emphasis on sustainable supply chain practices. The expansion of online retail platforms and flexible return policies are significantly increasing the volume of returned goods, requiring efficient collection, inspection, refurbishment, recycling, or disposal processes. Businesses are increasingly investing in reverse logistics systems to improve customer experience, recover product value, and reduce operational losses associated with returns management. Additionally, growing environmental regulations and circular economy initiatives are encouraging companies to strengthen recycling, remanufacturing, and product recovery operations.

Model Insights

The 3PL/contract logistics segment dominated the logistics market in 2025. Rapid growth in e-commerce, retail, manufacturing, and healthcare industries is significantly increasing demand for scalable and flexible third-party logistics solutions. Companies are increasingly relying on 3PL providers to manage complex logistics operations, enhance delivery performance, and optimize inventory management across regional and global supply chains. Additionally, rising adoption of omnichannel distribution models and cross-border trade activities is accelerating the need for integrated transportation and warehousing services. Technological advancements such as warehouse automation, transportation management systems (TMS), real-time tracking, and data analytics are improving operational visibility and service efficiency within the 3PL market.

The 4PL/lead logistics segment is expected to witness the fastest growth over the forecast period. The 4PL/lead logistics segment is witnessing significant growth driven by the increasing complexity of global supply chains and the rising demand for end-to-end supply chain management solutions. Large enterprises are increasingly adopting 4PL services to gain centralized control over transportation networks, warehousing operations, freight forwarding, and multiple logistics service providers through a single integrated platform. Growing globalization, multi-country sourcing strategies, and expansion of cross-border trade are further increasing demand for strategic logistics coordination and supply chain optimization services. Additionally, the rising adoption of digital technologies, such as artificial intelligence, cloud-based logistics platforms, IoT-enabled tracking, and predictive analytics, is enabling 4PL providers to improve operational visibility and decision-making capabilities.

Operation Insights

The domestic segment dominated the logistics industry in 2025. Rising consumer demand for faster deliveries and efficient regional supply chain operations is significantly increasing freight transportation volumes within national boundaries. Governments are also investing heavily in transportation infrastructure such as highways, industrial corridors, rail networks, and logistics parks to improve domestic freight connectivity and reduce transit times. Additionally, growth in manufacturing, agriculture, FMCG, healthcare, and construction sectors is driving demand for reliable warehousing, transportation, and distribution services across urban and rural markets. Technological advancements, including fleet tracking, warehouse automation, route optimization, and digital freight platforms, are improving operational efficiency and shipment visibility within domestic logistics networks.

The international segment is expected to witness the fastest growth over the forecast period. The segment is driven by the globalization of trade, the expansion of cross-border e-commerce, and rising import-export activity across multiple industries. Businesses are increasingly establishing global sourcing, manufacturing, and distribution networks, thereby increasing demand for efficient international transportation and freight management solutions. Growth in free trade agreements, international trade corridors, and containerized cargo transportation is further supporting the expansion of global logistics operations. Additionally, the rising complexity of customs regulations, trade compliance requirements, and multimodal transportation coordination is encouraging companies to rely on specialized international logistics providers.

Application Insights

The retail & e-commerce segment accounted for the largest market share in 2025. Expansion of omnichannel retail models is significantly increasing demand for integrated warehousing, fulfillment, transportation, and last-mile delivery solutions. Retailers are increasingly investing in regional distribution centers, micro-fulfillment hubs, and automated warehousing systems to improve order processing efficiency and reduce delivery timelines. Additionally, rising cross-border e-commerce transactions are strengthening demand for international freight forwarding and customs management services. Technological advancements, such as AI-driven demand forecasting, real-time shipment tracking, and route optimization, are further improving operational efficiency in retail logistics networks.

The healthcare segment is expected to witness the substantial growth over the forecast period. The healthcare logistics segment is driven by increasing demand for safe, reliable, and temperature-controlled transportation of pharmaceuticals, medical devices, vaccines, and biotechnology products. Growth in global pharmaceutical production and rising healthcare expenditure are significantly increasing the movement of healthcare products across domestic and international supply chains. Strict regulatory requirements regarding product integrity, traceability, and cold chain compliance are encouraging investments in specialized healthcare logistics infrastructure. Additionally, the expansion of biologics, personalized medicines, and vaccine distribution networks is increasing demand for advanced cold storage and real-time monitoring solutions.

Regional Insights

The Asia Pacific logistics market accounted for the largest global revenue share of 35.3% in 2025. The expansion of cross-border logistics networks across the Asia Pacific is driving the market growth as trade flows, manufacturing activity, and e-commerce transactions continue to increase across the region. Rising economic integration among Southeast Asian countries is encouraging logistics providers to expand regional transportation networks and introduce end-to-end supply chain solutions to improve the efficiency of cargo movement. Companies are increasingly investing in integrated logistics ecosystems that combine transportation, warehousing, customs support, distribution, and last-mile delivery to address growing cross-border trade requirements.

China Logistics Market Trends

The China logistics market held a significant revenue share in 2025. The market is witnessing strong growth driven by the expansion of advanced warehousing infrastructure and supply chain modernization. Logistics providers are increasingly investing in automation technologies, smart warehouses, and integrated logistics facilities to improve efficiency and handle growing freight volumes. For instance, in March 2026, Shanghai Kintetsu Logistics opened a highly automated warehouse in the Shanghai Waigaoqiao Free Trade Zone, equipped with advanced storage and material-handling systems. Rising investments in warehouse automation and increasing demand from sectors such as electronics, semiconductors, healthcare, and automotive are expected to further accelerate market growth.

The logistics market in Japan is expected to grow at the notable CAGR during the forecast period. Labor shortages and demographic shifts are driving the market growth by increasing investment in automation and digital technologies across supply chains. Japan’s aging population and declining working-age workforce have created persistent labor constraints in trucking, warehousing, and last-mile delivery operations, forcing logistics companies to improve productivity through technology adoption. Growing reliance on robotics, automated warehouses, autonomous mobile robots, and AI-powered logistics systems is helping companies reduce dependence on manual labor while improving operational efficiency.

Europe Logistics Market Trends

The Europe logistics industry is expected to grow at the substantial CAGR during the forecast period. The increasing emphasis on sustainable logistics practices is supporting the market growth as governments, businesses, and consumers prioritize environmentally responsible supply chain operations. Stringent emission-reduction targets, carbon-neutrality commitments, and regulatory frameworks to reduce transportation-related emissions are encouraging logistics providers to modernize their operations. Companies are increasingly investing in low-emission transportation fleets, electric commercial vehicles, alternative fuels, and energy-efficient warehousing facilities to align with sustainability objectives while maintaining operational efficiency.

The Germany logistics market held a significant revenue share of Europe in 2025. Germany’s strong manufacturing base and export-oriented economy are driving the market growth, as the country remains one of Europe’s largest industrial and trading hubs. The presence of globally competitive industries such as automotive, machinery, chemicals, electronics, and industrial equipment generates substantial demand for transportation, warehousing, freight forwarding, and supply chain management services. Large-scale manufacturing operations require efficient inbound logistics for raw materials and components, as well as reliable outbound distribution networks for finished goods.

The logistics market in the UK is expected to grow at a notable CAGR during the forecast period. The UK remains one of the key global e-commerce markets, with online retail accounting for a substantial share of consumer spending. According to statistics from the U.S. International Trade Administration, UK e-commerce sales increased by nearly 30% during 2024-2025, highlighting strong growth in online purchasing activity and digital retail expansion. In addition, online channels are projected to account for approximately 38.1% of total retail sales in 2025, emphasizing the increasing importance of digital commerce within the retail ecosystem.

North America Logistics Market Trends

The North America logistics industry was identified as a lucrative region in 2025. The market growth is supported by a highly developed transportation infrastructure, advanced technological capabilities, and increasing demand for faster, more flexible supply chain operations. The region benefits from extensive connectivity across roadways, rail networks, air cargo facilities, and maritime ports, enabling efficient domestic and cross-border freight movement. Expanding e-commerce activity, omnichannel retail strategies, and continued industrial production growth are increasing demand for warehousing capacity, fulfillment centers, transportation services, and last-mile delivery solutions.

The U.S. logistics industry held a substantial revenue share in 2025, due to its extensive transportation network, advanced warehousing ecosystem, and strong consumer spending patterns. The rapid expansion of e-commerce has significantly increased demand for fulfillment centers, same-day delivery services, and third-party logistics (3PL) providers. According to the U.S. Census Bureau, retail e-commerce sales reached approximately USD 326.7 billion in Q1 2026, reinforcing the need for fulfillment centers, parcel delivery systems, and technologically advanced warehouse operations. Major logistics hubs, supported by ports, railways, airports, and interstate highway systems, continue to facilitate efficient domestic and international trade.

Key Logistics Company Insights

Some of the key players operating in the logistics market include Kuehne + Nagel International AG; Deutsche Post AG; Schenker AG (DB Schenker); and Expeditors International of Washington, Inc. These companies focus on logistics services, including freight transportation, warehousing, distribution, contract logistics, and digital supply chain solutions across multiple industries and regions.

-

Kuehne + Nagel International AG is a global provider of logistics and supply chain management. The company facilitates global trade by providing efficient logistics infrastructure and integrated supply chain solutions for diverse industries. Its logistics services include air and ocean freight, supported by strong carrier networks and capacity management. Kuehne + Nagel also offers contract logistics, warehousing, distribution, and supply chain management. Its portfolio features multimodal transportation, customs brokerage, consolidation, and tailored logistics solutions for sectors such as automotive, healthcare, high-tech, FMCG, perishables, and energy.

-

Schenker AG, doing business as DB Schenker, is a German logistics company serving local and global firms across various industries. It manages large, complex supply chains for multinational customers across the automotive, technology, and industrial sectors. It provides comprehensive services, including air, ocean, and land transport, supported by strong global connectivity and capacity management. This includes freight solutions such as customs brokerage, consolidation, and multimodal transport across road, rail, air, and sea, along with time-definite delivery services. It also delivers contract logistics, warehousing, distribution, and supply chain solutions, including advanced 4PL services for global enterprises.

Key Logistics Companies

The following key companies have been profiled for this study on the logistics market.

-

Kuehne + Nagel International AG

-

Deutsche Post AG

-

Schenker AG (DB Schenker)

-

Expeditors International of Washington, Inc.

-

CEVA Logistics

-

DSV A/S

-

FedEx

-

United Parcel Service, Inc.

-

NIPPON EXPRESS HOLDINGS C.H.

-

Robinson Worldwide, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: DHL Group; FedEx Corporation; CEVA Logistics; DSV A/S; Kuehne+Nagel International AG; DB Schenker.

- Mature logistics players focus on expanding global networks, strengthening multimodal transportation capabilities.

- Companies are investing in digital logistics platforms, automation, AI-driven analytics, and sustainable transportation initiatives to improve operational efficiency and environmental performance.

- Established brands gain their competitive edge from strong global transportation and warehousing networks, diversified service portfolios, long-term customer relationships, advanced supply chain infrastructure, and high operational reliability across international markets.

- Face high operational and infrastructure costs due to extensive global networks and large-scale logistics operations.

- Complex legacy systems and large organizational structures can reduce flexibility and slow adaptation to changing market demands and digital transformation.

Emerging Players: United Parcel Service, Inc.; C.H. Robinson Worldwide, Inc.; NIPPON EXPRESS HOLDINGS; Expeditors International of Washington, Inc.

- Focus on technology-driven and asset-light business models, leveraging digital freight platforms and AI-based route optimization.

- These companies emphasize e-commerce fulfillment, rapid expansion of last-mile delivery, strategic partnerships, and regional network growth to strengthen market presence and customer reach.

- Emerging players leverage technology-driven, asset-light business models, AI-enabled logistics optimization, and faster digital adoption to improve operational efficiency and scalability.

- These companies maintain a strong focus on e-commerce fulfillment and flexible logistics solutions to rapidly expand their customer reach and market presence.

- Often have limited global network presence and lower brand recognition than established logistics companies.

- Dependence on third-party logistics infrastructure and rapid expansion strategies can create challenges in maintaining profitability and service consistency.

Recent Developments

-

In March 2026, DHL Group announced that its Global Forwarding division had expanded air freight capacity between Asia and Europe to support rising cross-border trade demand and improve shipment reliability across major international trade routes.

-

In May 2026, C.H. Robinson expanded its cross-border logistics capabilities with the opening of a new 142,600-square-foot fresh produce logistics center in South Texas. The facility, operated through its Robinson Fresh division, was strategically located near the U.S.-Mexico border to improve the speed and efficiency of fresh produce movement. The expansion strengthened the company’s farm-to-fork supply chain network, enabling faster transit times and improved freshness for cross-border shipments.

Logistics Market Report Scope

Report Attribute

Details

Market size in 2025

USD 4,109.1 billion

Estimated market size in 2026

USD 4,334.3 billion

Projected market size by 2033

USD 8,496.1 billion

Growth rate

CAGR of 10.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Service, category, model, type, operation, mode of transport, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Kuehne + Nagel International AG; Deutsche Post AG; Schenker AG (DB Schenker); Expeditors International of Washington, Inc.; CEVA Logistics; DSV A/S; FedEx; United Parcel Service, Inc. (UPS); NIPPON EXPRESS HOLDINGS; C.H. Robinson Worldwide, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Logistics Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global logistics market report based on service, category, model, type, operation, mode of transport, application, and region:

-

Service Outlook (Revenue, USD Billion, 2021 - 2033)

-

Transportation Services

-

Warehousing & Distribution Services

-

Freight Forwarding Services

-

Inventory Management Services

-

Value-Added Logistics Services

-

Integration & Consulting Services

-

-

Category Outlook (Revenue, USD Billion, 2021 - 2033)

-

Conventional Logistics

-

E-Commerce Logistics

-

-

Model Outlook (Revenue, USD Billion, 2021 - 2033)

-

3PL/Contract Logistics

-

4PL/Lead Logistics

-

Others

-

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Forward Logistics

-

Reverse Logistics

-

-

Operation Outlook (Revenue, USD Billion, 2021 - 2033)

-

Domestic

-

International

-

-

Mode of Transport Outlook (Revenue, USD Billion, 2021 - 2033)

-

Road

-

Ocean

-

Air

-

Rail

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Retail & E-commerce

-

Food & Beverages

-

Industrial Machinery and Equipment

-

Consumer Electronics

-

Healthcare

-

Aerospace & Defense

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Mode of Transport

Revenue capture definition

Road

Road logistics refers to the transportation of goods through road networks using commercial vehicles such as trucks, vans, and trailers for domestic and cross-border freight movement. This mode is widely utilized for short- to medium-distance transportation due to its flexibility, extensive connectivity, and ability to provide door-to-door delivery services. Road transportation plays a critical role in distribution, retail logistics, industrial supply chains, and last-mile delivery operations.

Ocean

Ocean logistics refers to the transportation of goods through sea routes using cargo vessels and shipping containers for international trade and long-distance freight movement. This mode is primarily used for bulk cargo, containerized goods, industrial products, and raw materials due to its cost efficiency for large-volume shipments. Ocean freight forms a critical component of global supply chains and international commerce.

Air

Air logistics refers to the transportation of goods using commercial passenger aircraft or dedicated cargo aircraft for domestic and international shipments. This mode is primarily utilized for high-value, lightweight, perishable, or time-sensitive products requiring rapid delivery. Air freight offers the fastest transit times and high shipment reliability, making it essential for industries such as healthcare, electronics, retail, and e-commerce.

Rail

Rail logistics refers to the transportation of freight through railway networks using cargo trains for long-distance domestic and cross-border cargo movement. Rail freight is widely used for transporting bulk commodities, industrial materials, automotive products, chemicals, agricultural goods, and containerized cargo. This mode provides advantages such as cost efficiency, fuel efficiency, high carrying capacity, and lower environmental impact compared to road transportation for long-haul freight operations.

Segment - Category

Revenue capture definition

Conventional Logistics

Conventional logistics refers to traditional logistics operations focused on transportation, warehousing, inventory handling, and distribution of goods through established supply chain networks. This category primarily supports business-to-business (B2B) operations across industries such as manufacturing, automotive, industrial goods, chemicals, agriculture, and wholesale trade. Conventional logistics generally involves bulk freight movement, long-term supply contracts, scheduled transportation routes, and centralized warehousing operations.

E-Commerce Logistics

E-commerce logistics refers to logistics operations specifically designed to support online retail and digital commerce activities, including order fulfillment, inventory management, parcel transportation, last-mile delivery, and reverse logistics. This category focuses on handling high shipment volumes, smaller order sizes, rapid delivery requirements, and frequent return management associated with online shopping platforms.

Segment - Service

Revenue capture definition

Transportation Services

Transportation services refer to logistics activities involved in the physical movement of goods from one location to another through various modes such as road, rail, air, and ocean freight. These services support domestic and international cargo transportation for raw materials, components, and finished products across supply chains. Transportation services include freight movement, route planning, carrier management, shipment tracking, and last-mile delivery operations to ensure timely and efficient product distribution.

Warehousing and Distribution Services

Warehousing and distribution services refer to logistics operations associated with the storage, handling, sorting, packaging, and distribution of goods within supply chains. These services include inventory storage, order fulfillment, cross-docking, cargo handling, and regional distribution management for various industries. Warehousing and distribution facilities play a critical role in maintaining inventory availability, optimizing supply chain efficiency, and enabling timely product delivery across domestic and international markets.

Freight Forwarding Services

Freight forwarding services refer to specialized logistics solutions involving the coordination and management of cargo transportation across domestic and international trade routes. These services help businesses streamline cross-border trade and improve transportation efficiency.

Inventory Management Services

Inventory management services refer to logistics solutions focused on monitoring, controlling, and optimizing inventory levels throughout the supply chain. These services include stock tracking, demand forecasting, replenishment planning, inventory visibility, and warehouse inventory control to ensure efficient product availability and minimize operational costs. Inventory management services support improved order accuracy, reduced stock shortages, and enhanced supply chain responsiveness across multiple industries.

Value-Added Logistics Services

Value-added logistics services refer to supplementary logistics activities provided beyond standard transportation and warehousing operations to improve supply chain efficiency, product handling, and customer service capabilities. These services include packaging, labeling, kitting, assembly, product customization, quality inspection, palletization, reverse logistics, and after-sales support. Value-added logistics solutions help businesses streamline operations, reduce supply chain complexity, improve inventory management, and enhance order fulfillment efficiency.

Integration & Consulting Services

Integration and consulting services refer to strategic logistics solutions focused on optimizing supply chain operations, improving logistics efficiency, and integrating advanced technologies across transportation, warehousing, and distribution networks. These services include supply chain consulting, logistics network design, transportation optimization, warehouse planning, digital transformation, and implementation of logistics management systems such as transportation management systems (TMS), warehouse management systems (WMS), and enterprise resource planning (ERP) platforms.

Segment - Type

Revenue capture definition

Forward Logistics

Forward logistics refers to the movement of goods from manufacturers or suppliers to distributors, retailers, or end customers through the supply chain network. This process includes activities such as transportation, warehousing, inventory management, order fulfillment, and distribution to ensure timely product delivery. It plays a critical role in supporting manufacturing, retail, e-commerce, healthcare, and industrial supply chain operations.

Reverse Logistics

Reverse logistics refers to the movement of goods from end users back to manufacturers, distributors, or recycling facilities for returns processing, refurbishment, recycling, repair, or disposal. This process includes product returns management, asset recovery, remanufacturing, waste handling, and reverse transportation activities. Reverse logistics is widely utilized across e-commerce, electronics, automotive, healthcare, and consumer goods industries to manage returned or defective products efficiently.

Segment - Model

Revenue capture definition

3PL/Contract Logistics

Third-Party Logistics (3PL) or Contract Logistics refers to outsourced logistics services where external service providers manage specific supply chain operations on behalf of businesses. These services typically include transportation, warehousing, distribution, freight forwarding, inventory management, packaging, and order fulfillment activities. Companies utilize 3PL providers to improve operational efficiency, reduce logistics costs, enhance supply chain flexibility, and focus on core business functions.

4PL/Lead Logistics

Fourth-Party Logistics (4PL) or Lead Logistics refers to advanced logistics management services where a provider oversees and integrates the entire supply chain ecosystem on behalf of the client. A 4PL provider acts as a strategic logistics partner responsible for coordinating multiple logistics service providers, transportation networks, warehousing operations, technology integration, and supply chain optimization activities.

Others

The others segment includes first-party logistics (1PL) and second-party logistics (2PL). first-party logistics (1PL), where companies manage logistics internally using owned transportation and warehousing assets, and second-party logistics (2PL), where transportation providers offer standalone freight or warehousing services without integrated supply chain management.

Segment - Operation

Revenue capture definition

Domestic

Domestic logistics refers to the transportation, warehousing, distribution, and supply chain operations conducted within the geographical boundaries of a single country. This segment includes the movement of goods between manufacturers, suppliers, distribution centers, retailers, and end customers through road, rail, air, or inland waterways. Domestic logistics supports regional trade, retail distribution, industrial supply chains, e-commerce fulfillment, and last-mile delivery operations. The segment focuses on improving delivery speed, operational efficiency, inventory availability, and nationwide freight connectivity within local markets.

International

International logistics refers to the movement of goods across national borders through global transportation and supply chain networks. This segment includes import-export operations, cross-border freight transportation, customs clearance, international warehousing, freight forwarding, and multimodal logistics management through air, ocean, rail, and road transportation modes. International logistics supports global trade activities by enabling the movement of raw materials, components, and finished products between countries and regions.

Segment - End Use

Revenue capture definition

Retail & e-commerce

Retail and e-commerce logistics refer to logistics operations supporting the movement, storage, fulfillment, and delivery of consumer goods across online and offline retail channels. This segment includes warehousing, inventory management, order fulfillment, parcel transportation, last-mile delivery, and reverse logistics services for retailers, marketplaces, and e-commerce platforms.

Healthcare

Healthcare logistics refers to specialized logistics operations involved in the transportation, storage, handling, and distribution of pharmaceuticals, medical devices, vaccines, biotechnology products, and healthcare supplies. This segment includes cold chain logistics, temperature-controlled transportation, inventory monitoring, regulatory compliance management, and secure distribution services.

Food & Beverages

Food and beverages logistics refers to logistics activities associated with the transportation, storage, handling, and distribution of perishable and non-perishable food products and beverages. This segment includes cold chain transportation, refrigerated warehousing, inventory management, packaging, and retail distribution operations.

Media & Entertainment

Media and entertainment logistics refers to specialized logistics services supporting the transportation, storage, and distribution of broadcasting equipment, production materials, stage infrastructure, gaming hardware, audiovisual systems, and event-related assets. This segment includes time-sensitive transportation, event logistics coordination, equipment handling, international freight movement, and secure cargo management for film production, live events, concerts, sports broadcasting, and entertainment operations.

Industrial & Manufacturing

Industrial and manufacturing logistics refers to supply chain and logistics operations supporting the movement of raw materials, industrial components, machinery, and finished goods across manufacturing and industrial sectors. This segment includes inbound logistics, transportation, warehousing, inventory management, freight forwarding, and distribution services for industries such as automotive, electronics, chemicals, heavy machinery, and construction.

Oil & Gas

Oil and gas logistics refers to logistics services supporting exploration, production, refining, storage, and distribution activities within the oil and gas industry. This segment includes transportation of drilling equipment, pipelines, chemicals, petroleum products, and hazardous materials through road, rail, ocean, and air networks. The segment focuses on ensuring reliable and secure transportation across upstream, midstream, and downstream energy operations.

Others

The others segment include logistics operations supporting aerospace, agriculture, chemicals, telecommunications, mining, construction, defense, and government sectors. These industries often require specialized transportation, warehousing, project cargo handling, temperature-controlled logistics, or customized supply chain solutions based on operational requirements and regulatory standards.

Estimation Model

Layer Name

Key Question

Description

Global Freight Transportation Layer

What is the total value of freight movement across transportation modes?

Assess the overall transportation market across road, rail, air, maritime, and intermodal freight services. This establishes the total addressable market for logistics activities involving the movement of goods.

Logistics Services Penetration Layer

What proportion of freight spending is associated with outsourced logistics services?

Evaluate the adoption of third-party logistics (3PL), fourth-party logistics (4PL), freight forwarding, warehousing, and value-added logistics services across industries and regions.

Integrated Supply Chain Solutions Layer

What share of logistics spending is directed toward integrated and technology-enabled solutions?

Analyze the adoption of warehousing, inventory management, transportation management, cold chain logistics, last-mile delivery, and digital logistics platforms to determine the market value of advanced logistics services.

End-Use Industry Demand Layer

Which industries are driving logistics demand?

Assess logistics expenditure across key end-use sectors such as e-commerce, retail, manufacturing, automotive, healthcare, electronics, food & beverages, and consumer goods to derive the final market size and growth outlook.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional logistics infrastructure and supply chain analysis

Delivered country- and region-level assessment of logistics infrastructure, warehousing capacity, transportation networks, and trade flows

Assisted in identifying emerging markets and regional expansion opportunities

Evaluation of technology adoption trends in the logistics industry

Provided detailed analysis of AI, IoT, warehouse automation, robotics, digital freight platforms, and supply chain visibility solutions

Supported strategic planning by highlighting key technological transformation trends

Competitive Landscape Assessment

Provided profiling and competitive benchmarking of leading logistics providers along with strategic developments and expansion initiatives

Enabled evaluation of competitive positioning and market-entry strategies

Frequently Asked Questions About This Report

The road segment dominated the market and accounted for the largest revenue share of 43.4% in 2025. The segment is primarily driven by increasing domestic freight transportation demand and expanding regional distribution networks across retail, manufacturing, e-commerce, healthcare, and industrial sectors.

The forward logistics segment dominated the logistics market in 2025 with a share of 68.6%

The 3PL/contract logistics segment dominated the logistics market in 2025, with a 71.4% share.

The conventional logistics segment dominated the logistics market in 2025 with a share of 73.3%

The global logistics market size was estimated at USD 4,109.1 billion in 2025 and is expected to reach USD 4,334.3 billion in 2026.

The global logistics market is expected to grow at a compound annual growth rate of 10.1% from 2026 to 2033 to reach USD 8,496.1 billion by 2033.

The transportation services segment dominated the target market with a 31.9% revenue share in 2025, driven by its essential role in ensuring timely delivery of goods, the rise of e-commerce, increased international trade, technological advancements, and infrastructure investments.

Key players in the logistics market include Deutsche Post AG, United Parcel Service of America, Inc., FedEx, Maersk, CEVA Logistics (The CMA CGM Group), DB Schenker, Kuehne + Nagel, Nippon Express, Expeditors International, DSV, Kerry Logistics, XPO Logistics, Toll Group, J.B. Hunt Transport Services, C.H. Robinson Worldwide, Inc.

The logistics market is growing due to the rapid expansion of online retail, driving demand for efficient services in last-mile delivery and warehousing, as well as increasing customer expectations for faster deliveries. Additionally, improvements in transportation infrastructure and the complexity of international trade are further boosting the demand for supply chain services, requiring more efficient and agile supply chains.

About the Author(s)

Automotive & Transportation Research Team

Technology · Automotive & TransportationThis report was authored by the automotive & transportation research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the automotive & transportation segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.