- Home

- »

- Next Generation Technologies

- »

-

LiDAR Market Size, Share And Trends Report, 2026-2033GVR Report cover

![LiDAR Market (2026 - 2033)Report]()

LiDAR Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Airborne, Terrestrial, Mobile & UAV), By Application (Engineering, Environment, ADAS), By Component (GPS, Navigation, Laser Scanners), By Region, And Segment Forecasts

Market Size, 2025

$3.0BMarket Estimate, 2026

$3.4BMarket Forecast, 2033

$9.0BCAGR, 2026–2033

14.8%LiDAR Market Summary

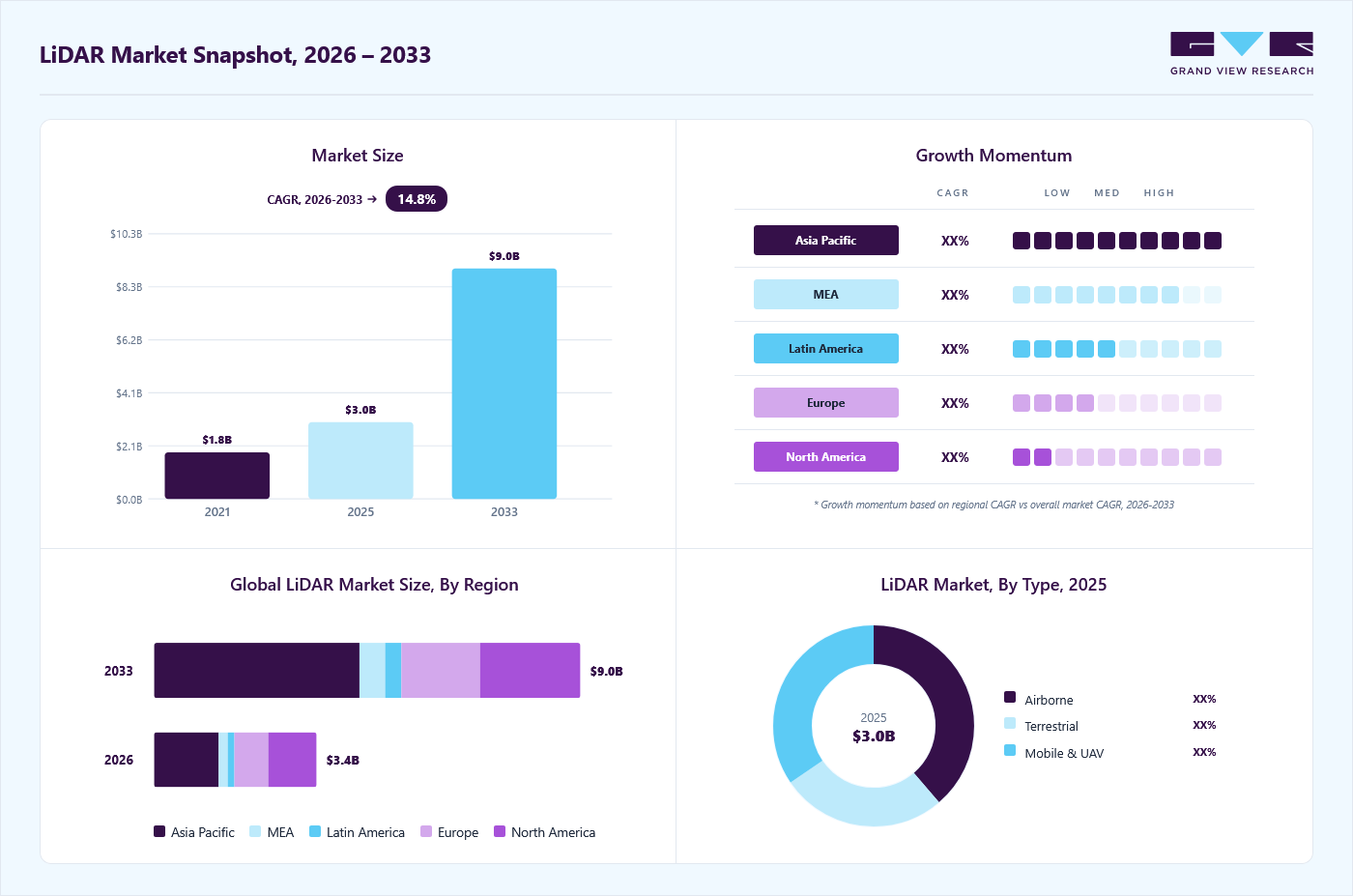

The global LiDAR market size was valued at USD 3.0 billion in 2025 and is projected to grow from USD 3.4 billion in 2026 to USD 9.0 billion by 2033, growing at a CAGR of 14.8% from 2026 to 2033. Asia Pacific dominated the market with the largest revenue share of 38.8% in 2025. The market is growing rapidly due to advancements in autonomous vehicle technology. Companies increasingly adopt LiDAR sensors for self-driving cars, providing highly accurate 3D mapping and real-time object detection.

Key Market Trends & Insights

- By type: airborne accounted for the dominant share of 38.7% in 2025.

- By application: the corridor mapping segment accounted for the dominant share of 37.1% in 2025.

- By component: laser scanners dominate the market with share of 46.9% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (38.8% revenue share, 2025)

- By country: The LiDAR market in the China held the largest share in the Asia Pacific region in 2025.

Market Size & Forecast

- Market Size in 2025: USD 3.0 Billion

- Estimated Market Size in 2026: USD 3.4 Billion

- Projected Market size by 2033: USD 9.0 Billion

- CAGR (2026-2033): 14.8%

This demand is fueled by the automotive industry's push toward safer, more reliable autonomous systems. Moreover, government regulations promoting advanced driver assistance systems (ADAS) have further boosted the adoption of LiDAR technology. Developing higher-resolution sensors and decreasing costs have made LiDAR more accessible for automotive applications. The growing integration of LiDAR into electric vehicles also contributes to market growth.")

The market is expanding within the geospatial and mapping industries. LiDAR technology offers exceptional precision for topographical mapping, urban planning, and land surveying, helping professionals gather accurate data. Its applications in environmental monitoring, such as deforestation tracking and flood risk assessment, have also surged due to the increasing focus on climate change. Furthermore, LiDAR systems are becoming more essential in disaster management by enabling rapid terrain analysis and damage assessment. Government infrastructure projects, especially in developing regions, are turning to LiDAR for planning and development. The technology's ability to capture vast areas quickly and efficiently makes it a preferred construction and civil engineering tool.

The market also benefits from advances in drones and UAVs (unmanned aerial vehicles). LiDAR-equipped drones offer an efficient solution for industries like agriculture, mining, and forestry, providing detailed aerial surveys. These applications drive adoption due to the ease of use and reduced operational costs of drone-based LiDAR systems. Furthermore, technological innovations are enhancing the performance and portability of LiDAR sensors for UAV platforms. As industries prioritize real-time data collection and precision, drone-based LiDAR is becoming more widespread. The defense and security sectors also utilize LiDAR for surveillance and reconnaissance missions. Overall, the growing adoption of LiDAR in aerial applications further accelerates market growth.

Market Dynamics

The LiDAR market is supported by increasing demand for advanced sensing and measurement technologies across a wide range of industries. Ongoing technological advancements are improving performance, reliability, and affordability, encouraging broader adoption. Organizations are investing in digital transformation initiatives that require accurate data collection and real-time environmental awareness. Companies are focusing on product development, partnerships, and expansion strategies to strengthen their market presence. At the same time, cost considerations, competitive pressures, and evolving industry standards continue to influence market growth and adoption patterns.

The growing need for accurate and real-time data collection and analysis is a major factor supporting the growth of the LiDAR market. Organizations increasingly depend on precise spatial, environmental, and object-level information to improve planning, monitoring, and decision-making processes. Traditional data collection methods often face limitations in speed, accuracy, and coverage, creating demand for more advanced sensing solutions. LiDAR technology addresses these requirements by delivering highly detailed and reliable data across a variety of operating environments.

At the same time, the increasing emphasis on data-driven strategies is encouraging wider use of LiDAR systems across multiple industries. The technology enables users to capture large volumes of information quickly, supporting faster analysis and more informed resource management. Improved access to high-quality data helps organizations optimize workflows, reduce operational uncertainties, and enhance overall productivity. Continuous advancements in data analytics and digital technologies are further increasing the value of precise spatial information. These factors are contributing to sustained demand for LiDAR solutions and supporting long-term market expansion.

The relatively high initial cost of LiDAR systems continues to limit wider adoption across certain end users and applications. Expenses related to hardware procurement, software platforms, deployment, integration, and maintenance can create financial challenges, particularly for organizations operating under budget constraints. Although technological advancements are improving affordability, the total cost associated with implementing and operating LiDAR solutions remains substantial in many cases. These cost considerations can slow purchasing decisions and reduce the pace of large-scale deployments.

Organizations may also need to invest in workforce training, data processing infrastructure, and system upgrades to fully utilize LiDAR-generated information. Such additional requirements can increase implementation complexity and extend return-on-investment timelines. In some cases, potential users may choose alternative technologies with lower upfront costs despite differences in performance and accuracy. Consequently, financial and implementation-related challenges continue to moderate the rate of LiDAR market adoption.

The increasing development of smart infrastructure, automation, and data-driven operations is creating substantial opportunities for the LiDAR market. Organizations are adopting advanced technologies to improve operational visibility, data accuracy, and decision-making capabilities. LiDAR solutions support these objectives by providing detailed spatial and environmental information that can be integrated into digital workflows. As modernization efforts continue across various sectors, demand for precise and reliable sensing technologies is expected to increase.

The expanding use of digital platforms and advanced analytics is further enhancing the value of LiDAR-generated data. The technology supports a wide range of activities, including monitoring, asset management, planning, and operational optimization across diverse environments. Improvements in data processing and visualization capabilities are enabling organizations to derive greater insights from collected information. These developments are broadening the application scope of LiDAR and creating favorable conditions for long-term market growth.

Market Concentration & Characteristics

The LiDAR market is moderately concentrated, with competition occurring among a mix of established participants and emerging technology providers. The market serves a broad range of applications, including mapping, industrial automation, robotics, transportation, and defense, which supports the presence of numerous vendors across the ecosystem. However, certain application areas exhibit higher concentration due to the technical expertise, manufacturing capabilities, and scale required to compete effectively. Ongoing innovation and the entry of new participants continue to maintain a competitive environment.

The market is characterized by rapid technological advancements focused on improving performance, accuracy, reliability, and affordability. Merger and acquisition activity remains active as companies seek to expand capabilities and strengthen their competitive positions. Regulatory requirements significantly influence product development and deployment, particularly in applications with strict safety and operational standards. Alternative sensing technologies provide partial substitutes, although LiDAR offers distinct advantages in data precision and environmental perception. Demand is generated from multiple industries, limiting dependence on any single end-user group while allowing certain applications to contribute a larger share of market revenue.

Analyst Perspective

The LiDAR market is positioned for strong growth as adoption expands across automotive, geospatial mapping, infrastructure, mining, and industrial automation applications. Advances in sensor performance, detection range, and data processing capabilities are improving the value proposition of LiDAR solutions across industries. The automotive sector remains a major demand driver, supported by increasing integration of LiDAR into advanced driver-assistance systems and autonomous driving platforms. Government investments in infrastructure development, digital mapping, and environmental monitoring continue to support market expansion. Mobile and UAV-based LiDAR solutions are gaining wider acceptance due to their efficiency in collecting high-accuracy spatial data. Competitive activity is increasing as established geospatial companies, and emerging sensor manufacturers invest in innovation and strategic partnerships.

Type Insights

Based on type, the airborne segment led the market with the largest revenue share of 38.7% in 2025. This segment dominates the market due to its extensive use in large-scale mapping and surveying applications. Airborne LiDAR systems are preferred for their ability to cover vast areas quickly and accurately, making them ideal for topographic and infrastructure mapping. The technology's high precision in capturing elevation data is widely used in environmental monitoring and natural resource management. Government projects, such as infrastructure development and disaster response, rely heavily on airborne LiDAR for detailed geographical data. This dominance is also supported by continuous advancements in aircraft-based LiDAR systems, improving range and data resolution.

The mobile and UAV segment is experiencing rapid growth due to its versatility and cost-effectiveness. UAVs equipped with LiDAR provide a flexible solution for agriculture, mining, and forestry industries, offering detailed aerial surveys with minimal human intervention. Mobile LiDAR systems mounted on vehicles are increasingly used for urban planning, road mapping, and infrastructure inspection. The portability and ease of deployment of UAV and mobile LiDAR systems allow for real-time data collection in difficult-to-access or hazardous environments. Technological innovations enhancing sensor performance and data processing capabilities further drive the adoption of mobile and UAV-based LiDAR.

Application Insights

Based on application, the corridor mapping segment led the market with the largest revenue share of 37.1% in 2025. due to its critical role in infrastructure projects such as highways, railways, and power lines. It provides highly accurate and detailed 3D maps, essential for planning and maintaining linear infrastructures. The precision and efficiency of LiDAR in capturing long stretches of land with minimal human intervention make it the preferred method for corridor mapping. Governments and private companies increasingly use LiDAR for monitoring and inspection purposes in utility corridors. This demand is further supported by growing infrastructure development projects worldwide, requiring precise and up-to-date geographical data.

The ADAS (Advanced Driver Assistance Systems) segment is growing rapidly as the automotive industry shifts toward automation and enhanced safety features. LiDAR sensors are essential for real-time 3D mapping and object detection and critical for advanced vehicle navigation and collision avoidance. With regulatory support for ADAS technologies, the adoption of LiDAR in automotive applications is rising, particularly for features like lane-keeping assistance and emergency braking. Improvements in LiDAR sensor resolution and cost reductions make the technology more accessible for a wider range of vehicles.

Component Insights

Based on component, the laser scanners segment led the market with the largest revenue share of 46.9% in 2025, due to their ability to capture high-resolution 3D data with precision and speed. They are widely used in applications such as topographic mapping, construction, and forestry, where detailed surface measurements are critical. The growing need for accurate spatial data across various scanner accuracy and range improvement industries has cemented the role of laser scanners as the preferred LiDAR technology. Continuous scanner accuracy and range improvements have enhanced their effectiveness in large-scale surveying projects. Moreover, the affordability and adaptability of laser scanners for different environments contribute to their dominant position in the market.

The navigation segment, particularly using Inertial Measurement Units (IMU), is growing significantly. IMUs enhance LiDAR’s accuracy by providing real-time positioning and orientation data, especially in mobile and aerial platforms. Integrating IMUs with LiDAR is gaining traction in autonomous vehicles, UAVs, and other navigation-intensive applications. As industries increasingly prioritize precise geolocation and stable data collection in dynamic environments, IMU-based navigation systems are becoming essential. With advancements in IMU technology, LiDAR systems can offer more reliable navigation solutions, driving further growth in this segment.

Regional Insights

North America LiDAR market is experiencing a robust market, driven by increasing adoption in sectors such as autonomous vehicles, smart cities, and defense. The push for advanced infrastructure projects across the region also accelerates demand for LiDAR technology, particularly in transportation and urban planning. Companies in North America are focusing on developing high-resolution LiDAR systems to enhance real-time mapping and data accuracy. The region’s established tech industry is fueling innovation in LiDAR applications, making it a hub for research and development. Moreover, government funding and partnerships with private firms are bolstering market expansion.

U.S. LiDAR Market Trends

The LiDAR market in the U.S. is growing primarily due to advancements in autonomous driving and aerial mapping technologies. The automotive sector is a key driver, with LiDAR integral to developing ADAS and self-driving vehicles. The country’s defense industry also heavily invests in LiDAR for surveillance, targeting, and reconnaissance operations. The U.S. also sees increased LiDAR use in agriculture and environmental monitoring, supporting precision farming and disaster management initiatives. Regulatory frameworks encouraging the use of LiDAR in improving road safety and infrastructure further support growth.

Europe LiDAR Market Trends

The LiDAR market in Europe is witnessing significant growth, largely propelled by smart mobility initiatives and the widespread adoption of ADAS technologies. LiDAR is crucial in Europe’s efforts to reduce carbon emissions and improve road safety, particularly by developing autonomous and electric vehicles. The region's strong environmental focus is also driving the use of LiDAR in sustainable land use and climate monitoring. Moreover, Europe’s investment in smart city projects and modern transportation systems creates new opportunities for LiDAR deployment.

Asia Pacific LiDAR Market Trends

Asia Pacific dominated the LiDAR market with the largest revenue share of 38.8% in 2025, fueled by strong demand from the automotive industry and large-scale infrastructure development. Countries such as China and Japan are leading the way in integrating LiDAR into autonomous vehicles and public transportation systems. The region also sees increased LiDAR use in industrial automation, agriculture, and environmental monitoring. Governments in the Asia Pacific are heavily investing in smart city projects and upgrading infrastructure, boosting the demand for LiDAR technology.

The LiDAR market in the China held the largest share in the Asia Pacific region in 2025. The China LiDAR market is expanding due to increased adoption of LiDAR sensors, autonomous vehicles, ADAS, and intelligent transportation systems in the automotive sector. Investments in smart cities, robotics, industrial automation, UAVs, and autonomous mobility are driving demand for advanced 3D sensing, object detection, and real-time mapping. Advancements in solid-state LiDAR, laser scanning, AI-powered perception, digital mapping, and HD mapping are improving performance and lowering deployment costs. In addition, strong government support for connected mobility and smart infrastructure is creating significant growth opportunities.

Key LiDAR Company Insights

Some of the key companies in the market include Faro Technologies, Inc., Leica Geosystem Holdings AG, Teledyne Optech Incorporated, and others. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions and partnerships with other major companies.

-

Faro Technologies, Inc. focuses on high-precision 3D laser scanning systems for industrial applications. The company has developed portable and versatile LiDAR solutions used in manufacturing, construction, and forensic analysis, enhancing data capture accuracy. Their continuous innovation in sensor technology and software integration is expanding the use of LiDAR in complex environments, driving broader adoption across various sectors.

-

Quantum Spatial, Inc. utilizes LiDAR for high-resolution aerial mapping, focusing on applications such as environmental monitoring, infrastructure development, and natural resource management. Their expertise in processing large datasets and delivering precise geospatial insights has made Quantum Spatial a key player in supporting public and private sector projects across various industries.

Key LiDAR Companies:

The following key companies have been profiled for this study on the LiDAR market.

-

Faro Technologies, Inc.

-

GeoDigital

-

Hesai Group

-

Innoviz Technologies Ltd.

-

Leica Geosystem Holdings AG

-

Quantum Spatial, Inc.

-

RIEGL USA, Inc.

-

Sick AG

-

Teledyne Optech Incorporated

-

Trimble Navigation Limited

-

Velodyne LiDAR, Inc.

-

YellowScan

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Established Players (FARO Technologies, Inc., Leica Geosystems Holdings AG, RIEGL USA, Inc., SICK AG, Teledyne Optech Incorporated.)

- Established players focus on portfolio expansion, strategic acquisitions, long-term customer relationships, stronger distribution networks, and integration with broader geospatial solutions.

- Established players benefit from strong brand recognition, extensive customer relationships, broad product portfolios, well-established distribution channels, and deep industry expertise.

- Established players often face challenges related to higher operating costs, slower product development cycles, and legacy product portfolios.

Emerging Players (GeoDigital, Hesai Group, Innoviz Technologies Ltd., Quantum Spatial, Inc., YellowScan.)

- Emerging players focus on product innovation, cost optimization, OEM partnerships, expansion into high-growth applications, and entry into new geographic markets.

- Emerging players benefit from advanced sensor innovation, faster product development cycles, competitive pricing, specific offerings, and strong partnerships in high-growth markets.

- Emerging players often face challenges related to limited brand recognition, smaller customer bases, constrained resources, and lower global market reach.

Recent Developments

-

In September 2024, Teledyne Geospatial announced the launch of its new products and solutions, including the Galaxy Edge airborne LiDAR system and the Network Surveyor, at the INTERGEO 2024 event. This launch aims to provide advanced real-time data processing capabilities for enhanced mapping and analysis.

-

In August 2024, YellowScan collaborated with Nokia, a Telecommunications company in Finland, to integrate the YellowScan Surveyor Ultra LiDAR scanner into Nokia's Drone Networks. This collaboration aims to transform industrial operations through automated 5G-based LiDAR scanning for applications such as telecommunications towers and utility inspections.

-

In June 2024, Innoviz Technologies Ltd. announced a collaboration with an automotive OEM to improve its Level 4 autonomous vehicle functionalities by integrating Innoviz's new short-range LiDAR sensors into the OEM's platform. The short-range LiDAR, part of the InnovizTwo product platform, is designed for light commercial vehicles and aims to support the growing demand for safe and efficient autonomous driving solutions.

-

In April 2024, Hesai Group collaborated with Marelli Holdings Co., Ltd., a Japan-based multinational automotive parts manufacturer, to integrate its innovative headlamp design with Hesai's next-generation ATX lidar technology, enhancing vehicle safety and object detection while maintaining aesthetics and aerodynamics. This collaboration showcases a significant reduction in lidar volume and seamless integration into headlamps, emphasizing affordability and improved performance for cost-effective and luxury vehicle models.

LiDAR Market Report Scope

Report Attribute

Details

Market size in 2025

USD 3.0 billion

Estimated market size in 2026

USD 3.4 billion

Projected market size by 2033

USD 9.0 billion

Growth rate

CAGR of 14.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, application, component, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; Australia; South Korea; Brazil; KSA; UAE; South Africa

Key companies profiled

Faro Technologies, Inc.; GeoDigital; Hesai Group; Innoviz Technologies Ltd.; Leica Geosystem Holdings AG; Quantum Spatial, Inc.; RIEGL USA, Inc.; Sick AG; Teledyne Optech Incorporated; Trimble Navigation Limited; Velodyne LiDAR, Inc.; YellowScan.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global LiDAR Market Report Segmentation

This report offers revenue growth forecasts at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global LiDAR market report based on type, application, component, and region:

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Airborne

-

Terrestrial

-

Mobile & UAV

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Corridor Mapping

-

Engineering

-

Environment

-

Exploration

-

ADAS

-

Others

-

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

GPS

-

Navigation (IMU)

-

Laser Scanners

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

KSA

-

UAE

-

South Africa

-

-

Research Methodology

(a) Segment Definition

Segment – Product Type

Revenue capture definition

Airborne

Demand for airborne LiDAR solutions stems from their use in manned aircraft and helicopters for large-area mapping, topographic surveys, forestry assessment, corridor mapping, environmental monitoring, and disaster management applications. Government agencies, survey organizations, and infrastructure developers use these solutions to collect high-resolution geospatial data across extensive geographic regions.

Terrestrial

Market revenue is captured from ground-based LiDAR systems used for surveying, construction, mining, engineering, heritage preservation, and industrial site documentation. Organizations utilize these solutions to generate precise 3D models, perform structural analysis, monitor assets, and support project planning and execution.

Mobile & UAV

Income is generated from LiDAR systems integrated into mobile mapping vehicles and unmanned aerial vehicles (UAVs) for rapid data acquisition and high-precision mapping. End users deploy these solutions for transportation infrastructure mapping, utility inspections, urban planning, agriculture, mining, and asset management where flexibility and operational efficiency are critical.

Segment – Application

Revenue capture definition

Corridor Mapping

Revenue is generated from the use of LiDAR solutions for mapping transportation, utility, and pipeline corridors. Organizations utilize these systems to support route planning, asset inventory, maintenance, and infrastructure development projects.

Engineering

Revenue is captured from LiDAR applications used in engineering design, construction planning, structural assessment, and digital twin creation. Engineering firms and project developers employ these solutions to obtain precise spatial data for project execution and asset management.

Environment

Demand for LiDAR solutions is driven by environmental monitoring, forestry management, coastal assessment, flood modeling, and ecosystem analysis. Government agencies, research institutions, and environmental organizations use these systems to collect detailed terrain and vegetation data.

Exploration

Revenue is generated from LiDAR deployments in mining, oil and gas, and geological exploration activities. Organizations use these solutions to improve site assessment, resource evaluation, terrain analysis, and operational planning.

ADAS

Spending in this category is driven by the integration of LiDAR sensors into advanced driver-assistance systems (ADAS) for object detection, collision avoidance, lane assistance, and navigation functions. Automotive manufacturers and technology providers deploy these solutions to enhance vehicle safety and driving performance.

Others

Revenue is captured from LiDAR applications across security, defense, archaeology, smart cities, robotics, and other specialized use cases. End users utilize these solutions to support spatial analysis, monitoring, automation, and operational decision-making.

Segment – Component

Revenue capture definition

GPS

Revenue is generated from the integration of Global Positioning System (GPS) technologies with LiDAR platforms to provide accurate geospatial positioning and location data. These solutions support mapping, surveying, navigation, and asset management applications across multiple industries.

Navigation (IMU)

Demand for inertial measurement units (IMUs) is driven by their ability to provide orientation, motion, and positioning information for LiDAR systems. End users deploy these solutions to improve data accuracy and maintain reliable navigation in environments where satellite signals may be limited.

Laser Scanners

Revenue is captured from laser scanning components that collect distance and spatial information by emitting and receiving laser pulses. These systems form the core of LiDAR platforms used in surveying, mapping, automotive, industrial, and environmental applications.

Others

Revenue is generated from supporting components and technologies, including data processing units, software platforms, communication modules, and power management systems. These solutions enhance LiDAR performance, data quality, and operational efficiency across diverse applications.

(b) Estimation Model

Layer No.

Layer Name

Key Question

Description

01

Demand Generation Layer

Which industries are driving demand for LiDAR solutions?

Industries such as automotive, geospatial mapping, infrastructure, mining, and defense create the need for LiDAR solutions through increasing requirements for high-precision spatial data.

02

Technology Availability Layer

What LiDAR technologies are available and ready for use?

Availability of LiDAR sensors, platforms, and supporting technologies determines how widely solutions can be deployed across use cases and operating environments globally.

03

Deployment & Adoption Layer

How widely is LiDAR being adopted across applications?

LiDAR adoption varies across applications such as ADAS, autonomous driving, surveying, corridor mapping, and industrial automation depending on maturity, cost, and integration readiness.

04

Market Value Layer

What is the total revenue potential of the LiDAR market?

Market value is derived from revenues generated through hardware, software, and services across industries and regions, supported by LiDAR adoption in automotive, mapping, and industrial applications.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Market Entry & Expansion Assessment

Assessed regional demand potential, application opportunities, competitive dynamics, and regulatory requirements across key LiDAR markets.

Identified high-growth opportunities, supported market entry and expansion strategies, and highlighted key investment risks.

Product Positioning & Competitive Intelligence

Evaluated product performance, pricing strategies, competitor portfolios, and customer purchasing preferences across major application areas.

Improved product differentiation, supported pricing optimization, identified market gaps, and strengthened competitive positioning.

Technology & Innovation Assessment

Analyzed emerging technology trends, sensor innovations, adoption readiness, and strategic partnership opportunities within the LiDAR ecosystem.

Identified future growth areas, supported innovation roadmap development, evaluated commercialization potential, and strengthened strategic decision-making.

Frequently Asked Questions About This Report

The global LiDAR market size was estimated at USD 3.0 billion in 2025 and is expected to reach USD 3.4 billion in 2026.

The global LiDAR market is expected to grow at a compound annual growth rate of 14.8% from 2026 to 2033 to reach USD 9.0 billion by 2033.

Some key players operating in the LiDAR market include Faro Technologies, Inc., Leica Geosystem Holdings AG, Teledyne Optech Incorporated, Trimble Navigation Limited, RIEGL USA, Inc., Quantum Spatial, Inc., Velodyne LiDAR, Inc., Sick AG, YellowScan, and GeoDigital

Key factors driving the growth of the LiDAR market include the increasing demand for high-precision mapping and surveying, advancements in autonomous vehicles requiring accurate distance measurements, growing applications in environmental monitoring and conservation, and rising investments in smart city initiatives.

The Airborne segment led with a 38.7% revenue share in 2025 and is also the fastest-growing segment.

The Corridor Mapping segment held the largest revenue share of 37.1% in 2025, while ADAS is the fastest-growing segment.

The Laser Scanners segment led with a 46.9% revenue share in 2025 and is also the fastest-growing segment.

Asia Pacific is the fastest-growing region over the forecast period.

Asia Pacific dominated the LiDAR market with a share of 38.8% in 2025. This is attributable to the rapid adoption of advanced technologies in various sectors, including automotive, aerospace, and construction, and significant investments in infrastructure development.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.