- Home

- »

- Advanced Interior Materials

- »

-

Heat Treating Market Size And Share Report, 2026-2033GVR Report cover

![Heat Treating Market (2026 - 2033)Report]()

Heat Treating Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Steel, Cast Iron), By Process (Case Hardening, Hardening & Tempering), By Equipment (Electrically Heated Furnace), By Application (Automotive, Aerospace), By Region, And Segment Forecasts

Market Size, 2025

$96.1BMarket Estimate, 2026

$99.3BMarket Forecast, 2033

$128.1BCAGR, 2026–2033

3.7%Heat Treating Market Summary

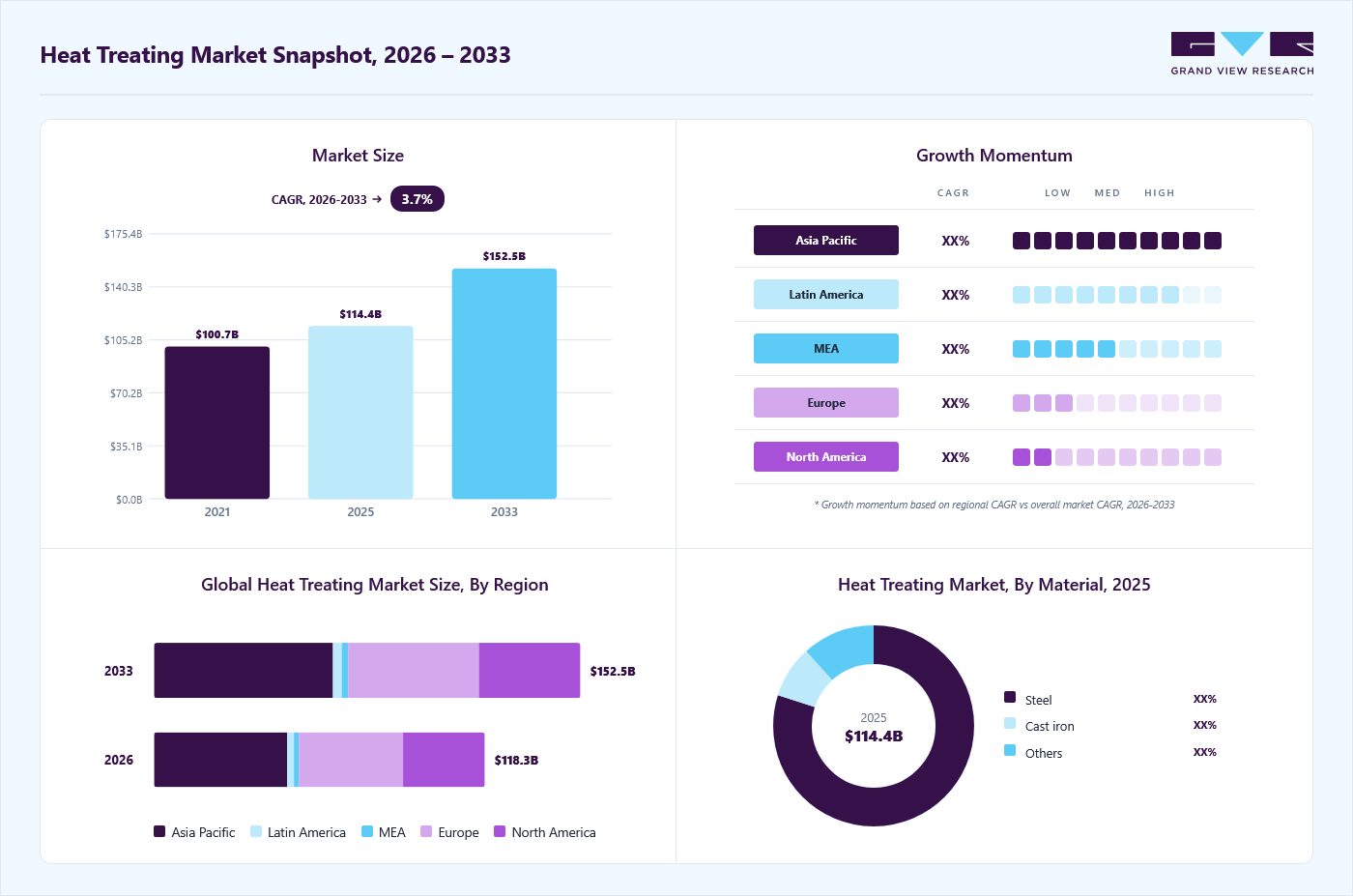

The global heat treating market size was valued at USD 96.1 billion in 2025 and is projected to grow from USD 99.3 billion in 2026 to USD 128.1 billion by 2033, at a CAGR of 3.7% from 2026 to 2033. Asia Pacific dominated the market, accounting for the largest revenue share of 42.3% in 2025. The global market is witnessing steady growth, driven by the increasing demand for high-performance materials in automotive, aerospace, construction, and industrial manufacturing sectors.

Key Market Trends & Insights

- By material: Steel segment led the market with the largest revenue share of 80.0% in 2025.

- By process: Case hardening segment led the market with the largest revenue share of 33.6% in 2025.

- By equipment: Electrically heated furnace segment led the market with the largest revenue share of 50.4% in 2025.

- By application: Automotive segment led the market with the largest revenue share of 34.6% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (42.3% revenue share, 2025)

- By country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 96.1 Billion

- Estimated market size in 2026: USD 99.3 Billion

- Projected market size by 2033: USD 128.1 Billion

- CAGR (2026-2033): 3.7%

Technological advancements in furnace design, automation, and process control have significantly improved efficiency, energy consumption, and output quality, further fueling market expansion. Moreover, expanding industrialization in emerging economies such as China, India, and Brazil is significantly boosting the demand for heat-treated components. The construction, heavy machinery, and energy sectors require durable parts, which rely on heat treatment for enhanced durability. Continuous advancements in furnace technologies and energy-efficient systems are also attracting industry adoption. Furthermore, stringent quality standards in manufacturing processes are increasing reliance on precise and controlled heat treatment techniques.")

Market Dynamics

The heat treating market is experiencing steady growth driven by increasing demand for high-performance metal components across automotive, aerospace, construction, energy, and industrial machinery sectors. Heat treatment processes play a critical role in enhancing hardness, strength, wear resistance, fatigue life, and dimensional stability of metals, making them indispensable in modern manufacturing. Growing adoption of advanced alloys, lightweight materials, and precision-engineered components is encouraging manufacturers to invest in sophisticated heat treatment technologies.

The automotive and aerospace sectors increasingly rely on heat-treated components to meet stringent requirements related to durability, safety, fuel efficiency, and operational performance. Components such as gears, crankshafts, bearings, landing gear assemblies, turbine parts, and structural elements require precise thermal processing to achieve desired mechanical properties. As vehicle manufacturers focus on improving powertrain efficiency and reducing component failure rates, demand for advanced heat treatment services continues to rise.

The transition toward electric vehicles and next-generation aircraft is further strengthening the need for specialized heat treatment solutions. Lightweight alloys and advanced steel grades require controlled thermal processing to maintain strength while reducing weight. Consequently, manufacturers are expanding heat treatment capacities and adopting modern furnace technologies to support the production of high-value engineered components across these industries.

Heat treating operations involve prolonged exposure to elevated temperatures, resulting in substantial energy consumption and operational expenditures. Rising electricity, natural gas, and fuel prices significantly affect production costs, particularly for facilities operating large-scale furnace systems. In addition, stringent environmental regulations regarding emissions and energy efficiency require continuous investments in equipment upgrades and process optimization. These factors can reduce profit margins for service providers and create challenges for small and medium-sized heat treatment companies seeking to remain competitive.

The increasing focus on sustainability and manufacturing efficiency is creating significant opportunities for advanced heat treatment technologies. Manufacturers are investing in electrically heated furnaces, induction heating systems, vacuum heat treatment, and digitally controlled thermal processing solutions that offer improved energy efficiency, reduced emissions, and superior process consistency. These technologies help industries meet environmental targets while enhancing product quality and operational productivity.

Market Concentration & Characteristics

The global heat treating market is moderately fragmented, with the presence of several regional and international players competing across various segments. While a few large companies hold significant market share, numerous small and mid-sized firms operate in niche areas or specific geographies. This competitive landscape drives innovation and price competition among players. However, ongoing consolidation trends may gradually increase market concentration over time.

The heat treating market demonstrates a steady pace of innovation, driven by the need for energy-efficient, precise, and automated systems. Developments in advanced furnace designs, real-time monitoring, and smart control technologies are reshaping operations. Integration of AI and IoT is enhancing process, optimization, and quality assurance. These innovations are helping manufacturers meet evolving performance and sustainability standards.

Mergers and acquisitions in the heat treating industry are moderate but growing, as larger players seek to expand capabilities and geographic reach. Companies are acquiring specialized firms to enhance their technological edge and service offerings. M&A activity is also fueled by the need to access emerging markets and consolidate fragmented supply chains. This trend supports business scalability and competitiveness.

Environmental regulations play a significant role in shaping the heat treating industry, particularly regarding emissions and energy use. Governments are enforcing stricter standards to reduce carbon footprints and improve workplace safety. Compliance drives adoption of cleaner technologies and modernized equipment. Regulatory pressure encourages sustainable practices but can increase operational costs for smaller firms.

Analyst Perspective

The heat treating market is expected to witness steady growth over the coming years, driven by increasing demand for high-strength, wear-resistant, and durable metal components across automotive, aerospace, industrial machinery, construction, energy, and defense sectors. As manufacturers continue to prioritize component performance, operational efficiency, and product longevity, heat treatment remains a critical value-added process within metal manufacturing. The growing adoption of advanced alloys, lightweight materials, and precision-engineered components is further accelerating demand for sophisticated heat treatment technologies.

Drivers, Opportunities & Restraints

Based on material, steel segment led the market with the largest revenue share of 79.9% in 2025. The global heat treating market is driven by rising demand from automotive, aerospace, and industrial machinery sectors for durable and high-performance components. Growth in electric vehicle production is further boosting the need for specialized thermal processing. Technological advancements in furnace design and process automation also support market expansion. Additionally, the trend toward lightweight materials requires advanced heat treatment solutions.

Emerging economies offer significant growth opportunities due to rapid industrialization and infrastructure development. Increasing adoption of Industry 4.0 technologies opens new possibilities for smart heat treating systems. Demand for customized heat treatment services is rising among end users with specific material requirements. Expansion into renewable energy and defense sectors also presents new avenues for market players.

High initial investment and maintenance costs of advanced heat treating equipment can limit adoption, especially among small-scale firms. Stringent environmental regulations may increase operational burdens and require costly upgrades. Lack of skilled labor in handling complex thermal processes poses a challenge in several regions. Additionally, fluctuations in raw material prices can impact overall profitability.

Material Insights

The steel material segment led the market and accounted for 80.0% revenue share in 2025. This dominance is primarily driven by the rising demand for heat-treated steel components across key industries, particularly construction, automotive, and heavy machinery. Countries such as the U.S., China, and India are witnessing a surge in infrastructure development, which in turn is fueling the need for high-strength, wear-resistant steel parts. Heat treatment is essential in enhancing the mechanical properties of steel, including strength, surface hardness, wear resistance, and machinability. These advantages make steel the most widely treated material in the industry, and continued demand from downstream sectors is expected to further propel the growth of this segment over the forecast period.

Cast iron is expected to witness growth at a significant rate in the heat treating market over the forecast period, owing to its rising use in heavy-duty applications such as engine blocks, machinery bases, and piping. Improvements in heat treating techniques have enabled better control over cast iron’s strength and brittleness. Its cost efficiency and ability to withstand high-temperature conditions make it attractive for industrial use. Growing demand from foundries and energy sectors is accelerating its adoption.

Process Insights

Based on process, case hardening segment led the market with the largest revenue share of 33.6% in 2025, due to their ability to create a hard, wear-resistant surface while maintaining a tough, ductile core. This makes it ideal for high-stress components like gears, shafts, and fasteners in the automotive and machinery industries. The process enhances fatigue strength and extends component life. Its widespread industrial use and reliability contribute to its leading market position.

Annealing is the significantly growing process segment in the market, driven by increasing demand for improved ductility and stress relief in metals. It is particularly important in electronics, construction, and metal fabrication industries. Advancements in controlled atmosphere annealing are enabling better quality and efficiency. The process supports the production of softer, more workable materials suited for further manufacturing.

Equipment Insights

Based on equipment, electrically heated furnace segment led the market with the largest revenue share of 50.4% in 2025, due to their precise temperature control, energy efficiency, and cleaner operation. They are widely used in industries where consistency and environmental compliance are critical. These furnaces support automation and are well-suited for small to medium-sized components. Their low emissions and reduced operating costs contribute to their dominant position.

Fuel-fired furnaces are the significantly growing segment, driven by their high heating capacity and cost-effectiveness for large-scale industrial applications. They are preferred in heavy industries such as steel, foundries, and power generation due to faster processing times. Technological improvements are enhancing combustion efficiency and emission control. Their ability to handle large batches makes them attractive in high-volume production settings.

Application Insights

Based on application, automotive segment led the market with the largest revenue share of 34.6% in 2025, due to its high demand for durable, high-performance metal components. Heat treatment is essential for parts like gears, crankshafts, and suspension systems to improve strength and wear resistance. The growing production of vehicles, including electric models, continues to fuel this demand. Cost-effective and scalable processes make heat treatment a key step in automotive manufacturing.

The aerospace industry is projected to grow fastest in the application segment over the forecast period, driven by the need for lightweight yet high-strength components. Heat treating processes are critical for ensuring the reliability and fatigue resistance of aircraft parts under extreme conditions. Increasing global air travel and defense investments are boosting the production of aircraft and related components. Strict quality standards in aerospace further amplify the need for advanced heat treatment solutions.

Regional Insights

North America heat treating market is growing at a significant CAGR of 3.1% in the global market, driven by strong automotive, aerospace, and defense industries. The presence of advanced manufacturing facilities and a focus on technological innovation drive demand. Strict quality and environmental regulations encourage the adoption of efficient heat treating processes. The U.S. remains the primary contributor due to its well-established industrial base.

U.S. Heat Treating Market Trends

The U.S. dominates the North American market due to its strong presence in automotive, aerospace, and defense manufacturing. Advanced technologies and high production standards drive consistent demand for thermal processing. The country has a well-developed industrial infrastructure and a skilled workforce. Additionally, investments in R&D and automation support its leading position.

Canada heat treating market is witnessing steady growth, supported by its expanding automotive and heavy machinery sectors. The country’s focus on advanced manufacturing and export-oriented industries is boosting demand for treated metal components.

Europe Heat Treating Market Trends

Europe heat treating market is a key player in the global market, driven by the region’s focus on high-precision engineering and sustainable manufacturing. Countries like Germany, France, and Italy have strong automotive and aerospace sectors requiring advanced thermal processing. Technological upgrades and energy-efficient practices are widely adopted across the region. Supportive regulations and R&D investments further strengthen Europe’s market position.

Germany heat treating market is a key growth market in Europe due to its strong engineering, automotive, and aerospace sectors. The country’s focus on precision manufacturing drives demand for advanced heat treating processes. Continuous investment in industrial automation and green technologies supports market expansion. Additionally, Germany’s export-oriented economy boosts the need for high-quality, heat-treated components.

The United Kingdom heat treating market is experiencing growth, driven by its aerospace, defense, and automotive industries. Increased adoption of advanced materials and manufacturing technologies is fueling demand for specialized thermal treatment. Government support for innovation and sustainable manufacturing is aiding the industry’s development. The presence of global OEMs and high-value production further strengthens market prospects.

Asia Pacific Heat Treating Market Trends

Asia Pacific dominated the heat treating market with the largest revenue share of 42.3% in 2025, owing to rapid industrialization and the large-scale presence of automotive and electronics manufacturing. China, Japan, South Korea, and India are major contributors with expanding production capacities. Cost-effective labor and increasing investments in infrastructure support market growth. Rising demand for consumer goods and machinery further fuels the need for heat treating services.

The heat treating market in the China held the largest share in the Asia Pacific region in 2025. China is experiencing strong growth in the heat treating market due to its massive manufacturing base across the automotive, electronics, and machinery sectors. Rapid industrialization and infrastructure development continue to drive demand for treated metal components. Government initiatives to upgrade industrial capabilities and promote high-end manufacturing are boosting technology adoption. Domestic demand and export growth are key factors propelling the market forward.

India heat treating market is growing steadily, supported by expanding automotive, railways, and heavy engineering industries. The government's "Make in India" initiative is encouraging local manufacturing and foreign investments in industrial sectors. Rising demand for cost-effective and durable metal components is fueling the adoption of heat treating processes. Additionally, improvements in infrastructure and technology accessibility are accelerating market development.

Middle East & Africa Heat Treating Market Trends

The Middle East and Africa heat treating market is experiencing steady growth due to infrastructure development and investments in the oil & gas and construction sectors. Countries like Saudi Arabia and South Africa are adopting more advanced manufacturing technologies. The need for corrosion-resistant and high-performance components is boosting heat treating demand. However, limited local manufacturing capacity presents challenges to faster market expansion.

Saudi Arabia heat treating market is witnessing growth, driven by expanding oil & gas, construction, and infrastructure sectors. The country's push for industrial diversification under Vision 2030 is encouraging investments in manufacturing and metal processing. Demand for corrosion-resistant and high-strength components is rising in energy and heavy equipment applications.

Latin America Heat Treating Market Trends

The Latin America heat treating market is witnessing gradual growth, driven by developments in the automotive and mining industries. Brazil and Argentina are emerging as key markets with increasing industrial activity. Demand for durable and heat-treated components is rising alongside regional manufacturing expansion. However, growth is moderated by economic and infrastructure challenges.

Brazil heat treating market is experiencing growth due to its expanding automotive, mining, and agricultural machinery industries. Rising domestic manufacturing and infrastructure projects are boosting demand for durable metal components. The country’s industrial sector is increasingly adopting modern thermal processing technologies to improve product quality. Government efforts to attract foreign investment further supporting market development.

Key Heat Treating Company Insights

Some key players operating in the market include Bluewater Thermal Solutions LLC, American Metal Treating Inc., and East-Lind Heat Treat Inc.

-

Bluewater Thermal Solutions operates a network of specialized heat treating and brazing facilities across North America. The company caters to various sectors, including automotive, aerospace, and energy, offering localized processing capabilities. Its services range from vacuum heat treating and carburizing to specialized processes like boronizing and fastener treatment. By tailoring services to regional market demands, it ensures both technical precision and quick turnaround.

-

Based in North Carolina, American Metal Treating Inc. focuses on precision thermal processing for high-performance components. It utilizes advanced vacuum furnaces and high-pressure quenching to minimize distortion in critical alloys. The company primarily serves industries such as defense, aerospace, and motorsports, where quality and reliability are essential. Their use of controlled digital systems ensures consistent results and compliance with strict customer specifications.

Key Heat Treating Companies:

The following key companies have been profiled for this study on the heat treating market.

-

Bluewater Thermal Solutions LLC

-

American Metal Treating Inc.

-

East-Lind Heat Treat Inc.

-

General Metal Heat Treating, Inc.

-

Shanghai Heat Treatment Co. Ltd.

-

Pacific Metallurgical, Inc.

-

Nabertherm GmbH

-

Unitherm Engineers Limited

-

SECO/WARWICK Allied Pvt. Ltd.

-

Triad Engineers

-

HighTemp Furnaces Limited

-

Deck India Engineering Pvt. Ltd.

-

Sourabh Heat Treatments

-

AFECO Heating Systems

-

THERELEK

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (e.g., Nabertherm GmbH, SECO/WARWICK Allied Pvt. Ltd., Bluewater Thermal Solutions LLC, American Metal Treating Inc., Shanghai Heat Treatment Co. Ltd., Pacific Metallurgical, Inc.)

Focus on continuous investment in advanced furnace technologies, automation, and energy-efficient heat treatment solutions.

Strengthen long-term partnerships with automotive, aerospace, industrial machinery, and defense manufacturers through integrated service offerings.

Extensive technical expertise, strong brand reputation, and proven capabilities in handling high-precision heat treatment requirements.

Broad geographic presence and large-scale processing capacity enable servicing of diverse industries and high-volume projects.

High capital expenditure and operating costs associated with maintaining sophisticated heat treatment infrastructure.

Greater exposure to fluctuations in industrial production cycles and energy prices due to large-scale operations.

Emerging & Regional Players (e.g., East-Lind Heat Treat Inc., General Metal Heat Treating, Inc., Unitherm Engineers Limited, Triad Engineers, HighTemp Furnaces Limited, Deck India Engineering Pvt. Ltd.)

Emphasize customized heat treatment services tailored to regional manufacturing requirements and niche applications.

Compete through flexible pricing models, quicker turnaround times, and customer-focused technical support.

Strong responsiveness to local customer needs and the ability to adapt rapidly to changing market demands.

Lower operational complexity enables efficient servicing of small and medium-sized manufacturing clients.

Limited investment capacity for advanced heat treatment technologies and large-scale facility expansion.

Smaller geographic footprint and lower brand visibility compared to established global market participants.

Recent Developments

-

In July 2025, Nitrex began expanding its Aurora, Illinois facility in July 2025 to support rising demand in heat treatment services. The new building will include a modern low-pressure carburizing furnace with oil quenching. This upgrade targets high-spec needs in automotive and aerospace sectors. Full operations are expected to start after construction completion.

-

In November 2024, FPM Heat Treating expanded its capacity by adding a high-performance vacuum furnace from Solar Manufacturing. The system meets strict industry standards and handles heavy loads at high temperatures. This upgrade strengthens FPM’s service offerings across key industries like aerospace, automotive, and medical.

-

In January 2024, SECO/WARWICK expanded its production capacity in 2023 to meet rising global demand for heat treating equipment. The company enhanced its facilities and added new production lines across key technology segments. This move aims to boost delivery efficiency and support long-term growth.

-

In December 2023, SECO/WARWICK has supplied a Vector vacuum furnace to Yalman Knives, a Turkish manufacturer specializing in knives and industrial rolls. The equipment will be used for hardening and tempering tool steel with high precision. This custom solution supports Yalman’s need for consistent heat treatment quality. It reflects SECO/WARWICK’s commitment to serving specialized production needs with advanced technology.

Heat Treating Market Report Scope

Report Attribute

Details

Market size in 2025

USD 96.1 billion

Estimated market size in 2026

USD 99.3 billion

Projected market size by 2033

USD 128.1 billion

Growth rate

CAGR of 3.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, process, equipment, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; Italy; Spain; UK; China; Japan; India; South Korea; Argentina; Brazil; Saudi Arabia; UAE

Key companies profiled

Bluewater Thermal Solutions LLC; American Metal Treating Inc.; East-Lind Heat Treat Inc.; General Metal Heat Treating, Inc.; Shanghai Heat Treatment Co. Ltd.; Pacific Metallurgical, Inc.; Nabertherm GmbH; Unitherm Engineers Limited; SECO/WARWICK Allied Pvt. Ltd.; Triad Engineers; HighTemp Furnaces Limited; Deck India Engineering Pvt. Ltd.; Sourabh Heat Treatments; AFECO Heating Systems; THERELEK.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Heat Treating Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global heat treating market report based on material, process, equipment, application, and region.

-

Material Outlook (Revenue, USD Billion, 2021 - 2033)

-

Steel

-

Cast iron

-

Others

-

-

Process Outlook (Revenue, USD Billion, 2021 - 2033)

-

Case hardening

-

Hardening & tempering

-

Annealing

-

Normalizing

-

Others

-

-

Equipment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Electrically heated furnace

-

Fuel-fired furnace

-

Others

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Automotive

-

Machine

-

Construction

-

Aerospace

-

Metalworking

-

Others

-

-

Region Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

Italy

-

Spain

-

UK

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Research Methodology

The heat treating market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each heat treating segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Material

Revenue Capture Definition

Steel

Revenue is generated from heat treatment services and processes applied to carbon steel, alloy steel, stainless steel, and specialty steel components to enhance hardness, strength, wear resistance, and durability across industrial applications.

Cast iron

Includes revenues derived from heat treatment of cast iron components used in machinery, automotive, construction, and industrial equipment to improve machinability, toughness, and dimensional stability.

Others

Covers revenues associated with thermal processing of non-ferrous metals such as aluminum, copper, and brass for improved mechanical properties, conductivity, corrosion resistance, and performance characteristics.

Process

Revenue Capture Definition

Case hardening

Revenue includes heat treatment solutions that harden the outer surface of metal components while maintaining a tough core, commonly used in gears, bearings, shafts, and automotive parts.

Hardening & tempering

Covers revenues from processes that increase material hardness followed by tempering to achieve the required balance of strength, toughness, and fatigue resistance.

Annealing

Includes revenues generated from controlled heating and cooling processes designed to improve ductility, relieve internal stresses, and enhance machinability of metal products.

Normalizing

Revenue is derived from normalizing treatments used to refine grain structure, improve uniformity, and enhance mechanical properties in ferrous metal components.

Others

Covers revenues from specialized heat treatment techniques focused on reducing residual stress, improving surface characteristics, and optimizing material performance for specific industrial requirements.

Equipment

Revenue Capture Definition

Electrically heated furnace

Includes revenues from heat treatment operations conducted using electrically powered furnaces, widely adopted for precise temperature control, energy efficiency, and consistent processing quality.

Fuel-fired furnace

Revenue is generated from heat treatment systems utilizing natural gas, oil, or other fuel sources, particularly for large-scale and high-temperature industrial applications.

Others

Covers revenues associated with advanced heating technologies that provide rapid, localized, and highly controlled thermal processing for precision manufacturing applications.

Application

Revenue Capture Definition

Automotive

Revenue includes heat treatment of engine components, transmission parts, gears, shafts, bearings, and structural components to improve performance, safety, and durability.

Machine

Covers revenues from thermal processing of industrial machinery components requiring enhanced wear resistance, fatigue strength, and operational reliability.

Construction

Includesrevenues generated from heat treatment of structural steel, fasteners, tools, and heavy equipment parts used in construction and infrastructure projects.

Aerospace

Revenue is derived from heat treatment of aerospace-grade metals and components requiring high strength, lightweight performance, dimensional stability, and compliance with stringent industry standards.

Metalworking

Covers revenues from treating cutting tools, dies, molds, and fabricated metal products to improve hardness, precision, and service life.

Others

Includes revenues generated from heat treatment services for specialized components used in rail transport, marine vessels, medical devices, power generation equipment, and defense systems requiring superior mechanical performance and reliability.

Estimation Model

Layer Name

Key Question

Description

End-Use Industry Demand Layer

Which industries generate demand for heat-treated metal components?

Demand is assessed across automotive, aerospace, construction, machinery, metalworking, rail, shipbuilding, medical, energy, and defense sectors where heat treatment is required to improve mechanical properties and component performance.

Technology Adoption Layer

Which heat treatment processes and materials are being increasingly utilized?

Analysis evaluates adoption of case hardening, hardening & tempering, annealing, normalizing, surface hardening, and stress-relieving processes across steel, cast iron, aluminum, copper, brass, and other engineered materials.

Equipment Deployment Layer

What types of heat treatment equipment are installed and utilized across industries?

Market sizing is derived from the deployment of electrically heated furnaces, fuel-fired furnaces, induction systems, plasma furnaces, laser furnaces, and other advanced thermal processing equipment used in manufacturing operations.

Revenue Layer

What revenue is generated from heat treatment equipment and processing activities?

Final market revenue is calculated by analyzing equipment utilization, heat treatment volumes, processing requirements, technology penetration, and spending across major end-use industries and geographic markets.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Market Intelligence and Strategic Assessment

Delivered a comprehensive market research study covering global market sizing, historical analysis, forecast projections, pricing trends, supply chain evaluation, regulatory landscape, technology advancements, investment trends, and macroeconomic factors influencing the Heat Treating Market. The report also included regional and country-level assessments to provide a holistic view of industry developments and future growth prospects.

Enabled the client to gain a complete understanding of market evolution, growth opportunities, industry risks, and strategic business considerations across the entire value chain, supporting long-term planning and investment decisions.

Segment-Level Analysis and Growth Opportunity Identification

Provided detailed analysis across all major market segments and sub-segments, including material types, heat treatment processes, equipment categories, and end-use applications. The study evaluated revenue contribution, adoption trends, demand patterns, technological shifts, and future growth potential across each segment and key geographic markets.

Helped identify the most lucrative segments, emerging demand centers, technology transition areas, and untapped growth opportunities, allowing the client to prioritize investments and optimize market positioning strategies.

Competitive Landscape, Industry Structure, and Strategic Benchmarking

Delivered an in-depth assessment of market participants, including company profiling, market participant categorization, competitive benchmarking, market share assessment, strategic developments, expansion initiatives, technology capabilities, mergers & acquisitions, and innovation trends shaping the competitive environment.

Provided actionable competitive intelligence to benchmark industry leaders, evaluate market positioning, understand competitive dynamics, and formulate effective growth, partnership, product development, and market expansion strategies.

Frequently Asked Questions About This Report

The rapid growth of the electric vehicle industry, coupled with the growing demand for metallurgical alterations to suit specific applications, is expected to boost the market growth over the forecast period.

Some of the key players operating in the heat treating market include Bluewater Thermal Solutions LLC, American Metal Treating Inc., East-Lind Heat Treat Inc., General Metal Heat Treating, Inc., Shanghai Heat Treatment Co. Ltd., Pacific Metallurgical, Inc., Nabertherm GmbH, Unitherm Engineers Limited, SECO/WARWICK Allied Pvt. Ltd., Triad Engineers, HighTemp Furnaces Limited, Deck India Engineering Pvt. Ltd., Sourabh Heat Treatments, AFECO Heating Systems, THERELEK

The global heat treating market size was estimated at USD 96.1 billion in 2025 and is expected to be USD 99.3 billion in 2026.

The global heat treating market, in terms of revenue, is expected to grow at a compound annual growth rate of 3.7% from 2026 to 2033 to reach USD 128.1 billion by 2033.

Asia Pacific dominated the heat treating market with the largest revenue share of 42.3% in 2025.

The case hardening segment accounted for the largest revenue share of 33.6% in 2025.

The automotive segment accounted for the largest revenue share of 34.6% in 2025.

The steel segment led the market with the largest revenue share of 80.0% in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.