- Home

- »

- Next Generation Technologies

- »

-

Generative AI Market Size, Share, Growth Report, 2026-2033GVR Report cover

![Generative AI Market (2026 - 2033)Report]()

Generative AI Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Software, Service), By Technology (GANs, Transformers, Variational Auto-encoders, Diffusion Networks), By End Use, By Application, By Model, By Customers, By Region, And Segment Forecasts

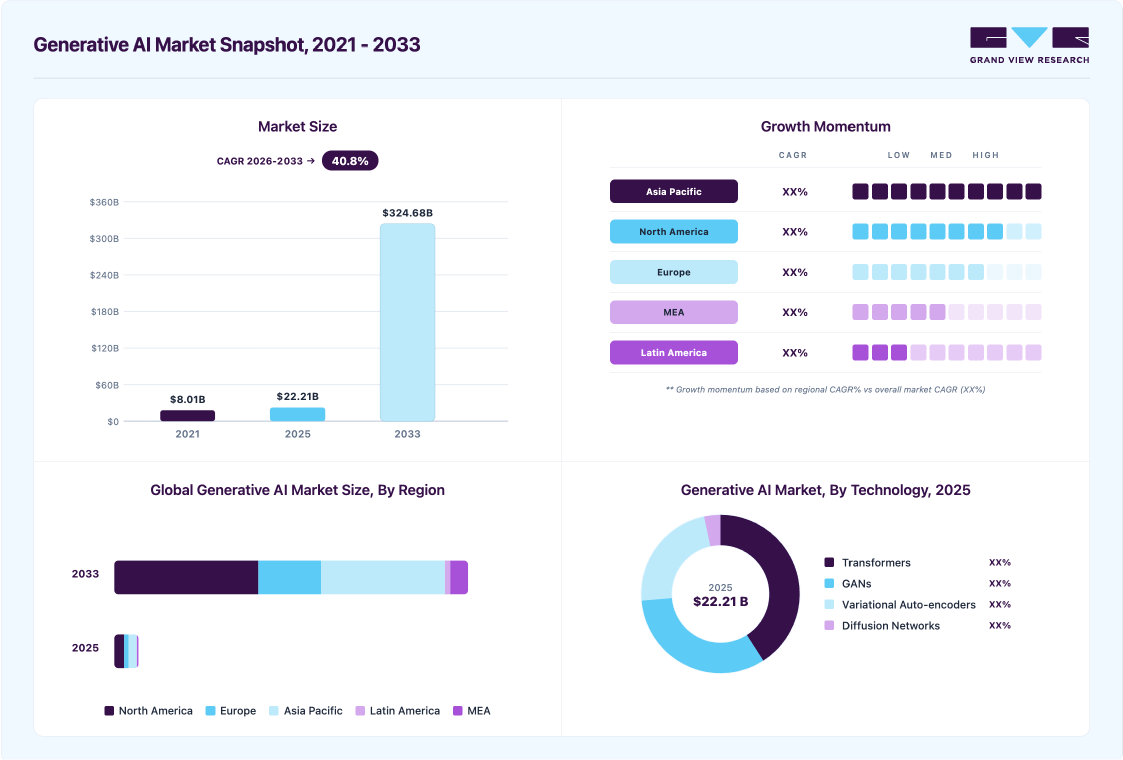

Market Size, 2025

$22.2BMarket Estimate, 2026

$29.6BMarket Forecast, 2033

$324.7BCAGR, 2026–2033

40.8%Generative AI Market Summary

The global generative AI market size was valued at USD 22.2 billion in 2025 and is projected to grow from USD 29.6 billion in 2026 to USD 324.7 billion by 2033, at a CAGR of 40.8% from 2026 to 2033. North America accounted for the largest revenue share of 40.8% in 2025. The demand for generative AI applications across industries is being driven by factors such as the expanding use of technologies such as super-resolution, text-to-image conversion, and text-to-video conversion, along with a growing need to modernize workflows.

Key Market Trends & Insights

- By component: Software segment held the largest revenue share of 64.1% in 2025.

- By technology: Transformers segment dominated the market with the largest share of 40.9% in 2025.

- By end use: BFSI segment is expected to grow at the fastest CAGR of 43.2% from 2026 to 2033.

Regional Highlights

- Largest regional market: North America (40.8% revenue share, 2025)

- By country: The U.S. generative AI market held the largest share of North America in 2025.

Market Size & Forecast

- Market size in 2025: USD 22.2 Billion

- Estimated market size in 2026: USD 29.6 Billion

- Projected market size by 2033: USD 324.7 Billion

- CAGR (2026-2033): 40.8%

This trend shows the increasing importance of AI-driven solutions in enhancing operational efficiency and innovation across various sectors. Generative AI uses unverified learning algorithms for tasks such as spam detection, image compression, and data preprocessing, including noise reduction in visual data. Supervised learning algorithms are essential for medical imaging and image classification. These technologies are applied in industries such as BFSI, healthcare, automotive and transportation, IT and telecommunications, and media and entertainment. Generative AI enables organizations to generate new ideas, solve complex problems, and develop innovative products. It also saves time and costs, increase efficiency, and improve content quality.")

The growth of cloud storage solutions has accelerated the generative AI market by providing a strong foundation for technology development and deployment. Cloud storage delivers scalable computing power, allowing businesses to train resource-intensive generative AI model training without substantial capital investment. It enhances data accessibility and collaboration, enabling global teams to efficiently store and share diverse datasets. The pay-as-you-go model reduces financial barriers and supports secure management of sensitive AI projects. Cloud platforms also offer pre-trained models and APIs, streamlining development and optimizing resources.

Market Dynamics

The increasing demand for AI copilots and virtual assistants across various industries is accelerating the global adoption of generative AI technologies. Organizations are deploying AI-powered assistants to automate routine workflows, improve employee productivity, and enhance operational efficiency across multiple business functions. AI copilots are being integrated into customer service, software development, healthcare, finance, sales, and enterprise collaboration platforms to facilitate real-time decision-making and task execution. The need for intelligent automation, rapid information retrieval, and personalized user experiences is prompting organizations to invest in advanced generative AI solutions. Additionally, ongoing advancements in natural language processing, contextual reasoning, and multimodal AI capabilities are strengthening the commercial adoption of AI copilots across sectors.

Organizations are leveraging virtual assistants and AI copilots to reduce operational costs, optimize workforce utilization, and streamline enterprise processes. The adoption of hybrid work environments and digital workplace transformation initiatives is generating strong demand for AI-driven collaboration and productivity tools. Furthermore, businesses are employing generative AI assistants to improve customer engagement through conversational interfaces, automated support systems, and personalized recommendations. Technology providers are introducing industry-specific AI copilots tailored to sectors such as healthcare, banking, financial services and insurance (BFSI), retail, manufacturing, and education, thereby expanding market opportunities. Increased investments by major technology companies in enterprise AI ecosystems and intelligent assistant platforms are expected to drive sustained growth in the generative AI market..

Rising concerns regarding data privacy and security risks are emerging as significant restraints for the growth of the generative AI market. Organizations are increasingly cautious about deploying generative AI solutions due to the potential exposure of sensitive business information, confidential customer data, and proprietary intellectual property during AI model training and usage. The growing use of cloud-based AI platforms and large-scale data processing systems has heightened concerns related to cybersecurity vulnerabilities, unauthorized access, and data leakage incidents. In highly regulated industries such as healthcare, BFSI, government, and legal services, strict compliance requirements surrounding data governance and privacy protection are further limiting large-scale AI adoption. Additionally, concerns regarding the misuse of AI-generated outputs, deepfakes, and synthetic content manipulation are creating reputational and operational risks for enterprises.

Enterprises are also facing challenges associated with ensuring transparency, accountability, and secure handling of data across generative AI ecosystems. The absence of standardized global regulations and evolving legal frameworks for AI governance is creating uncertainty for organizations planning long-term AI investments. Many businesses remain hesitant to integrate generative AI into mission-critical operations due to concerns surrounding model bias, unauthorized data retention, and potential violations of regional privacy laws. Furthermore, increasing incidents of cyberattacks targeting AI infrastructure and concerns related to third-party AI service providers are compelling enterprises to strengthen security protocols and compliance measures. As a result, rising investments in AI risk management, data protection infrastructure, and regulatory compliance activities may increase operational complexities and restrain the pace of generative AI market expansion.

The growing adoption of AI-driven cybersecurity and threat-detection solutions is creating substantial opportunities in the generative AI market. Organizations across various industries are employing generative AI to reinforce cybersecurity frameworks, detect advanced threats, and enhance real-time incident response. The escalating frequency of ransomware attacks, phishing campaigns, data breaches, and sophisticated cyber threats is driving demand for advanced AI-based security platforms. Generative AI models are utilized to process extensive security data, identify abnormal network behaviors, and automate the generation of threat intelligence with greater speed and accuracy. Additionally, rising investments in proactive cybersecurity infrastructure and AI-enabled security operations centers (SOCs) are expected to drive sustained market expansion.

Organizations are leveraging generative AI solutions to automate vulnerability assessments, fraud detection, identity verification, and compliance monitoring across digital ecosystems. The widespread adoption of cloud computing, remote work environments, and interconnected enterprise systems is intensifying the demand for scalable AI-powered cybersecurity solutions. Technology providers are introducing advanced generative AI-driven security tools that offer predictive analytics, automated remediation, and adaptive threat detection to address evolving cyber risks. Government agencies, financial institutions, healthcare organizations, and critical infrastructure operators are increasingly integrating AI-driven cybersecurity platforms to strengthen resilience against complex attacks. Furthermore, ongoing advancements in machine learning algorithms, behavioral analytics, and autonomous security technologies are projected to generate significant growth opportunities for generative AI vendors worldwide.

Market Concentration & Characteristics

The generative AI market has moderate to high concentration, with leading technology companies, cloud hyperscalers, enterprise software providers, and emerging AI startups competing in foundation models, AI copilots, and enterprise automation solutions. Major players strengthen their positions through investments in proprietary large language models (LLMs), multimodal AI technologies, and large-scale AI infrastructure ecosystems. Established companies benefit from strong enterprise customer relationships, integrated cloud platforms, advanced AI research, and scalable deployment networks worldwide. Meanwhile, emerging vendors differentiate themselves with industry-specific AI applications, lightweight AI models, and agile innovation strategies targeting niche enterprise needs. The growing adoption of AI-powered productivity tools, intelligent assistants, and generative content platforms intensifies competition and drives technological innovation across the market.

Generative AI solutions also compete with open-source AI frameworks, internally developed enterprise AI systems, and conventional automation platforms with limited generative capabilities. Large enterprises with strong in-house AI expertise increasingly develop customized generative AI models to address workflow automation, customer engagement, and business intelligence needs. Some organizations still rely on traditional machine learning models, analytics platforms, and rule-based automation systems instead of advanced generative AI solutions. However, dedicated generative AI platforms keep a strong competitive advantage by offering advanced natural language processing, multimodal content generation, and real-time intelligent automation. Growing enterprise investments in AI adoption, cloud-based AI ecosystems, and personalized digital experiences are expected to support long-term growth and innovation in the generative AI market.

Component Insights

Software segment accounted for the dominant share of 64.1% in 2025. The growth of the software segment in generative AI is driven by factors such as the rise in fraudulent activities, overestimation of capabilities, unexpected outcomes, and increasing concerns about data privacy. Generative AI software is expected to become increasingly significant across various industries, including fashion, entertainment, and transportation, as it gains power through advanced machine learning models. Brands such as H&M and Adidas, for instance, have leveraged generative AI to design clothing and create custom sneakers. Moreover, this technology has been applied to generate unique patterns for fabrics and prints, streamlining the design process and saving time for designers.

The service segment is projected to experience the fastest growth rate during the forecast period. The increasing adoption of advanced technologies such as large language models (LLMs), natural language processing (NLP), deep learning, transformer architectures, and predictive analytics is significantly accelerating demand for generative AI services. Cloud-based generative AI services are anticipated to gain popularity due to their flexibility, scalability, and cost-effectiveness, supported by cloud computing, API-based AI deployment, and model-as-a-service (MaaS) frameworks, fueling the segment's expansion. For instance, in April 2023, Amazon Web Services (AWS), a U.S.-based IT service management company, introduced Amazon Bedrock and a suite of generative AI services. These offerings use foundation models, prompt engineering, and multimodal AI to enable chatbots, text generation, summarization, and image classification, enhancing generative AI capabilities across industries.

Technology Insights

Transformer segment accounted for the dominant share in 2025, largely due to its capacity to handle vast amounts of data efficiently. These models excel in tasks involving natural language processing (NLP), computer vision, multimodal learning, and advanced reasoning, driven by innovations such as self-attention mechanisms, parallel processing, and sequence-to-sequence modeling. Transformer architectures, including large language models (LLMs), foundation models, and generative pre-trained transformers (GPT), enable the learning of complex contextual relationships and semantic representations.

Diffusion networks are gaining momentum in the generative AI market, particularly recognized for their effectiveness in image and video generation. Unlike Transformers, diffusion models progressively refine data by removing noise, which allows for the creation of high-quality, realistic content. Ongoing advancements in latent diffusion, noise scheduling, and computational optimization are improving their speed and efficiency, addressing earlier performance constraints. As a result, the rising adoption of diffusion networks highlights the market’s growing preference for specialized, high-performance generative models tailored to diverse use cases.

End Use Insights

The media and entertainment industry accounted for the dominant share in 2025. The growth is driven as this sector extensively integrates AI for content creation, personalized recommendations, and audience engagement. Generative AI technologies enable companies to develop immersive visuals, synthetic audio, and interactive storytelling experiences, significantly expanding creative possibilities. The integration of AI-driven content personalization, recommendation algorithms, and user behavior analytics allows media firms to deliver tailored experiences, boosting viewer engagement and retention. In addition, the growing adoption of virtual reality (VR), augmented reality (AR), and real-time rendering technologies is further accelerating the demand for generative AI in this sector.

The BFSI segment is seeing significant growth in generative AI adoption, focusing on applications that improve fraud detection, risk analysis, and customer service automation. Financial institutions are beginning to use AI-driven models to analyze complex datasets, identify suspicious patterns, and predict potential risks more accurately. Moreover, generative AI is streamlining customer support by enabling virtual assistants to handle routine inquiries and deliver personalized financial advice. With regulatory compliance becoming increasingly critical, AI models are also being utilized to ensure adherence to data privacy and security standards. The growing integration of generative AI within BFSI showcases the sector’s commitment to enhancing efficiency, security, and customer satisfaction.

Application Insights

Natural language processing (NLP) segment holds a dominant position in 2025, driven by its widespread applications in chatbots, virtual assistants, and content creation. NLP models are highly effective in understanding and generating human-like text, enabling organizations to enhance communication, automate support tasks, and personalize user interactions. These models help businesses analyze customer feedback, interpret complex queries, and provide meaningful responses, contributing to improved user experiences. NLP also supports language translation and sentiment analysis, making it valuable across diverse industries. As a result, NLP continues to be the leading technology in generative AI, shaping how businesses engage with their audiences.

Computer vision is experiencing significant growth within the generative AI market, particularly due to its applications in industries such as healthcare, automotive, and retail. This technology enables machines to interpret and analyze visual data, which is essential for tasks such as medical imaging, autonomous driving, and inventory management. Recent advancements are making computer vision models more efficient, allowing for the generation of highly realistic images and videos. Technology also supports object detection and facial recognition, further enhancing its utility across sectors. As computer vision capabilities advance, it is gaining traction and expanding its role in the generative AI landscape.

Model Insights

Large language models (LLMs) segment continue to lead the generative AI market in 2025, driven by their strong capabilities in content generation, conversational AI, customer support automation, and advanced data analytics. Built on transformer architectures, foundation models, and large-scale training datasets, LLMs deliver highly coherent, context-aware, and human-like responses, making them essential across industries. Their adoption in sectors such as education, healthcare, finance, and enterprise IT highlights their ability to manage complex linguistic and cognitive tasks. Additionally, LLMs play a critical role in sentiment analysis, real-time language translation, text summarization, and knowledge extraction, significantly improving user engagement and accessibility. This sustained leadership positions LLMs as a core driver of innovation and large-scale deployment in the generative AI ecosystem.

Multi-modal generative models segment is expected to witness strong growth over the forecast period, driven by their ability to process and generate content across multiple data formats, including text, images, audio, and video. Leveraging advancements in cross-modal learning, vision-language models (VLMs), and multimodal transformers, these models are gaining significant traction in industries such as e-commerce, media & entertainment, and education. Furthermore, continuous improvements in model alignment, data fusion techniques, and computational efficiency are enhancing their performance and scalability. As a result, the increasing adoption of multi-modal models reflects the market’s shift toward more versatile and sophisticated generative AI solutions capable of handling complex, cross-media interactions.

Customers Insights

App builders segment stand as the dominant customer segment within the generative AI market in 2025, driven by their need to integrate AI capabilities into applications across industries. These companies rely on generative AI to create innovative features such as personalized recommendations, automated customer support, and dynamic content generation, adding significant value to their applications. App builders are increasingly focused on enhancing user engagement and improving functionality, and generative AI provides the tools to achieve this efficiently. By incorporating AI-driven insights and interactions, app builders can meet growing customer expectations for responsive, intelligent applications. This demand reinforces the position of app builders as key customers driving generative AI advancements.

Model builders segment is increasingly using generative AI within this market, focusing on creating and refining advanced AI architectures for diverse applications. These builders play a crucial role in developing foundational models, optimizing them for efficiency, accuracy, and scalability. Model builders are essential in advancing generative AI’s capabilities, working on everything from language and vision models to complex multi-modal frameworks. Their work supports the broader ecosystem by enabling app builders to leverage robust, pre-trained models for specific use cases. As the demand for sophisticated AI grows, model builders are integral to the generative AI landscape, providing the backbone for new, impactful applications.

Regional Insights

North America Generative AI market leads the global market accounting for leading share of 40.8% in 2025. The region’s growth can be attributed to the high investment levels and a strong ecosystem of technology companies and research institutions. The region is witnessing rapid adoption across sectors such as healthcare, finance, and entertainment, as organizations seek to enhance productivity and create innovative solutions. Regulatory developments in data privacy and AI ethics are shaping the market, encouraging responsible AI adoption. In Canada, there is a particular focus on AI research and government support for AI-driven innovation. North America’s emphasis on advanced technology positions it as a major hub for generative AI development.

U.S. Generative AI Market Trends

In the U.S., generative AI is widely used across industries, from media and entertainment to finance and healthcare. The country is home to leading AI companies and research facilities driving advancements in language, vision, and multi-modal AI technologies. There is also significant investment from both private and public sectors, fueling the growth and adoption of generative AI. Government interest in establishing ethical standards and ensuring AI safety is impacting the regulatory sector.

Europe Generative AI Market Trends

In Europe, the generative AI market is expanding, bolstered by supportive government policies and an emphasis on ethical AI. The European Union has set guidelines to ensure that AI is transparent, fair, and accountable, which influences AI deployment across industries. Key industries such as automotive, finance, and retail are actively exploring generative AI to improve customer experience and operational efficiency. Several European countries, including Germany and France, are investing in AI research to strengthen their positions in the global market.

Asia Pacific Generative AI Market Trends

In Asia-Pacific, the generative AI market is witnessing rapid growth, driven by technological advancements and increasing adoption across industries. Countries such as China, Japan, and South Korea are investing heavily in AI, aiming to lead in areas like autonomous systems, robotics, and digital transformation. Generative AI is widely used in sectors such as e-commerce, manufacturing, and media, where automation and personalization are in high demand. Governments in the region are actively supporting AI research and development, fueling a competitive market environment.

Key Generative AI Company Insights

Some of the key companies in the Generative AI market include Adobe, Amazon Web Services, Inc., D-ID, Genie AI Ltd., Google LLC and others. Organizations are focusing on increasing customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Amazon Web Services, Inc. (AWS) has developed Amazon Bedrock, offering pre-trained foundational models for building generative AI applications. AWS provides cloud-based solutions for businesses to create chatbots, summarize text, and generate images. It offers APIs and model training resources customized to various industry needs. AWS’s scalable infrastructure supports businesses in deploying and expanding generative AI models efficiently.

-

Google LLC focuses on generative AI with models such as Bard and Gemini, advancing large language and multi-modal systems. Google integrates generative AI into its products, including Google Workspace, to enhance productivity with AI-powered writing and visual tools. It also emphasizes responsible AI use with guidelines for ethical implementation. Google’s ongoing research continues to expand generative AI’s capabilities in enterprise and consumer settings.

Key Generative AI Companies:

The following key companies have been profiled for this study on the generative AI market.

- Adobe

- Amazon Web Services, Inc.

- D-ID

- Genie AI Ltd.

- Google LLC

- IBM

- Microsoft

- MOSTLY AI Inc.

- Rephrase.ai

- Synthesia

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Adobe, Amazon Web Services, Inc., Google LLC, IBM, Microsoft

- Mature players are increasingly integrating generative AI copilots with enterprise productivity, cybersecurity, and cloud ecosystems to strengthen platform adoption.

- Leading companies are heavily investing in multimodal AI, autonomous AI agents, and proprietary large language models to expand enterprise capabilities.

- Their competitive advantage is supported by large-scale cloud infrastructure and high-performance AI computing ecosystems.

- Strong global enterprise customer networks and extensive R&D investments enable faster commercialization of advanced AI technologies.

- Increasing regulatory scrutiny related to AI governance, data privacy, and ethical AI practices may create compliance challenges.

- Dependence on large-scale computing infrastructure may expose companies to rising energy consumption and supply chain risks..

Emerging Players: D-ID, Genie AI Ltd., MOSTLY AI Inc., Rephrase.ai, Synthesia

- Emerging players are increasingly developing niche generative AI applications tailored for specific enterprise and industry use cases.

- AI startups are leveraging open-source AI frameworks and cloud-native architectures to accelerate market entry and scalability.

- Emerging vendors often benefit from innovation-focused business models and streamlined operational structures.

- Their competitive edge is driven by agile product development and faster adoption of emerging AI technologies.

- Limited financial resources and restricted access to high-performance AI infrastructure may constrain scalability.

- Intense competition from established technology companies may create barriers to long-term market penetration and profitability.

Recent Developments

-

In January 2026, Infosys announced a strategic collaboration with Amazon Web Services (AWS) to accelerate enterprise adoption of generative AI. The partnership focuses on integrating Infosys Topaz, an AI-first suite of services and platforms, with Amazon Q Developer, AWS’s generative AI-powered assistant, to enhance internal operations and drive innovation across industries such as manufacturing, telecom, financial services, and consumer goods

-

In November 2024, Amazon Web Services (AWS) collaborated with partners, including Booz Allen Hamilton and Crayon, to launch the Generative AI Partner Innovation. This collaboration aims to expand the reach of the Generative AI Innovation Center and help customers build and deploy AI solutions by utilizing industry-specific expertise and proven methodologies to scale generative AI initiatives globally.

-

In September 2024, IBM and Oracle Corporation, a U.S.-based computer software company, collaborated to enhance Oracle clients' use of generative AI by combining IBM's expertise in technologies such as OCI Generative AI, Watsonx, and third-party models. Through this partnership, IBM is helping clients maximize ROI and reduce compute costs.

-

In October 2024, Adobe expanded its Firefly generative AI to include video to provide creative professionals with new tools for generating and editing content in Photoshop, Illustrator, and Premiere Pro. These updates, available in a limited public beta, enable users to generate videos from text prompts and create faster, more refined images and designs.

Generative AI Market Report Scope

Report Attribute

Details

Market size in 2025

USD 22.2 billion

Estimated Market size in 2026

USD 29.6 billion

Projected Market size by 2033

USD 324.7 billion

Growth rate

CAGR of 40.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Million/Billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segment scope

Component, technology, end use, application, model, customers, region

Region scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; Australia, South Korea, Brazil, KSA, UAE, South Africa

Key companies profiled

Adobe; Amazon Web Services, Inc.; D-ID; Genie AI Ltd.; Google LLC; IBM; Microsoft; MOSTLY AI Inc.; Rephrase.ai; Synthesia

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Generative AI Market Report Segmentation

This report offers revenue growth forecasts at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global Generative AI market report based on component, technology, end use, application, model, customers, and region:

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Software

-

Service

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Generative Adversarial Networks (GANs)

-

Transformers

-

Variational Auto-encoders

-

Diffusion Networks

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Media & Entertainment

-

BFSI

-

IT & Telecommunication

-

Healthcare

-

Automotive & Transportation

-

Gaming

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Computer Vision

-

NLP

-

Robotics & Automation

-

Content Generation

-

Chatbots & Intelligent Virtual Assistants

-

Predictive Analytics

-

Others

-

-

Model Outlook (Revenue, USD Million, 2021 - 2033)

-

Large Language Models

-

Image & Video Generative Models

-

Multi-modal Generative Models

-

Others

-

-

Customers Outlook (Revenue, USD Million, 2021 - 2033)

-

Model Builders

-

App Builders

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Product Positioning & Competitive Intelligence

Benchmarking of large language models (LLMs), multimodal AI solutions, and enterprise AI copilots

Comparative analysis of pricing models, deployment strategies, and AI platform capabilities

Enterprise perception study related to AI productivity, automation, and customer engagement tools

Competitor analysis focusing on innovation pipelines, acquisitions, and strategic partnerships

Improved AI product differentiation and competitive positioning strategies

Supported pricing optimization and monetization planning

Identified evolving enterprise requirements and emerging AI use cases

Strengthened market competitiveness through innovation-led intelligence

Customer & End-User Insights Study

Enterprise AI adoption readiness and digital transformation assessment

End-user behavior analysis for AI-driven automation, conversational AI, and intelligent assistants

Customer satisfaction and productivity impact evaluation across enterprise workflows

Pain-point analysis related to AI scalability, model reliability, cybersecurity, and compliance concerns

Revealed key adoption accelerators and deployment barriers across industries

Supported customer-centric AI solution development and engagement strategies

Improved enterprise retention and long-term adoption planning

Identified upselling opportunities for advanced AI-enabled business solutions

Technology & Innovation Assessment

Emerging technology trend analysis covering autonomous AI agents, multimodal AI, and synthetic data generation

Evaluation of AI infrastructure ecosystems including GPUs, cloud AI, and high-performance computing platforms

Patent analysis and innovation tracking for next-generation generative AI technologies

Ecosystem mapping of AI developers, semiconductor providers, cloud vendors, and enterprise software companies

Identified future technology investment opportunities and innovation hotspots

Supported long-term AI roadmap and commercialization strategies

Evaluated scalability and competitive readiness of emerging AI technologies

Strengthened strategic collaboration and ecosystem partnership planning

Frequently Asked Questions About This Report

North America dominated the generative AI market with a share of 40.8% in 2025. This is attributable to the existence of leading companies researching & developing generative AI applications.

Some key players operating in the generative AI market include Adobe, Amazon Web Services, Inc., D-ID, Genie AI Ltd., Google LLC, IBM, Microsoft, MOSTLY AI Inc., Rephrase.ai, Synthesia

Key factors include the expanding use of technologies like super-resolution, text-to-image conversion, and text-to-video conversion, along with a growing need to modernize workflows.

The software segment dominated the generative AI industry, accounting for over 64.1% of revenue in 2025.

Transformer segment accounted for the dominant share in 2025.

The media and entertainment industry accounted for the dominant share in 2025.

Large language models (LLMs) segment continues to lead the generative AI market in 2025.

App builders segment stand as the dominant customer segment within the generative AI market in 2025.

The global generative AI market size was valued at USD 22.2 billion in 2025 and is expected to reach USD 29.6 billion in 2026.

The global generative AI market is expected to grow at a compound annual growth rate of 40.8% from 2026 to 2033 to reach USD 324.7 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.