- Home

- »

- Communications Infrastructure

- »

-

Fixed Wireless Access Market Size And Share Report, 2033GVR Report cover

![Fixed Wireless Access Market Size, Share & Trends Report]()

Fixed Wireless Access Market (2026 - 2033) Size, Share & Trends Analysis Report By Offering, By Operating Frequency (Hardware, Services), By Demography (Urban, Semi-Urban), By Technology (4G, 5G), By Application, By Region, And Segment Forecasts

Market Size, 2025

$183.8BMarket Estimate, 2026

$213.1BMarket Forecast, 2033

$1,119.0BCAGR, 2026–2033

26.7%Fixed Wireless Access Market Summary

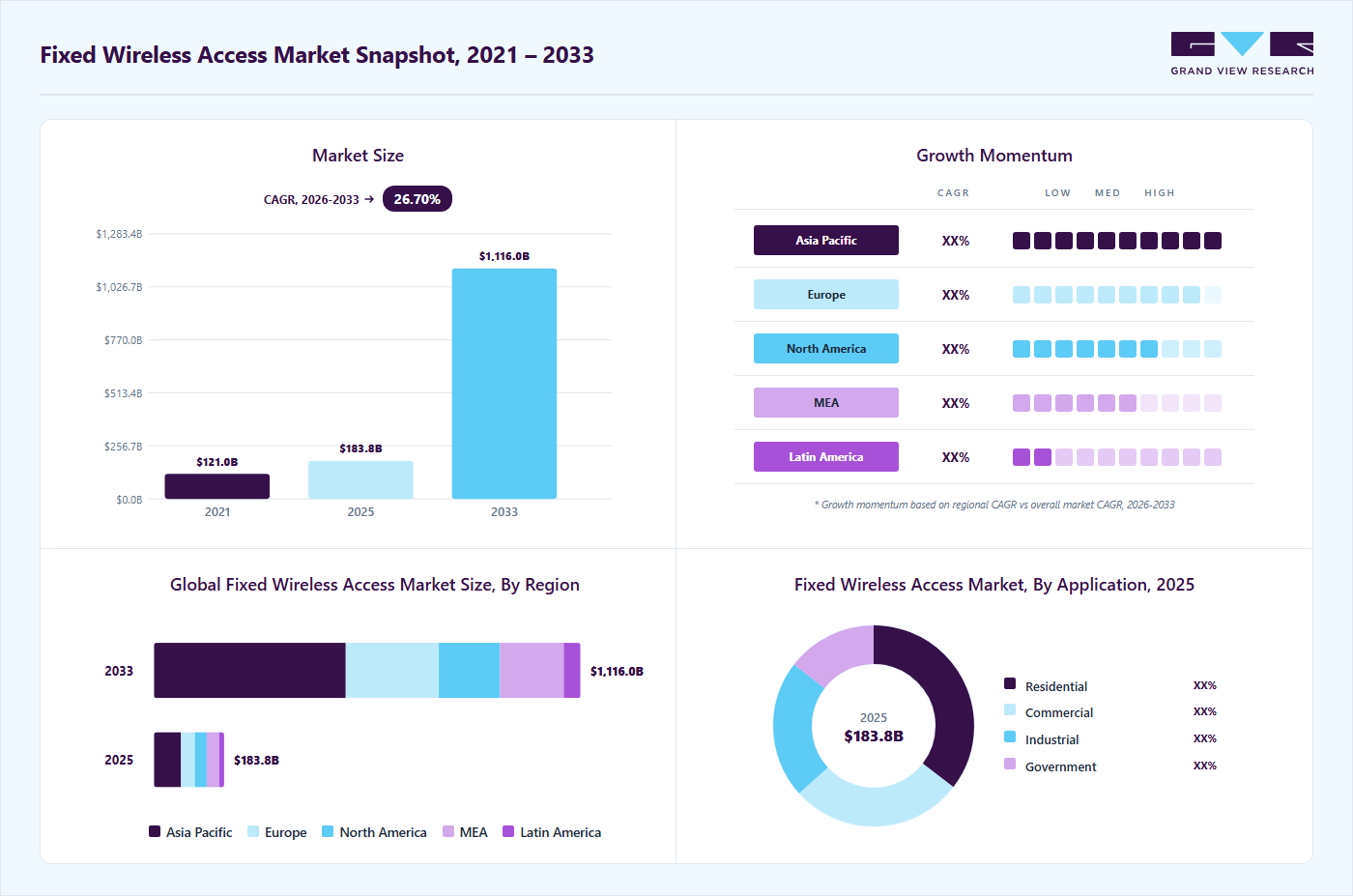

The global fixed wireless access market size was valued at USD 183.8 billion in 2025 and is projected to grow from USD 213.1 billion in 2026 to USD 1,116 billion by 2033, at a CAGR of 26.7% from 2026 to 2033. Asia Pacific dominated the global fixed wireless access market with the largest revenue share of 38.6% in 2025. The accelerated deployment of 5G infrastructure is a major factor expected to drive the growth of the fixed wireless access industry.

Key Market Trends & Insights

- By offering: Services segment led the market with the largest revenue share of 57.9% in 2025.

- By operating frequency: Sub-6 GHz segment accounted for the largest market revenue share in 2025.

- By demography: urban segment accounted for the largest market revenue share in 2025.

- By technology: 4G segment accounted for the largest market revenue share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (38.6% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 183.8 Billion

- Estimated market size in 2026: USD 213.1 Billion

- Projected market size by 2033: USD 1,116 Billion

- CAGR (2026-2033): 26.7%

FWA utilizes cellular networks to deliver high-speed internet connectivity. This capability allows telecom operators to extend broadband coverage to millions of households without extensive civil construction or fiber deployment.")

For instance, according to Telefonaktiebolaget LM Ericsson, during Q2 2025, Jio became the largest global FWA provider by the number of connections, with 9.5 million as of Q3 2025. Also, the advanced capabilities of 5G, including lower latency, higher bandwidth, and significantly faster data transmission compared with 4G LTE, have enhanced the reliability and performance of FWA services. These improvements have positioned FWA as a practical alternative to wired broadband, particularly in regions where fiber deployment involves high capital expenditure or logistical challenges.

Increasing demand for high-speed internet connectivity in rural regions is expected to support market growth. Low population density and high installation cost remain the major factors challenging the deployment of traditional wired infrastructure, such as fiber or cable, in rural or underserved regions. Also, demand for digital services, including remote work, online education, video streaming, and cloud-based applications, has intensified the need for affordable broadband solutions. This presents new opportunities for the fixed wireless access industry.

The high capital investment required for wired broadband infrastructure is a key factor driving the growing adoption of Fixed Wireless Access (FWA), which offers a more cost-efficient broadband deployment model. According to the GSMA, wireless broadband solutions can reduce last-mile infrastructure costs by approximately 60-70% compared with fiber deployments, making them highly attractive to telecom operators seeking to expand broadband coverage in low-density, geographically challenging regions. FWA significantly reduces the need for extensive physical infrastructure, such as underground cabling, trenching, and complex last-mile installations, thereby lowering both deployment costs and rollout timelines.

Furthermore, the increasing adoption of remote work, digital learning, and cloud-based enterprise operations has accelerated the demand for reliable and high-speed digital connectivity. This growing dependence on digital services is driving the need for flexible broadband solutions that can be deployed rapidly across diverse geographic environments. In response, telecom operators are increasingly adopting FWA, as it offers a scalable, reliable, and adaptable connectivity solution that meets evolving consumer and enterprise broadband requirements. Consequently, these factors are expected to support the continued growth of the fixed wireless access industry.

Market Dynamics

The increasing adoption of private 5G networks across industrial and enterprise environments is driving growth in the 5G security market by enabling organizations to deploy dedicated, high-performance communication infrastructure tailored to mission-critical operations. Enterprises across manufacturing, energy, logistics, healthcare, mining, and defense sectors are increasingly investing in private 5G networks to support industrial automation, real-time analytics, connected machinery, and autonomous systems. While these networks offer enhanced speed, low latency, and improved operational control, they also significantly expand the cybersecurity surface area, creating strong demand for advanced security solutions.

The deployment of private 5G networks introduces complex security challenges due to the convergence of IT and operational technology (OT) environments, as well as the increasing use of IoT devices, edge computing systems, and cloud-native applications. These interconnected ecosystems require robust protection against unauthorized access, data breaches, and sophisticated cyberattacks targeting critical infrastructure. As a result, organizations are increasingly adopting advanced 5G security frameworks, including zero-trust architectures, network slicing security, identity and access management, and AI-driven threat detection systems.

Limited network coverage and performance challenges in high-density environments are restraining the growth of the Fixed Wireless Access (FWA) market by affecting service reliability and user experience. FWA performance is highly dependent on network availability, spectrum capacity, and signal strength, which can vary significantly across geographic regions. In densely populated urban areas, network congestion and spectrum limitations may reduce connection speeds and increase latency, particularly during peak usage periods. In addition, physical obstructions such as buildings, terrain, and unfavorable weather conditions can negatively impact signal transmission and network stability.

The increasing digital transformation across industries and the expansion of smart connected ecosystems are creating significant growth opportunities for the Fixed Wireless Access (FWA) market by accelerating the demand for reliable, scalable, and high-speed wireless connectivity solutions. Enterprises, residential users, and public sector organizations are increasingly adopting digital technologies such as cloud computing, IoT devices, smart home systems, remote collaboration platforms, and connected industrial applications, which require robust broadband infrastructure. FWA offers a flexible, cost-effective solution that supports these growing connectivity requirements without extensive wired infrastructure deployment.

The rapid adoption of smart city initiatives, Industry 4.0 technologies, and connected enterprise environments is further driving the need for advanced wireless broadband services. In addition, increasing investments in private 5G networks, edge computing, and AI-enabled applications are expanding the use cases for FWA across sectors such as manufacturing, healthcare, logistics, education, and retail.

Market Concentration & Characteristics

The fixed wireless access market is fragmented, with numerous telecom operators, wireless internet service providers (WISPs), network infrastructure vendors, and customer premises equipment (CPE) manufacturers competing across global and regional markets. Fragmentation is particularly high in emerging economies and rural broadband segments, where regional telecom providers and local internet service companies actively deploy FWA solutions to address connectivity gaps. The relatively lower infrastructure deployment requirements compared with traditional fiber networks have enabled a broad range of service providers to enter the market and expand broadband access in underserved and geographically challenging areas.

The market is also characterized by increasing strategic partnerships, spectrum investments, and technology collaborations aimed at strengthening service capabilities and expanding geographic reach. Telecom operators are partnering with network equipment providers, cloud service companies, and chipset manufacturers to improve network performance, enhance customer experience, and accelerate FWA rollout timelines. In addition, infrastructure vendors are introducing advanced routers, antennas, and plug-and-play CPE devices to improve broadband accessibility and operational efficiency.

Offering Insights

The services segment led the market with the largest revenue share of 57.9% in 2025 and is projected to grow at the fastest CAGR during the forecast period. The shift towards subscription-based models is driving the growth of the segment. Many service providers are adopting subscription-based pricing for their FWA offerings, which include ongoing connectivity access and related services such as network security, customer support, and equipment leasing. This model provides customers with a predictable and manageable cost structure while ensuring continuous service updates and enhancements. For providers, subscription models offer a steady and recurring revenue stream, enhancing profitability and financial stability.

The hardware segment is expected to register at a significant CAGR from 2026 to 2033. The evolution of CPE, with improvements in design, functionality, and performance, significantly drives the market's growth. Modern CPE devices are now equipped with advanced features such as dual-band Wi-Fi, mesh networking, and enhanced security protocols, improving the user experience and the reliability of connectivity. The increasing adoption of these sophisticated CPE devices by both residential and business customers is contributing to the expansion of the hardware segment.

Operating Frequency Insights

The sub-6 GHz segment accounted for the largest market revenue share in 2025. The Sub-6 GHz frequency bands, which include the spectrum below 6 GHz, are widely available and have been extensively used in various wireless communication technologies, including 4G LTE and early 5G deployments. This availability has made the Sub-6 GHz segment highly attractive for FWA applications. Many telecom operators already possess licenses for these frequency bands, allowing them to deploy FWA services quickly and cost-effectively.

The above 39 GHz segment is expected to grow at the fastest CAGR during the forecast period. The increasing demand for high-capacity broadband services is driving the segment's growth. Consumers and businesses seek faster and more reliable internet connections to support bandwidth-intensive applications, such as cloud computing, online gaming, video conferencing, and streaming services. FWA solutions operating in the above 39 GHz range are well-suited to meet this demand, as they can deliver high speed with low latency, comparable to or even exceeding traditional fiber-optic connections.

Demography Insights

The urban segment accounted for the largest market revenue share in 2025. Urban areas are dynamic environments where the demand for connectivity can change rapidly due to population growth, new business developments, and increased reliance on digital services. Fixed wireless access offers the flexibility to quickly deploy and scale internet services to meet these changing demands. Unlike wired solutions requiring extensive planning and construction, FWA can be deployed rapidly using cellular infrastructure. This agility is particularly beneficial in urban settings, where gaps in coverage or spikes in demand may require quick responses.

The semi-urban segment is expected to register at the fastest CAGR from 2026 to 2033. Semi-urban areas often have a mix of residential, commercial, and small industrial zones, each with varying connectivity needs. FWA is adaptable to diverse requirements, offering tailored solutions for homes, small businesses, and community institutions such as schools and healthcare centers. The versatility of FWA in addressing different use cases within semi-urban environments further drives its adoption. As businesses in semi-urban areas increasingly rely on digital tools and services, the demand for reliable broadband supporting these activities has grown, making FWA an attractive option for service providers and consumers.

Technology Insights

The 4G segment accounted for the largest market revenue share in 2025. The extensive network coverage drives the market's growth. Over the past decade, telecom operators have invested heavily in expanding 4G infrastructure, resulting in widespread availability across urban, suburban, and rural areas. This extensive coverage makes 4G a highly accessible and practical solution for providing broadband internet through FWA. As a result, FWA services leveraging 4G technology can reach a broad customer base, driving their adoption across markets.

The 5G segment is expected to grow at the fastest CAGR from 2026 to 2033. The superior performance and capabilities offered by the 5G network drive the segment's growth. 5G provides significantly higher data speeds, lower latency, and greater network capacity, which is crucial for delivering high-quality broadband services through FWA. The enhanced performance of 5G enables internet speeds that exceed those of traditional wired connections, such as fiber-optic and DSL, making FWA a competitive alternative for residential and business users. The ability of 5G to support high-bandwidth applications, including ultra-high-definition video streaming, online gaming, and large-scale IoT deployments, further drives its adoption in the fixed wireless access industry.

Application Insights

The residential segment accounted for the largest market revenue share in 2025. The growing adoption of smart home technologies is driving the popularity of FWA in residential applications. Smart home devices such as security cameras, smart thermostats, voice assistants, and connected appliances require stable and high-speed internet connectivity to function effectively. As more households integrate these devices into their daily lives, the demand for reliable broadband, such as fixed wireless access, that can support multiple connected devices simultaneously, is increasing.

The commercial segment is expected to register at the fastest CAGR from 2026 to 2033. Fixed wireless access is well-suited for temporary or pop-up business operations, such as construction sites, event venues, or seasonal businesses. These operations often require quick and temporary internet solutions that can be set up and dismantled with minimal hassle. FWA offers the perfect solution, providing high-speed internet without needing permanent infrastructure. Businesses can deploy FWA to support short-term projects, mobile offices, or temporary retail locations, ensuring they have the connectivity they need to operate efficiently. This ease of deployment and flexibility of FWA make it an attractive option for businesses with temporary or mobile operations, thus driving its growth in commercial applications.

Regional Insights

The fixed wireless access market in North America is poised for significant growth from 2026 to 2033. The growing adoption of Internet of Things (IoT) devices and smart technologies in residential and commercial settings drives the growth of the FWA market in North America. Smart homes, connected businesses, and industrial IoT applications require reliable and high-capacity internet connections to function effectively. FWA offers a robust solution for these needs, providing the bandwidth and low latency to support a wide range of connected devices, from smart thermostats and security systems to industrial sensors and machinery.

U.S. Fixed Wireless Access Market Trends

The fixed wireless access market in the U.S. is anticipated to register at a significant CAGR from 2026 to 2033. The shift towards remote work and the increasing reliance on digital services, accelerated by the COVID-19 pandemic, contribute to the growth of FWA in the U.S.

Asia Pacific Fixed Wireless Access Market Trends

Asia Pacific dominated the global fixed wireless access market with the largest revenue share of 38.6% in 2025 and is projected to grow at the fastest CAGR during the forecast period. The large and rapidly growing population, rising adoption of 5G technology, and increasing digitalization drive the market growth in the Asia Pacific.

The fixed wireless access market in China accounted for the largest market revenue share in the Asia Pacific in 2025. China's FWA momentum is closely tied to the sheer density of its 5G macro and small-cell networks, which now span millions of sites. This vast infrastructure base enables operators to deploy FWA at unprecedented scale and cost-effectively, seamlessly bundling it with smart-home and household broadband packages. As a result, FWA is evolving into a mainstream connectivity layer across China’s urban and semi-urban households, complementing the government’s push for ubiquitous high-speed internet.

The Japan fixed wireless access market is anticipated to grow at a significant CAGR during the forecast period. In Japan, FWA is becoming a practical alternative to fiber in newly developing suburban zones where construction timelines or zoning hurdles delay wired builds. Operators leverage Japan’s advanced mmWave rollouts and dense small-cell architecture to deliver high-capacity FWA for residential and commercial users. This approach positions FWA as an ultra-fast, low-friction broadband option, particularly attractive for new housing clusters, commercial complexes, and temporary construction sites.

The fixed wireless access market in India is anticipated to grow at the fastest CAGR during the forecast period, driven by an aggressive operator-led model anchored by JioAirFiber. FWA is emerging as a mass-market broadband product aimed at millions of first-time home internet users, with extremely rapid subscriber onboarding in states such as Uttar Pradesh, Gujarat, and Maharashtra. This model fundamentally alters India’s last-mile economics, enabling high-volume broadband penetration without waiting for costly, slow fiber trenching across dense or irregular urban morphologies.

Europe Fixed Wireless Access Market Trends

The fixed wireless access market in Europe is poised for significant growth from 2026 to 2033. Government efforts to improve network infrastructure in the region drive the market's growth. For instance, the European Commission, through the Horizon 2020 program, committed public funding of more than EUR 700 million (USD 770 million) to support 5G opportunities in the region. Such initiatives are expected to drive the market's growth over the forecast period.

The Germany fixed wireless access market is increasingly using FWA as a deliberate policy-aligned tool to accelerate municipal digital inclusion goals. Local governments and telecom operators are adopting FWA to close broadband gaps faster than fiber civil works allow, especially across semi-rural and exurban municipalities where trenching timelines remain politically sensitive. What started as a stopgap measure is now being integrated into regional digital master plans as a parallel connectivity track alongside future fiber deployments.

The fixed wireless access market in the UK is witnessing a competitive repositioning, with FWA packages now framed with premium-grade speed tiers, latency commitments, and bundled content to directly challenge incumbents offering fixed broadband. Operators are targeting suburban churn markets by presenting FWA as a lower-friction home broadband service with rapid installation and performance parity, pushing traditional ISPs to respond with aggressive discounting and upgraded fiber-based plans.

Key Fixed Wireless Access Company Insights

Key players operating in the fixed wireless access industry include Nokia Corporation, AT&T Inc., T-Mobile USA, Inc., CommScope Inc., Verizon Communications Inc., Vodafone Group Plc, Huawei Technologies Co., Ltd., Inseego Corp., Telstra, and FS.com. The fixed wireless access industry is highly competitive, with companies constantly seeking to gain an edge through advanced technological innovations and unique service offerings.

Key Fixed Wireless Access Companies:

The following key companies have been profiled for this study on the fixed wireless access market.

- Nokia Corporation

- AT&T Inc.

- T Mobile USA, Inc.

- CommScope Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- Huawei Technologies Co., Ltd.

- Inseego Corp

- Telstra

- FS.com

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Verizon Communications Inc.; T-Mobile USA, Inc.; Huawei Technologies Co., Ltd.; AT&T Inc.; Nokia Corporation

- Mature players focus on deploying integrated 4G and 5G FWA ecosystems supported by extensive spectrum assets, nationwide network infrastructure, and advanced broadband service offerings.

- • They leverage strategic partnerships with governments, enterprises, and telecom operators to expand broadband coverage across urban, semi-urban, and rural regions.

- Strong global telecom infrastructure presence with extensive broadband subscriber bases and spectrum ownership.

- Ability to provide end-to-end FWA solutions, including network infrastructure, spectrum capabilities, managed services, and customer premises equipment (CPE).

- High infrastructure investment and spectrum acquisition costs may affect profitability and deployment flexibility.

- Complex regulatory approvals and long deployment timelines in certain regions may slow broadband expansion initiatives.

Emerging Players: CommScope Inc.; Vodafone Group Plc; Huawei Technologies Co., Ltd.; Inseego Corp; Telstra; FS.com

- Emerging players focus on specialized FWA solutions such as indoor and outdoor CPE devices, wireless access units, enterprise broadband connectivity, and rural broadband deployment solutions.

- Strategies emphasize flexible, cost-efficient, software-driven, and rapidly deployable broadband technologies tailored for underserved and industrial connectivity applications.

- Strong focus on niche FWA applications, compact deployment models, and cost-effective broadband technologies.

- Faster innovation cycles in customer premises equipment (CPE), wireless access technologies, and enterprise connectivity solutions.

- Limited large-scale telecom infrastructure and smaller geographic presence compared with global telecom leaders.

- Lower brand recognition and limited financial resources for large-scale spectrum investments and network expansion.

Recent Developments

- In June 2023, Nokia Corporation launched a purpose-built FWA receiver tailored for the North American market. The Nokia FastMile 5G receiver features a high-gain antenna to deliver high speeds over extended distances, making it ideal for serving rural and suburban communities with limited access. The receiver supports 5G and 4G bands, including Citizens Broadband Radio Service (CBRS) in either 5G or 4G and C-band.

Fixed Wireless Access Market Report Scope

Report Attribute

Details

Market size in 2025

USD 183.8 billion

Estimated Market size in 2026

USD 213.1 billion

Projected Market size by 2033

USD 1,116 billion

Growth rate

CAGR of 26.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, Volume in Thousand Units, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Offering, operating frequency, demography, technology, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; South Korea; Philippines; Brazil; Kingdom of Saudi Arabia (KSA); UAE; South Africa

Key companies profiled

Nokia Corporation; AT&T Inc.; T Mobile USA, Inc.; CommScope Inc.; Verizon Communications Inc.; Vodafone Group Plc; Huawei Technologies Co., Ltd.; Inseego Corp; Telstra; and FS.com

Customization scope

Free report customization (equivalent to up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fixed Wireless Access Market Report Segmentation

The report forecasts revenue and volume growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global fixed wireless access market report based on offering, operating frequency, demography, technology, and region.

-

Offering Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Hardware

-

Customer Premises Equipment (CPE)

-

Indoor CPE

-

Outdoor CPE

-

-

Access Units

-

Femto Cells

-

Pico Cells

-

-

-

Services

-

-

Operating Frequency Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Sub-6 GHz

-

24-39 GHz

-

Above 39 GHz

-

-

Demography Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Urban

-

Semi-Urban

-

Rural

-

-

Technology Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

4G

-

5G

-

-

Application Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Residential

-

Commercial

-

Industrial

-

Oil & Gas

-

Mining

-

Utility

-

Others

-

-

Government

-

-

Regional Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Philippines

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

UAE

-

Kingdom of Saudi Arabia (KSA)

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Fixed Wireless Access (FWA) Market Opportunity Assessment

Country/region-wise fixed wireless access market sizing and growth forecasts in terms of volume (Thousand Units) and revenue (USD Million) across North America, Europe, Asia Pacific, Latin America, and MEA

Assessment of regulatory frameworks impacting FWA deployment, including spectrum allocation policies, broadband expansion initiatives

Identified region-specific growth opportunities in underserved broadband markets

Supported telecom operators and broadband service providers in network expansion and subscriber growth planning

Fixed Wireless Access Technology & Deployment Behavior Study

Analysis of enterprise and residential FWA adoption patterns across 4G and 5G technologies

Evaluation of operating frequency adoption trends across Sub-6 GHz, 24–39 GHz, and above 39 GHz bands

Improved segmentation of FWA demand by technology, operating frequency, device type, and deployment environment

Supported product positioning for CPE manufacturers and network infrastructure providers

Competitive Benchmarking and Strategic Positioning in the Fixed Wireless Access Market

Comparative assessment of telecom operator partnerships, 5G infrastructure investments, spectrum ownership, subscriber base expansion, and broadband monetization strategies.

Analysis of market share across residential, commercial, industrial, and government end-use applications

Identified competitive white spaces in rural broadband connectivity and high-frequency FWA deployment

Supported strategic partnership development among telecom operators, infrastructure vendors, and CPE providers

Frequently Asked Questions About This Report

The global fixed wireless access market size was estimated at USD 183.8 billion in 2025 and is expected to reach USD 213.1 billion in 2026.

The global fixed wireless access market is expected to grow at a compound annual growth rate of 26.7% from 2026 to 2033 to reach USD 1,116 billion by 2033.

Asia Pacific dominated the fixed wireless access market with a share of 38.6% in 2025.

Some key players operating in the fixed wireless access market include Nokia Corporation; AT&T Inc.; T Mobile USA, Inc.; CommScope Inc.; Verizon Communications Inc.; Vodafone Group Plc; Huawei Technologies Co., Ltd.; Inseego Corp; Telstra; and FS.com.

Key factors that are driving the market growth include the accelerated deployment of 5G infrastructure is a major factor expected to drive the growth of the fixed wireless access industry.

4G segment accounted for the largest market revenue share in 2025.

Services segment led the market with the largest revenue share of 57.9% in 2025.

Urban segment accounted for the largest market revenue share in 2025.

About the Author(s)

Communications Infrastructure Research Team

Technology · Communications InfrastructureThis report was authored by the communications infrastructure research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the communications infrastructure segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.