- Home

- »

- Next Generation Technologies

- »

-

Engineering Services Market Size & Share Report 2026-2033GVR Report cover

![Engineering Services Market (2026 - 2033)Report]()

Engineering Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Engineering Discipline (Civil, Mechanical, Electrical), By Engineering Service Type, By Application (Infrastructure Development, Industrial Projects), By End-use, By Region, And Segment Forecasts

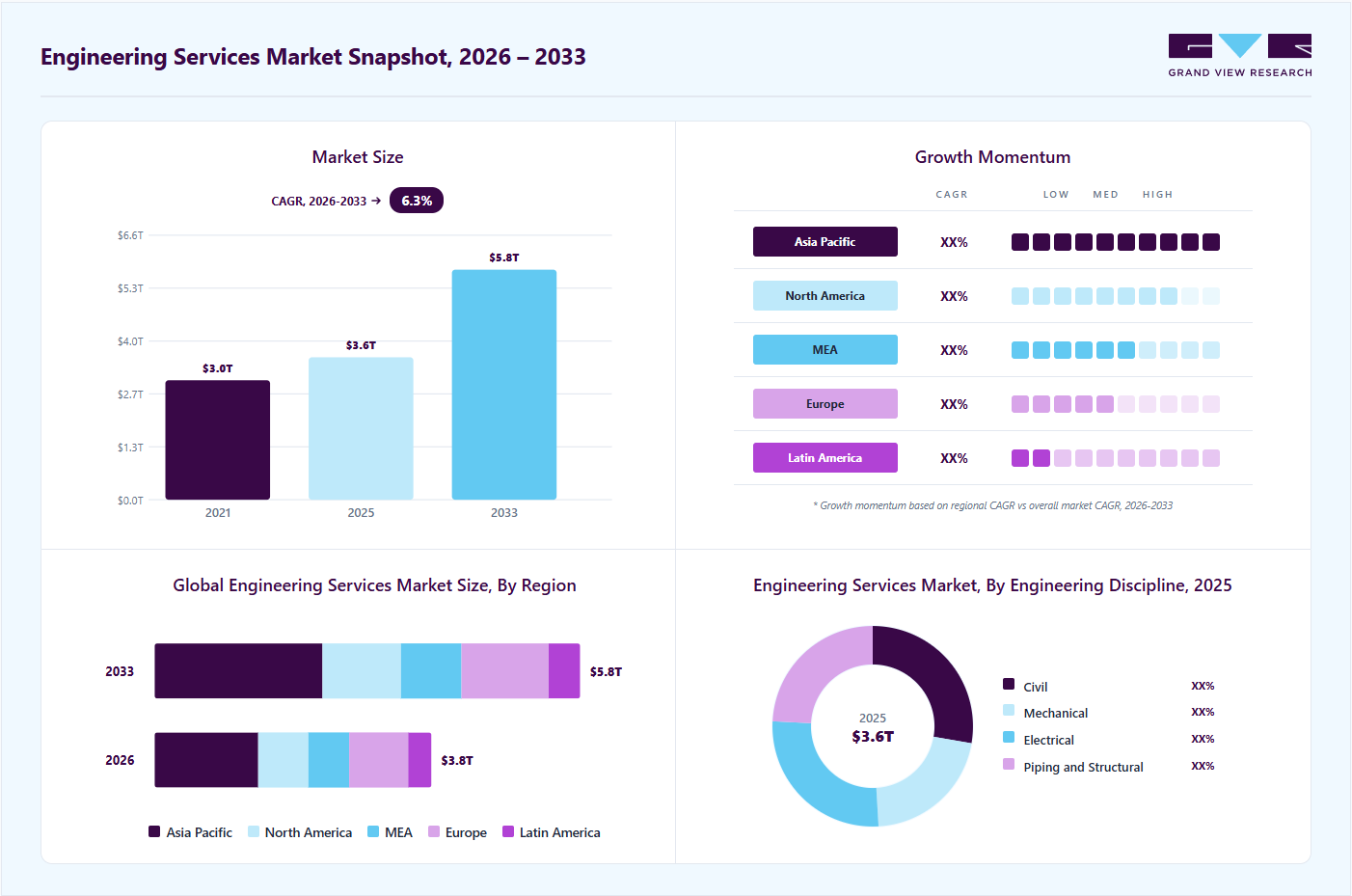

Market Size, 2025

$3,578.2BMarket Estimate, 2026

$3,759.5BMarket Forecast, 2033

$5,778.0BCAGR, 2026–2033

6.3%Engineering Services Market Summary

The global engineering services market size was valued at USD 3,578.2 billion in 2025 and is projected to grow from USD 3,759.5 billion in 2026 to USD 5,778.0 billion by 2033, growing at a CAGR of 6.3% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 37.1% in 2025. The engineering services market is driven by an increasing emphasis on infrastructure modernization and digital transformation across industries, with organizations proactively adopting advanced engineering design tools, simulation technologies, and AI-enabled digital engineering solutions to reduce operational costs and improve planning, development, and execution accuracy for complex industrial projects.

Key Market Trends & Insights

- By engineering service type: Specialized engineering services segment dominated the market, with a share of 19.2% in 2025.

- By engineering discipline: Civil segment accounted for the largest market share of 27.7% in 2025.

- By application: Environmental projects segment held the largest market share in 2025.

- By end use: Telecommunications segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (37.1% revenue share in 2025)

- By Country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 3,578.2 Billion

- Estimated market size in 2026: USD 3,759.5 Billion

- Projected market size by 2033: USD 5,778.0 Billion

- CAGR (2026-2033): 6.3%

Governments are focusing on upgrading transport, water and sanitation, and clean energy infrastructure, leading to a steady demand for engineering design, consulting, and construction-related services. In addition, private sector investments in smart manufacturing, commercial buildings, and data centers are boosting the market. Engineering companies play a crucial role in helping clients meet project deadlines, comply with environmental regulations, and improve cost-effectiveness through integrated services across the planning, design, and execution stages.One significant trend in the international market for engineering services is the growing adoption of digital tools and processes. Technologies such as Building Information Modeling (BIM), digital twins, and AI-driven simulations are transforming the planning and delivery of engineering projects. These innovations promote collaboration, reduce design flaws, and enhance asset lifecycle management. Many companies are investing in software integration and digital infrastructure to automate workflows and improve project visibility. As clients increasingly demand faster delivery and greater accuracy, digital transformation has become central to engineering service offerings for construction, energy, industrial, and infrastructure projects worldwide.

")

Furthermore, there is a growing emphasis on sustainability and regulatory compliance in engineering projects. With more stringent emissions regulations, energy efficiency requirements, and environmental assessment procedures, engineering firms are expanding their services to include green design, renewable energy systems, and low-impact infrastructure planning. These services cover solar and wind project design, sustainable material selection, and energy modeling for buildings and industrial facilities. Customers across various industries-including transportation, utilities, manufacturing, and real estate-are demanding environmentally sustainable project execution, which is consequently altering service scopes and technical specifications in engineering contracts.

Moreover, the Leading Companies in the engineering services sector are actively expanding geographically, enhancing their digital capabilities, and pursuing high-value public and private sector projects. Companies such as AECOM, WSP Global, Jacobs Engineering Group, and Bechtel are engaged in large-scale infrastructure, energy, and urban development projects in North America, Europe, and Asia Pacific. Regional and mid-sized companies are also capitalizing on their specialties in MEP design, environmental consulting, and civil works. Many firms are forming joint ventures, acquiring boutique consultancies, and improving their in-house capabilities to respond more effectively to complex, multi-disciplinary projects in both local and global markets.

Market Dynamics

Engineering services are gaining significant traction, offering advanced capabilities such as digital design and simulation, BIM-based modeling, product lifecycle management, and AI-enabled engineering optimization. These services enable organizations to improve project efficiency, reduce design errors, enhance cost optimization, and ensure higher accuracy in planning, development, and execution of complex infrastructure and industrial projects. The increasing adoption of digital engineering solutions, Industry 4.0 technologies, and cloud-based collaboration platforms, coupled with growing investments in smart infrastructure, renewable energy, and industrial automation, is expected to continue driving growth in the engineering services market.

The market is driven by increasing adoption of digital engineering tools such as BIM, digital twins, AI-based design platforms, and simulation software across infrastructure and industrial projects. Organizations are leveraging these technologies to enhance design precision, streamline workflows, and reduce project execution timelines. Growing complexity of large-scale engineering projects is further pushing firms to adopt integrated engineering services that improve coordination, minimize errors, and support data-driven decision-making throughout the project lifecycle.

The rising investments in smart infrastructure, energy systems, and transportation modernization are strengthening demand for advanced engineering expertise. Companies are increasingly focusing on outsourcing specialized engineering functions to improve operational efficiency and access global talent pools. The shift toward cloud-based collaboration and real-time project monitoring is further enabling seamless execution of complex engineering activities across geographically distributed teams.

The market faces challenges due to a significant shortage of highly skilled engineering professionals proficient in advanced digital tools and multidisciplinary project execution. Engineering services require specialized expertise in design, analysis, and emerging technologies, making talent acquisition and retention increasingly difficult. This skill gap often leads to delays in project delivery, increased training costs, and reliance on a limited pool of experienced professionals, affecting overall service efficiency.

The rapid technological advancements are creating continuous upskilling requirements, increasing operational complexity for service providers. Smaller firms often struggle to match the capabilities of larger players, which have established talent networks and training infrastructure. This imbalance can limit competitiveness and restrict the ability of firms to scale services efficiently across diverse and complex engineering projects.

The market presents strong opportunities as the shift toward integrated engineering service models that combine design, consulting, simulation, and lifecycle management under a unified framework continues. Organizations are increasingly seeking end-to-end solutions that reduce fragmentation, improve coordination, and enhance project visibility. This shift is encouraging service providers to develop comprehensive digital engineering ecosystems that support seamless project execution from concept to completion.

The increasing demand for sustainable infrastructure and energy-efficient systems is creating opportunities for innovative engineering solutions. Service providers can leverage advanced analytics, automation, and cloud platforms to deliver more adaptive and scalable services. Expansion into emerging markets, coupled with rising outsourcing trends, is further enabling firms to diversify their service offerings and strengthen long-term client engagement.

Market Concentration & Characteristics

The engineering services market is moderately fragmented to moderately concentrated, with established global engineering consulting firms, infrastructure design companies, industrial service providers, and emerging digital engineering solution specialists operating alongside a large base of regional and niche service providers. The market is expanding due to increasing demand for complex infrastructure development, rising adoption of digital engineering tools, and growing outsourcing of multidisciplinary engineering functions. Strategic collaborations between design firms, technology providers, and industrial enterprises are becoming increasingly common as organizations focus on improving project efficiency and enhancing design accuracy. Continuous investments in digital twins, BIM platforms, AI-assisted engineering design, cloud-based collaboration systems, and simulation-driven development are emerging as key competitive strategies across the market.

The market is characterized by a high level of innovation, driven by advancements in AI-enabled design automation, generative engineering, real-time simulation modeling, and integrated lifecycle management platforms. The industry is witnessing moderate merger and acquisition activities as large engineering firms acquire niche technology providers and specialized consultancies to strengthen digital capabilities and expand geographic reach. Competition from in-house engineering teams and basic design tools remains moderate, but external engineering services continue to dominate complex, large-scale infrastructure and industrial projects due to their multidisciplinary expertise and scalability. Growing investments in smart cities, renewable energy infrastructure, transportation modernization, and industrial automation are expected to further strengthen demand across the engineering services market.

Analyst Perspective

The engineering services market is positioned at the intersection of rapid infrastructure modernization, industrial automation, and accelerating digital transformation across design and development ecosystems. Growing adoption of advanced technologies such as AI-driven design, digital twins, and Building Information Modeling (BIM), combined with rising global investments in smart cities, energy transition, and transportation infrastructure, is reshaping how engineering projects are planned, executed, and optimized. The strongest long-term competitive advantage will lie with providers that can integrate domain engineering expertise with digital engineering capabilities to deliver faster, more efficient, and sustainability-aligned project outcomes.

Engineering Service Type Insights

Based on engineering service type, the specialized engineering services segment led the market with the largest revenue share of 19.2% in 2025 and is expected to grow at the highest CAGR over the forecast period, driven by consistent demand for project planning, feasibility studies, regulatory advisory, and design optimization across infrastructure, energy, and industrial sectors. Clients now more than ever depend on consulting firms to facilitate regulatory compliance, cost control, and risk mitigation at initial stages of a project. Public sector project work and high-value private development, particularly in developed economies, continue to generate stable income for this segment. The increasing size and complexity of projects and the trend towards holistic planning methodologies have further established consulting services as a key element in the value chain of engineering services.

On the other hand, the specialized engineering services is poised to experience the highest growth during the next few years. This involves sophisticated services in geotechnical, environmental, structural, and systems engineering. Growing technical sophistication in infrastructure and industrial projects is leading clients to hire firms with specialized domain knowledge. Moreover, growing demand for services in renewable energy systems, smart grid infrastructure, water treatment, and advanced manufacturing is opening up opportunities for niche engineering providers. As sustainability, automation, and digital infrastructure increasingly shape project demand, expert engineering capabilities are assuming greater significance in international and regional markets, especially in energy, utilities, and transport markets.

Application Insights

The environmental projects segment dominated the engineering services market in 2024, fueled by rising global focus on sustainability, climate change reduction, and natural resource management. Public sectors, industries, and private organizations are spending heavily on projects related to waste management, water treatment, air quality management, and renewable energy systems. As nations introduce stricter environmental standards, engineering companies are serving to design and implement green infrastructure, environmental cleanups, and green urban planning. As increased awareness of the environmental footprint of building and industrial operations takes effect, this sector is anticipated to remain at the helm of the market for the foreseeable future.

On the other hand, technology implementation segment is registering the fastest growth, driven by the growing adoption of digital solutions and automation in engineering projects. Solutions such as Building Information Modeling (BIM), digital twins, artificial intelligence (AI), and Internet of Things (IoT) are revolutionizing engineering services delivery. These solutions provide enhanced project efficiency, real-time data analysis, and better predictive modeling for infrastructure and industrial projects. The embedding of intelligent systems within buildings, transportation, and energy management is fueling demand for technology implementation services, hence it is among the fastest-growing sectors in the engineering services sector.

End-use Insights

The communications segment is currently leading the market for engineering services, primarily due to the ongoing expansion of 5G networks, data centers, and telecommunications infrastructure worldwide. As the demand for fast internet and connectivity increases, engineering companies play a crucial role in designing and deploying network infrastructure, such as towers, fiber optics, and data storage units. The rising complexity of telecommunications projects, combined with the need for reliable and scalable systems, ensures that this sector continues to drive significant market growth. In addition, the momentum towards smart cities and the growing reliance on interconnected devices further accelerates the demand for specialized engineering services in this field.

The construction segment is experiencing the fastest growth, fueled by a surge in residential, commercial, and public infrastructure projects globally. Rapid urbanization in emerging economies, along with ongoing infrastructure investments in developed economies, is driving the construction industry's expansion. Engineering services related to structural design, civil engineering, project management, and green building practices are in high demand. With an increasing focus on green building certification, energy-efficient designs, and advanced construction methods, the building construction sector is emerging as one of the key drivers of demand for engineering services, making it one of the most rapidly growing end-use segments in the market.

Engineering Discipline Insights

Based on engineering discipline, the civil segment led the market with the largest revenue share of 27.7% in 2025. The civil engineering segment accounts for a significant portion of the engineering services market, primarily due to the high demand for infrastructure development across various sectors, including transportation, water systems, and urban planning. Civil engineers are vital in designing, constructing, and maintaining essential infrastructure projects such as roads, bridges, airports, and public utilities. As governments and the private sector prioritize infrastructure development, civil engineering remains a dominant segment, particularly in emerging markets, where rapid urbanization and industrial growth lead to an increased demand for civil works.

Moreover, the civil engineering discipline is experiencing the fastest growth, driven by a rise in large-scale infrastructure projects, especially in emerging economies. With urbanization accelerating and populations expanding, there is an urgent need for sustainable infrastructure, efficient transportation networks, and resilient buildings. The increasing focus on smart cities, green construction, and climate-resilient infrastructure further boosts the demand for civil engineering services. This trend is particularly evident in regions such as Asia Pacific, where substantial investments in public infrastructure, including roads, bridges, and water systems, are anticipated to continue propelling the sector's rapid growth.

The printed circuit board (PCB) testing automated test equipment segment is projected to experience the highest growth rate during the forecast period. This expansion is primarily driven by the increasing global need for miniature, multilayer, and high-density circuit boards utilized in a broad range of electronic devices. Since PCBs are the backbone of all electronics, their integrity and functionality are of utmost importance. Growing miniaturization, increasingly sophisticated circuit designs, and the inclusion of high-speed signal paths have dramatically increased the challenge of testing accuracy. Automated PCB test equipment assists manufacturers in identifying faults including open circuits, shorts, and component misplacements effectively during in-circuit and functional test phases. In addition, the fast growth in consumer electronics, EV production, and medical electronics is further driving the demand for cutting-edge PCB testing technologies that provide speed, precision, and reliability in high-volume production settings.

Regional Insights

Asia Pacific dominated the engineering services market with the largest revenue share of 37.1% in 2025. The region is expected to witness a significant growth at a CAGR of 6.5%. The Asia Pacific engineering services industry is growing because of increased urbanization, industrialization, and infrastructure investments in emerging as well as developed economies. Governments in nations such as China, India, Japan, and Australia are budgeting for smart cities, renewable energy, and transportation networks. There is demand for engineering services across sectors such as rail, highways, energy, and manufacturing. Public-private partnerships are prevalent, particularly in infrastructure-driven markets. Engineering companies are adjusting to tighter environmental regulations, computer-aided design processes, and automation. As local supply chains become more diversified, numerous companies are also providing product engineering, plant design, and energy systems consulting to respond to changing project and compliance requirements.

The engineering services market in China held the largest share in the Asia Pacific region in 2025. China engineering services market is driven by ongoing urban infrastructure growth, high-speed rail development, and the government push towards renewable energy and digital manufacturing. Engineering companies are engaged in large-scale public works, such as water management, metro networks, and industrial parks. The move to carbon neutrality by 2060 has boosted demand for energy-efficient design and engineering contribution in wind, solar, and hydrogen facilities. Domestic companies usually collaborate with state-owned companies, whereas foreign companies generally participate through joint ventures or technical consulting positions. Implementation of intelligent engineering tools such as BIM and AI-based modeling is on the rise to enhance project efficiency and lifecycle performance.

Engineering services market in India is expanding with countrywide infrastructure growth, manufacturing expansion, and digitization in construction. Government initiatives such as Bharatmala, Smart Cities Mission, and Make in India are fueling demand for civil, structural, and mechanical engineering services. An expanding market for outsourced engineering services in design, simulation, and product development to serve global customers also exists. Renewable energy initiatives and public transport networks such as metro rail and expressways are among the prominent contributors. Multinational and domestic engineering companies are increasing capacity, particularly in Tier 2 towns, and embracing digital engineering processes to facilitate cost-effective and sustainable project delivery.

North America Engineering Services Market Trends

The North America engineering services market is underpinned by continued investment in infrastructure upgrades, renewable energy growth, and digitalization of construction and manufacturing. Public investment in transportation, water infrastructure, and broadband through U.S. federal infrastructure programs is fueling the demand for civil and structural engineering services. Private sector projects in data centers, electric vehicle manufacturing, and smart buildings are also offering opportunities for mechanical, electrical, and systems engineering. Environmental compliance, energy efficiency, and climate resilience are major themes influencing project needs. Engineering companies are also embracing digital technologies such as BIM, GIS, and simulation software to enhance project planning, coordination, and delivery.

U.S. Engineering Services Market Trends

The U.S. engineering services market is witnessing steady growth fueled by infrastructure revitalization, clean energy projects, and investments in advanced manufacturing. Federal efforts such as the Infrastructure Investment and Jobs Act are driving demand for engineering in highways, bridges, public transportation, and water systems. Renewable energy, such as solar, wind, and energy storage, also has rising activity. Investments by the private sector in semiconductor facilities, EV manufacturing facilities, and logistics infrastructure further contribute to market demand. Engineering companies are emphasizing integrated project delivery, sustainability, and digital engineering tools such as BIM, digital twins, and automation to enhance efficiency and comply with regulatory requirements.

Europe Engineering Services Market Trends

The Europe engineering services market is influenced by continued infrastructure development, green energy programs, and intensifying digitalization in industries. Demand is generated primarily through transportation modernization, energy efficiency requirements, and government spending on city development. Western and Northern European countries are concentrating on sustainable infrastructure, while Central and Eastern Europe are experiencing growth in industrial engineering and energy projects. The rise of design-build and EPC contracts is significant, as public and private clients look for integrated solutions. Engineering companies are also increasing offerings in digital twin technology, BIM, and smart infrastructure to meet Europe's changing regulatory and environmental objectives.

The UK engineering services market continues to grow with significant emphasis on decarbonization and renewal of infrastructure. Work on National Infrastructure Strategy projects such as high-speed rail (HS2), upgrade of road networks, and development of offshore wind further propels stable demand. Both design and delivery phases have participation by engineering firms with increasing attention towards sustainability and meeting building safety regulations after Grenfell. Public sector procurement continues to be significant, while private clients are investing in smart buildings and retrofitting existing buildings. The trend towards modular construction and digital engineering tools is affecting the way firms plan and deliver engineering services across sectors.

Engineering services market in Germany is driven by industrial modernization, energy transition objectives, and infrastructure resilience. Engineering companies are backing energy-efficient building retrofits, public transport system upgrades, and automotive sector transformation. The nation's initiative towards renewable energy and hydrogen infrastructure has generated engineering demand in complicated energy systems. Moreover, old bridges, tunnels, and roads are being refurbished with technical assistance from civil and structural engineering companies. In production, firms are looking for process engineering and automation services in order to remain competitive. Digital engineering technologies such as simulation tools and BIM are being widely used to enhance project efficiency and compliance.

Key Engineering Services Company Insights

Some of the key players operating in the market are STRABAG SE, Jones Lang LaSalle Incorporated, Balfour Beatty Inc., among others.

-

STRABAG SE offers engineering services related to construction in the areas of transportation infrastructure, building construction, and civil engineering. The firm has its headquarters in Austria and serves all over Europe and chosen overseas markets. STRABAG deals with technical facility management, large-scale infrastructure projects, and integrated design-to-delivery engineering solutions such as energy and environmental technologies.

-

Jones Lang LaSalle Incorporated (JLL) provides engineering and technical consulting solutions as part of its overall real estate and facilities management business. JLL provides building systems design, energy management, sustainability, and infrastructure optimization solutions. It provides services to industries such as commercial real estate, industrial facilities, and public infrastructure.

-

Balfour Beatty Inc. offers engineering and construction services across the civil infrastructure, transportation, and utilities markets. Headquartered in the UK with substantial operations in the U.S., the firm undertakes sophisticated engineering work such as railways, highways, and energy networks. It also offers lifecycle support such as maintenance and refurbishment.

AECOM Engineering Company, NV5 Global, Inc., and Barton Malow are some of the emerging market participants in the Engineering Services Market.

-

AECOM Engineering Company provides multidisciplinary engineering, architecture, and construction services for sectors such as transportation, water, defense, and environmental systems. AECOM is active globally, working with public authorities and private clients on long-term capital improvement programs and infrastructure modernization.

-

NV5 Global, Inc. is a company which provides infrastructure, environmental, utility, and construction market compliance, consulting, and engineering services. NV5's services include geotechnical engineering, transportation design, energy optimization, and building code consulting. NV5 both consults private developers and works with public sector agencies, primarily in North America.

-

Barton Malow is an American company providing construction and engineering solutions in the industrial, education, healthcare, and sports markets. The firm assists project delivery using design-assist, integrated project delivery (IPD), and preconstruction services, with a focus on efficiency and teamwork in the engineering stage.

Key Engineering Services Companies:

The following key companies have been profiled for this study on the engineering services market.

-

STRABAG SE

-

Jones Lang LaSalle Incorporated

-

Balfour Beatty Inc.

-

Kiewit Corporation

-

AECOM Engineering company

-

NV5 Global, Inc.

-

Barton Malow

-

Brasfield & Gorrie LLC

-

Nearby Engineers

-

RMF Engineering Inc.

-

Bechtel Corporation

-

Gilbane Building Company

-

WSP Global Inc.

-

Jacobs Engineering Group

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (STRABAG SE, Jones Lang LaSalle Incorporated, Balfour Beatty Inc.)

- Focus on expanding end-to-end engineering service portfolios across infrastructure, industrial, and energy sectors.

- Strengthening global delivery centers and offshore engineering hubs for cost-efficient project execution and scalability.

- Strong global engineering expertise and long-term client relationships across infrastructure and industrial domains.

- Ability to deliver integrated multidisciplinary engineering solutions combining design, consulting, and project management services.

- High dependence on traditional engineering processes limits rapid digital transformation and agility.

- Large organizations have slower decision cycles than emerging digital-first engineering firms.

Emerging Players (AECOM Engineering Company, NV5 Global, Inc., Barton)

- Focus on building niche engineering capabilities in digital design, simulation, and AI-driven modeling services.

- Leverage cloud-based engineering platforms and flexible delivery models to target cost-sensitive project opportunities.

- Agile organizational structures enable faster adoption of digital engineering tools and emerging technologies.

- Ability to deliver customized, cost-effective engineering solutions for small and mid-scale projects globally.

- Limited global presence restricts access to large-scale infrastructure and high-value engineering contracts.

- Lower investment capacity limits adoption of advanced digital engineering platforms and R&D expansion.

Recent Developments

-

In 2024, STRABAG SE, together with PORR AG, entered into a purchase agreement to buy assets of the VAMED Group, including Vienna General Hospital (AKH Wien) technical operations management and construction projects divisions, Austrian project development business, and spa holdings, for around €90 million. The acquisition is expected to strengthen the service portfolio of STRABAG in technical facility management in the medical segment.

-

In 2025, Balfour Beatty won an $889 million deal from the Texas Department of Transportation to rebuild 2.3 miles of Interstate 30 in east Dallas County. The project will start pre-construction work in 2026, demonstrating the company's presence in the U.S. infrastructure market.

-

In 2024, Glenfarne Group LLC hired Kiewit as the construction contractor for its planned Texas LNG export terminal in Brownsville, Texas. The facility will be capable of converting about 0.5 billion cubic feet per day of natural gas into 4 million tonnes of liquefied natural gas per year. Construction was scheduled to start by November 2024.

Engineering Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 3,578.2 billion

Estimated market size in 2026

USD 3,759.5 billion

Projected market size by 2033

USD 5,778.0 billion

Growth rate

CAGR of 6.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Engineering service type, engineering discipline, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; U.K.; Germany; France; China; Australia; Japan; India; South Korea; Brazil; South Africa; Saudi Arabia; UAE

Key companies profiled

STRABAG SE; Jones Lang LaSalle Incorporated; Balfour Beatty Inc.; Kiewit Corporation; AECOM Engineering company; NV5 Global, Inc.; Barton Malow; Brasfield & Gorrie LLC; Nearby Engineers; RMF Engineering Inc.; Bechtel Corporation; Gilbane Building Company; WSP Global Inc.; Jacobs Engineering Group

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Engineering Services Market Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest technology trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global engineering services market report based on engineering service type, engineering discipline, application, end-use and region:

-

Engineering Service Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Design and Development

-

Consulting

-

Construction and Project Management

-

Maintenance and Support

-

Specialized Engineering Services

-

Technology Integration

-

-

Engineering Discipline Outlook (Revenue, USD Million, 2021 - 2033)

-

Civil

-

Mechanical

-

Electrical

-

Piping and Structural

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Infrastructure Development

-

Industrial Projects

-

Technology Implementation

-

Environmental Projects

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Infrastructure Development

-

Industrial Projects

-

Technology Implementation

-

Environmental Projects

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Research Methodology

Segment Definition

Segment - Engineering Service Type

Revenue capture definition

Design and Development

Revenue is generated through engineering design services that include conceptual planning, detailed drafting, simulation modeling, and product or infrastructure development. This segment is a core revenue contributor as organizations increasingly rely on advanced digital engineering tools and integrated design platforms to improve accuracy, reduce development cycles, and optimize overall project outcomes.

Consulting

Revenue is captured through engineering consulting services that provide feasibility analysis, technical advisory, regulatory compliance guidance, and project planning support. This segment plays a critical role in early-stage decision-making, helping clients evaluate technical risks, improve project viability, and align engineering strategies with cost, sustainability, and operational efficiency objectives.

Construction and Project Management

Revenue is generated through end-to-end project execution services, including construction supervision, scheduling, resource coordination, and lifecycle project management. This segment is a major revenue driver as organizations increasingly outsource project delivery functions to ensure timely execution, cost control, quality assurance, and seamless coordination.

Maintenance and Support

Revenue is generated through post-project engineering services, including system maintenance, asset optimization, performance monitoring, and technical support. This segment is growing as industries focus on extending asset life cycles, reducing operational downtime, and improving long-term reliability of infrastructure, industrial systems, and utility networks through continuous engineering support.

Specialized Engineering Services

Revenue is captured through niche engineering services such as structural analysis, environmental engineering, geotechnical studies, and high-precision technical modeling. This segment is gaining traction as projects become more complex and require domain-specific expertise to ensure compliance, safety, and optimized performance under varying operational conditions.

Technology Integration

Revenue is generated through the integration of digital technologies such as BIM, IoT systems, AI-based engineering platforms, and cloud collaboration tools into traditional engineering workflows. This segment is expanding rapidly as organizations adopt digital transformation strategies to improve real-time decision-making, enhance design accuracy, and enable connected engineering ecosystems.

Segment - Engineering Discipline

Revenue capture definition

Civil

Revenue is generated through civil engineering services focused on infrastructure design, urban development, transportation systems, and large-scale construction planning. This discipline remains a key revenue contributor due to rising investments in smart cities, public infrastructure modernization, and large-scale urban expansion projects.

Mechanical

Revenue is captured through mechanical engineering services involving machine design, thermal systems, manufacturing equipment development, and industrial system optimization. This segment is driven by increasing demand for automation, advanced manufacturing systems, and energy-efficient mechanical solutions across industrial sectors.

Electrical

Revenue is generated through electrical system design, power distribution planning, control systems, and energy infrastructure development. This segment is expanding due to growing investments in renewable energy systems, smart grids, electrification projects, and industrial power optimization initiatives.

Piping and Structural

Revenue is captured through structural design and piping system engineering used in industrial plants, oil and gas facilities, and large-scale infrastructure projects. This segment is essential for ensuring safety, durability, and operational efficiency in high-load and high-pressure engineering environments.

Segment - Application

Revenue capture definition

Infrastructure Development

Revenue is generated through engineering services for roads, bridges, airports, railways, and urban infrastructure systems. This segment is a major growth driver due to global urbanization, government investments, and smart infrastructure development initiatives.

Industrial Projects

Revenue is captured through engineering support for manufacturing plants, processing facilities, and heavy industrial installations. This segment is driven by increasing industrial automation, capacity expansion, and modernization of production facilities.

Technology Implementation

Revenue is generated through integration of digital engineering systems, automation platforms, and smart technologies into existing infrastructure and industrial operations. This segment is expanding as organizations accelerate digital transformation initiatives across engineering workflows.

Environmental Projects

Revenue is captured through engineering services focused on sustainability projects, waste management systems, water treatment facilities, and environmental compliance solutions. This segment is growing due to increasing regulatory pressure and rising emphasis on sustainable development practices.

Others

Revenue is generated through specialized and emerging engineering applications that do not fall into conventional categories, including research-driven projects, experimental designs, and custom engineering solutions tailored to unique client requirements.

Segment - End Use

Revenue capture definition

Construction

Revenue is generated through engineering services supporting residential, commercial, and large-scale construction projects. This segment remains highly active due to continuous urban development and infrastructure expansion activities.

Manufacturing

Revenue is captured through engineering support for production facilities, industrial automation systems, and manufacturing process optimization. This segment is driven by the adoption of Industry 4.0 technologies and smart factory initiatives.

Energy and Utilities

Revenue is generated through engineering services for power plants, renewable energy systems, transmission networks, and utility infrastructure. This segment is expanding due to global energy transition and increasing investments in sustainable energy solutions.

Transportation

Revenue is captured through engineering design and planning for aviation, rail, road, and maritime transport systems. This segment is driven by modernization of transport infrastructure and rising demand for efficient mobility systems.

Healthcare

Revenue is generated through engineering services for hospital infrastructure design, medical facility planning, and healthcare system optimization. This segment is growing due to rising investments in advanced healthcare infrastructure and facility modernization.

Telecommunications

Revenue is captured through engineering support for telecom infrastructure, network design, data centers, and connectivity systems. This segment is expanding rapidly due to 5G deployment and increasing demand for high-speed digital connectivity.

Others

Revenue is generated through specialized end-use applications across emerging sectors that require tailored engineering solutions, including research institutions, defense-related infrastructure, and niche industrial domains.

Estimation Model

Layer Name

Key Question

Description

Industrial Base Layer

Who are potential adopters of engineering services?

Identify the total addressable base, including infrastructure developers, manufacturing facilities, energy plants, construction companies, transportation networks, and industrial operators across global regions requiring engineering design and support services.

Capability Readiness Layer

Who can execute engineering services projects?

Filter the addressable base based on engineering maturity, digital adoption readiness, project complexity, outsourcing capability, and availability of in-house engineering expertise across organizations.

Deployment Layer

Who actively engages in engineering service providers?

Apply engineering service adoption rates across ready industries engaging in design, consulting, project management, maintenance, and technology integration for infrastructure, industrial, and technology-driven projects.

Revenue Generation Layer

How much revenue is generated?

Estimate revenue generated from design and development services, consulting contracts, project management fees, maintenance agreements, specialized engineering projects, and digital engineering integration services such as BIM, simulation, and digital twin solutions.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Infrastructure Planning, Design Engineering & Project Feasibility Analysis

Conducted detailed engineering design and feasibility studies across infrastructure project planning, transportation networks, building systems, and industrial facilities, integrating BIM modeling, simulation tools, and digital design workflows.

Helps stakeholders identify optimal design alternatives, reduce project risks, improve cost efficiency, and enhance planning accuracy for large-scale infrastructure development programs.

Industrial Engineering, Process Optimization & Digital Transformation Strategy

Evaluated industrial systems and manufacturing facilities to deliver process engineering, workflow optimization, automation integration, and digital engineering strategies using AI-based simulation, IoT integration, and advanced modeling tools.

Provides insights into operational efficiency improvements, production cost reduction, and scalable engineering strategies supporting smart manufacturing and Industry 4.0 transformation initiatives.

Project Execution, Asset Management & Engineering Lifecycle Optimization

Assessed engineering project execution requirements including construction management, procurement support, maintenance planning, and lifecycle asset optimization across infrastructure and industrial assets.

Supports efficient project delivery, improved asset performance, reduced downtime, and long-term operational sustainability through integrated engineering management and monitoring solutions.

Frequently Asked Questions About This Report

Key drivers include the adoption of automation, AI, and IoT, which enhance productivity and efficiency. Rapid urbanization and government investments in infrastructure, along with the push for eco-friendly practices due to stringent environmental regulations, are also propelling the market.

Specialized engineering services segment dominated the market, with a share of 19.2% in 2025.

Civil segment accounted for the largest market share of 27.7% in 2025.

Environmental projects segment held the largest market share in 2025.

The Asia Pacific engineering services market dominated with a share of 37.1% in 2025.

The global engineering services market size was estimated at USD 3,578.2 billion in 2025 and is expected to reach USD 3,759.5 billion in 2026.

The global engineering services market is expected to grow at a compound annual growth rate of 6.3% from 2026 to 2033 to reach USD 5,778.0 billion by 2033.

Some key players operating in the engineering services market include STRABAG SE, Jones Lang LaSalle Incorporated, Balfour Beatty Inc., Kiewit Corporation, AECOM Engineering company, NV5 Global, Inc., Barton Malow, Brasfield & Gorrie LLC, Nearby Engineers, RMF Engineering Inc, Bechtel Corporation, Gilbane Building Company, WSP Global Inc among others.

Telecommunications segment accounted for the largest revenue share in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.