- Home

- »

- Advanced Interior Materials

- »

-

Battery Raw Materials Market Size, Share Report, 2026-2033GVR Report cover

![Battery Raw Materials Market Size, Share & Trends Report]()

Battery Raw Materials Market (2026 - 2033) Size, Share & Trends Analysis Report By Battery Type (Lithium-Ion, Lead-Acid), By Material Type, By Application, By Region (North America, Europe, Asia Pacific, Middle East & Africa, Central & South America), And Segment Forecasts

Market Size, 2025

$62.4BMarket Estimate, 2026

$67.6BMarket Forecast, 2033

$127.4BCAGR, 2026–2033

9.5%Battery Raw Materials Market Summary

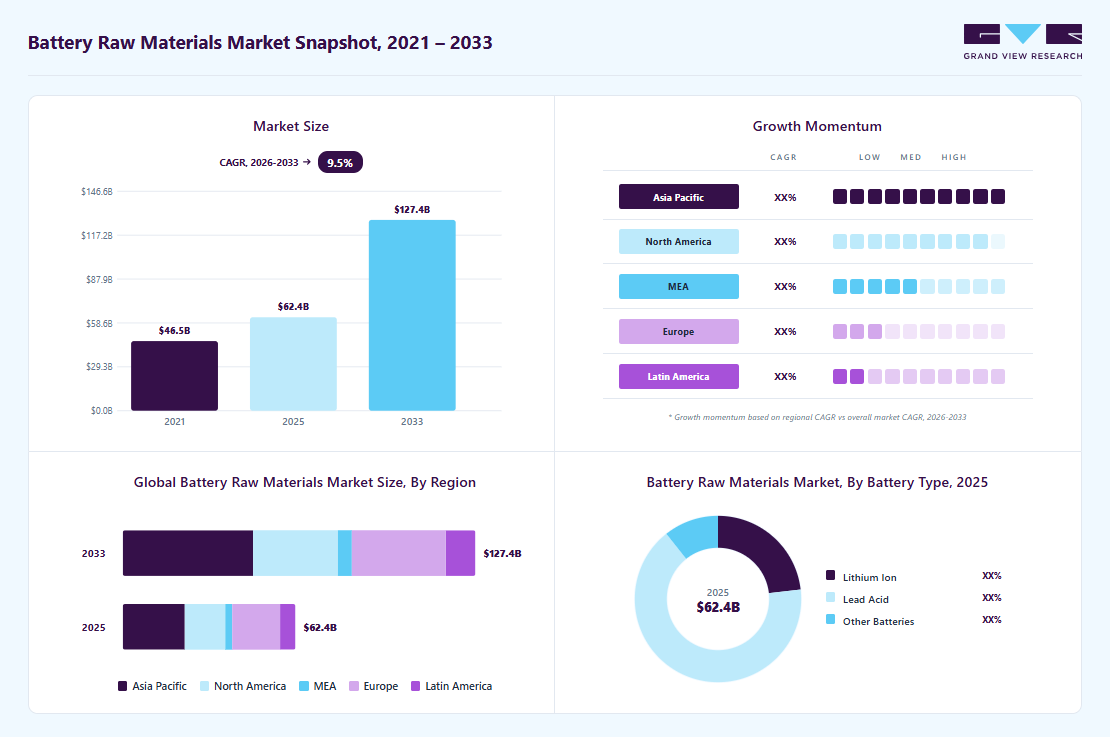

The global battery raw materials market size was valued at USD 62.4 billion in 2025 and is projected to grow from USD 67.6 billion in 2026 to USD 127.4 billion by 2033, growing at a CAGR of 9.5% from 2026 to 2033. Asia Pacific dominated the industry with the largest revenue share of 35.8% in 2025. This growth is attributed to rising demand for lithium-ion batteries from the automotive industry for use in electric vehicles.

Key Market Trends & Insights

- By battery type: Lithium-ion segment is expected to grow at the fastest CAGR of 10.4% over the forecast period.

- By application: lithium-ion automotive segment is expected to grow at the fastest CAGR of 10.7% over the forecast period.

Regional Highlights

- Largest regional market: Asia Pacific (35.8% revenue share, 2025)

- Battery raw materials market in the U.S. accounted for the largest share of 75.2% in North America in 2025.

Market Size & Forecast

- Market size in 2025: USD 62.4 Billion

- Estimated market size in 2026: USD 67.6 Billion

- Projected market size by 2033: USD 127.4 Billion

- CAGR (2026-2033): 9.5%

Moreover, the rising adoption of renewable energy sources, including wind and solar, is expected to fuel demand for energy storage solutions, thereby boosting the battery raw materials market. The expansion of portable electronic devices such as laptops and smartphones is also likely to contribute to the growth of battery materials over the forecast period. Ongoing technological advancements for improving battery performance, including the adoption of nuclear batteries in the future, are expected to create opportunities for industry growth.

")

Companies in the battery raw material industry position themselves as miners and processors of the key materials used in rechargeable batteries for electric vehicles, consumer electronics, and other applications. Players in this domain are increasingly adopting green extraction technologies to reduce energy and water consumption during material processing, both to appeal to a broader customer base and to mitigate the environmental impact of resource extraction.

Market Concentration & Characteristics

The industry growth stage is medium, and the pace of growth is accelerating. The industry is characterized by many public companies that process raw materials worldwide, providing unique battery components for various end-use applications. These companies account for a relatively large share of global annual raw material production. Industry players compete by adopting innovative techniques and acquiring patents to leverage higher battery raw-material costs and increase revenue. Companies also compete on the basis of profit margins due to large-scale volumetric production consumed by the end use industries.

The industry for battery raw materials is driven by the growth of the regulations set for safe handling of hazardous materials in manufacturing, mining, transportation for human health, and preservation of the environment. Lithium batteries, due to their inherent dangers, pose safety risks; thus, regulations are in place in developed and emerging economies regarding their use, shipping, and disposal.

The industry exhibits the presence of fewer substitutes for raw materials used for lithium-ion and lead-acid batteries. There are companies involved in using innovative materials with different combinations of metals for reduced use of energy. The processing technology used for manufacturing battery materials increases additional charges. In addition, it is seen that the established end-use industry players have a propensity towards using established products which is anticipated to reduce the threat of substitutes in the industry.

Battery Type Insights

Lead acid battery was the largest segment and accounted for more than 66.3% of the global revenue share in 2025, growing at a CAGR of 9.2% over the forecast period. The industry is driven by various factors such as their lower cost of production, established technology, and reliable and robust recycling infrastructure. The lead-acid battery is preferred in industries with critical expenses, including automotive lighting and ignition systems, where durability and cost-effectiveness are essential. In addition, benefits offered by lead-acid batteries, such as longer lifespan and high energy density, are further likely to contribute to industry growth.

The demand for lithium-ion battery materials is on a rapid rise, primarily driven by increasing adoption of electronic vehicles, consumer electronics, and renewable energy storage solutions. Lithium-ion batteries, being essential components in these applications, are significantly driving up demand for materials such as nickel, cobalt, lithium, and graphite. Furthermore, government initiatives to reduce greenhouse gas emissions and promote clean energy solutions are expected to further boost demand for lithium-ion batteries over the forecast period.

Material Insights

The electrodes segment of lead-acid battery led the material segment and accounted for a revenue share of over 54.0% of the global revenue in 2025 and is expected to witness significant growth for battery materials over the forecast period. The widespread adoption of lead-acid batteries has boosted demand for electrodes. These electrodes consist of lead oxide and sponge lead, essential components of lead-acid batteries, enabling electrochemical reactions necessary for energy storage and discharge. This segment dominance is further fueled by well-established manufacturing processes for lead-acid batteries, which have enabled efficient production and economies of scale.

The lithium nickel manganese cobalt oxide (NMC) segment of cathode lithium-ion batteries is anticipated to grow at the fastest rate over the forecast period. NCM is considered most precious combination of metals with a continuous discharge of 20 A at 2000mWh. The material is observed to have high specific energy and high specific power. Generally, lithium-ion batteries with cathode material such as NMC are used in power applications and electric vehicles. The material contains one-third of all three components, lowering raw material cost for battery. In addition, due to its low self-heating rate, it is used in electric vehicles. The abundant usage of NCM in cathode and its lower cost are anticipated to drive industry growth over the forecast period.

Application Insights

The automotive segment has dominated the overall application segments with a revenue share of 37.7% in 2025. Lead-acid batteries have been widely used in automotive applications owing to their reliability, cost-effectiveness, and well-established technology. These batteries are particularly well suited for automotive starting and ignition systems, providing the necessary power to start the engine and support various electrical components. Moreover, established manufacturing processes and distribution networks make them easily accessible to automotive manufacturers and consumers.

The grid storage application of lithium-ion batteries is expected to grow significantly over the forecast period. As the world is moving towards using renewable energy sources to fulfill energy security, growth has been noted in the grid storage system over forecast period. Grid storage systems use lithium batteries for the storage of power, which is driving industry for battery raw materials over the forecast period.

Regional Insights

The Asia Pacific battery raw materials market accounted for a revenue share of 35.8% of the global demand in 2025, owing to factors including robust domestic demand, recovery in the commodity prices, falling poverty rates, and rising labor income. The supply of raw materials between the countries of the region is estimated to be effortless and robust with integrated supply chain operation established in region, which is forecasted to drive the industry growth for battery raw materials over the coming years.

The battery raw materials market in India is expected to grow at a CAGR of 10.1% over the forecast period. The industry is expected to grow with increasing job opportunities, a regularized tax structure, a globally integrated supply chain, and acceptance of foreign direct investments (FDI) and manufacturing facilities. There is an increase noted in spending capacity of citizens of India in consumer electronics and solar panel sectors on account of growing urban population and on account of government directives on using renewable and alternative energies in place of conventional ones, which is anticipated to drive the industry growth over the forecast period.

Europe Battery Raw Materials Market Trends

The battery raw materials market in Europe is anticipated to grow at a significant CAGR from 2026 to 2033. Europe is forecasted to see the arrival of factories dedicated to manufacturing batteries installed in electric cars. The inauguration of factories in this region is focused on shifting car manufacturing to green power-operated vehicles and utilities, which is expected to create opportunities for battery materials in the coming years.

Germany's battery raw materials market accounted for the largest revenue share of 24.0% in 2025. The presence of electric vehicles positively impacts the economy of Germany as, according to the government of Germany, it is planning to discontinue the usage of ICE engines, looking forward to adopting greener fuel for whole country, which is estimated to drive the industry growth for batteries.

The battery raw materials market in the UK is anticipated to grow at a CAGR of 9.0% over forecast period. The UK has a large influx of lithium-ion battery manufacturers spread across the region, producing various components, which is expected to increase demand for battery raw materials over the forecast period.

North America Battery Raw Materials Market Trends

The batteryraw materials market in North America region is expected to witness rapid growth. The North American economy is one of strongest economies in the world, with tightly integrated markets of the U.S., Canada, and Mexico for manufacturing and distributing automotive, electronics, and other supplies. The region is abundant with rich and varied resources wealth, with a substantial percentage of steel, copper, lead, zinc, iron, oil, and others in this region, which is favorable for the establishment of manufacturing facilities for battery raw materials over the forecast period.

U.S. Battery Raw Materials Market Trends

Battery raw materials market in the U.S. accounted for the largest share of 75.2% in North America in 2025. The region is constituted by many regulations established by agencies on mining, processing, recycling, and transportation of lithium-ion batteries due to risk they pose to human health and environment. Certain regulations, such as those issued by the U.S. Department of Transportation, are listing certain materials as hazardous, thereby improving the value chain of battery raw materials and driving the industry over the forecast period.

The battery raw materials market in Canada is expected to grow at a CAGR of 9.8% over the forecast period. Canada is rich in natural resources, including minerals, metals, and salts. It is second in line in the production of nickel, cobalt, and aluminum and fifth in manufacturing of graphite, which is anticipated to drive industry.

Central & South America Battery Raw Materials Market Trends

The battery raw materials market in the Central & South America region is expected to witness significant growth over the coming years. A large number of mining companies extract lithium and its compounds in Argentina, Bolivia, and Chile. The mining companies in this region are booming due to increased demand expected from electric car manufacturers. Due to ever-increasing demand for rechargeable batteries, market for its raw materials is anticipated to drive market growth over the forecast period.

The battery raw materials market in Brazil is expected to grow at a CAGR of 9.2% in terms of revenue over the forecast period. The growing market of the automotive sector, including electric and hybrid vehicles across the globe, is anticipated to increase demand for raw materials mined in Brazilian region by a certain percentage, which is presumed to drive market growth moderately over the forecast period.

Middle East & Africa Battery Raw Materials Market Trends

The battery raw materials market in the Middle East & Africa region is anticipated to grow at a significant rate over the forecast period. A rise was observed in the spending capacity of people in the Middle East region on account of lower costs of oil and other commodities in region. Due to an increase in spending capacity, there is a higher demand expected in the electric vehicle application segment, which is anticipated to drive the market growth for battery raw materials over the forecast period.

The battery raw materials market in Saudi Arabia accounted for the largest revenue share of 19.6% in the Middle East & Africa in 2025. The market is characterized by the inclusion of a large number of end-use electronics companies procuring lithium-ion batteries for their sleek designs and rechargeability, used in laptops and notebooks, which is expected to drive market growth for battery raw materials.

Key Battery Raw Materials Company Insights

Some of the key players operating in industry include Targray, NICHIA CORPORATION, BASF Catalysts LLC, and DuPont

-

Targray is engaged in the sourcing, storage, transportation, and supply of sustainable materials for solar, renewable fuels, battery, agricultural commodity industry, and carbon trading.

-

NICHIA CORPORATION is a Japan-based manufacturer and distributor of fine chemicals, especially phosphors, such as battery materials, light-emitting diodes (LEDs), calcium chloride, and laser diodes. The company has a presence in various countries, including Japan, the U.S., China, Taiwan, South Korea, Malaysia, Singapore, Indonesia, Thailand, and India.

Celgard LLC, and NEI Corporation are some of the emerging participants in battery raw materials market.

-

Celgard LLC is engaged in the development and manufacturing of high-performance membrane technology. The company has a vast product line includes technical textiles, medical personal protective equipment (PPE), lithium primary and other specialty battery solutions, and lithium-ion batteries. The company has manufacturing facilities in China and U.S.

-

NEI Corporation is a U.S.-based producer and supplier of advanced materials for a wide range of industries. The company’s product portfolio includes battery materials, protective clothing, electrospun mats, heat transfer fluids.

Key Battery Raw Materials Companies:

The following key companies have been profiled for this study on the battery raw materials market.

- Targray

- ENTEK

- BASF Catalysts LLC

- DuPont

- Hitachi, Ltd.

- NICHIA CORPORATION

- Mitsubishi Chemical Group Corporation

- Celgard LLC

- Umicore N.V.

- NEI Corporation

Recent Developments

-

In February 2023, ENTEK, a U.S.-based manufacturer of lithium-ion battery separator materials, partnered with Brückner Group USA to expand its production line for battery separator film to support the growing demand for electric vehicles and energy storage systems in the U.S.

-

In December 2023, KPIT Technologies, an India-based independent software integration partner in automobile industry, has launched its sodium (Na)-ion battery technology. This technology is expected to reduce dependency on importing core battery materials. Sodium-ion batteries offer a longer lifespan and faster charging than lithium-ion batteries.

Battery Raw Materials Market Report Scope

Report Attribute

Details

Market size in 2025

USD 62.4 billion

Estimated market size in 2026

USD 67.66 billion

Projected market size by 2033

USD 127.43 billion

Growth rate

CAGR of 9.5% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Million/Billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Battery type, material, application, and region

Region scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Brazil; Saudi Arabia

Key companies profiled

Targray; ENTEK; BASF Catalysts LLC; DuPont; Hitachi; Ltd.; NICHIA CORPORATION; Mitsubishi Chemical Group Corporation; Celgard LLC; Umicore N.V.; NEI Corporation

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Battery Raw Materials Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the battery raw materials market report based on battery type, material, application, and region:

-

Battery Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Lithium Ion

-

Lead Acid

-

Other Batteries

-

-

Battery Material Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Lithium Ion

-

Cathode Materials

-

Lithium Cobalt Oxide (LCO)

-

Lithium Nickel Manganese Cobalt Oxide (NMC)

-

Lithium Iron Phosphate (LFP)

-

Lithium Manganese Oxide (LMO)

-

Lithium Nickel Cobalt Aluminum (NCA)

-

-

Anode Materials

-

Natural Graphite

-

Artificial Graphite

-

Amorphous Carbon

-

LTO

-

Si Compounds

-

-

Separator

-

Others

-

-

Lead Acid

-

Electrodes

-

Electrolyte

-

Separator

-

Packaging

-

-

Other Batteries

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Lithium Ion

-

Consumer electronics

-

Automotive

-

Grid storage

-

Others

-

-

Lead Acid

-

Automotive

-

UPS

-

Telecom

-

Others

-

-

Other Batteries

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

-

Frequently Asked Questions About This Report

The global battery raw materials market size was estimated at USD 62.42 billion in 2025 and is expected to reach USD 67.66 billion in 2026.

The key factors that are driving the global battery raw materials market include growing demand for lithium-ion batteries from the automobile industry for their use in electric vehicles.

Some of the key players operating in the battery raw materials market include Targray, ENTEK, BASF Catalysts LLC, DuPont, Hitachi, Ltd., NICHIA CORPORATION, Mitsubishi Chemical Group Corporation, Celgard LLC, Umicore N.V., NEI Corporation.

The global battery raw materials market is expected to grow at a compound annual growth rate of 9.5% from 2026 to 2033 to reach USD 127.43 billion by 2033.

Lead-acid battery type segment led the market and accounted for over 66.3% of the revenue in 2025. The benefits of lead-acid batteries, such as longer lifespan and high energy density, are likely to drive market growth.

Asia Pacific dominated the battery raw materials market with the largest revenue share of 35.8% in 2025.

Lead acid battery was the largest segment and accounted for more than 66.3% of the global revenue share in 2025, growing at a CAGR of 9.2% over the forecast period.

The electrodes segment of lead-acid battery led the material segment and accounted for a revenue share of over 54.0% of the global revenue in 2025 and is expected to witness significant growth for battery materials over the forecast period.

The automotive segment has dominated the overall application segments with a revenue share of 37.7% in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.