Australia Uterine Manipulation Devices Market Size & Outlook

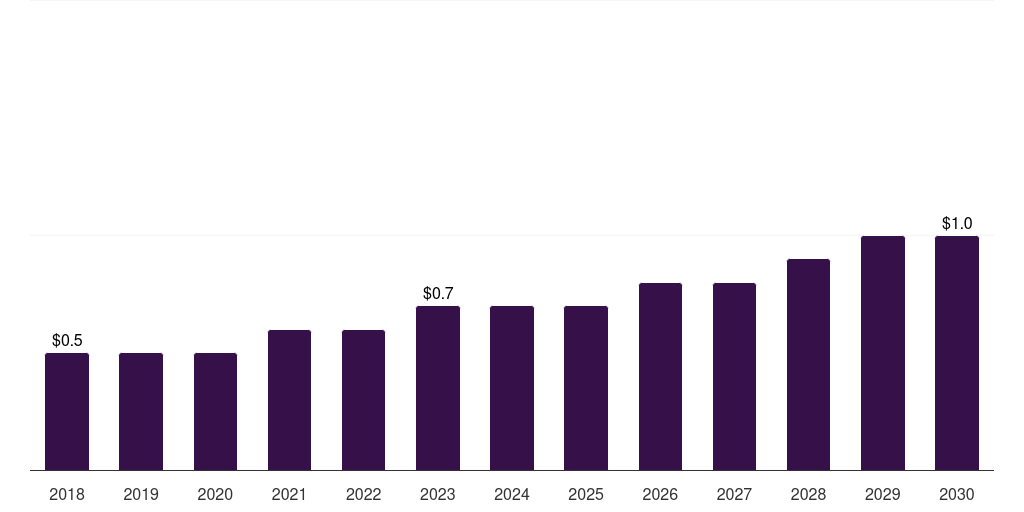

Australia uterine manipulation devices market, 2018-2030 (US$M)

Related Markets

Australia uterine manipulation devices market highlights

- The Australia uterine manipulation devices market generated a revenue of USD 6.3 million in 2023 and is expected to reach USD 9.7 million by 2030.

- The Australia market is expected to grow at a CAGR of 6.4% from 2024 to 2030.

- In terms of segment, total laparoscopic hysterectomy (tlh) was the largest revenue generating type in 2023.

- Laparoscopic Supracervical Hysterectomy (LSH) is the most lucrative type segment registering the fastest growth during the forecast period.

Uterine manipulation devices market data book summary

| Market revenue in 2023 | USD 6.3 million |

| Market revenue in 2030 | USD 9.7 million |

| Growth rate | 6.4% (CAGR from 2023 to 2030) |

| Largest segment | Total laparoscopic hysterectomy (tlh) |

| Fastest growing segment | Laparoscopic Supracervical Hysterectomy (LSH) |

| Historical data | 2018 - 2022 |

| Base year | 2023 |

| Forecast period | 2024 - 2030 |

| Quantitative units | Revenue in USD million |

| Market segmentation | Total Laparoscopic Hysterectomy (TLH), Laparoscopic Supracervical Hysterectomy (LSH), Laparoscopically Assisted Vaginal Hysterectomy (LAVH), Sacrocolpopexy |

| Key market players worldwide | Johnson & Johnson, The Cooper Companies Inc, B. Braun Medical, Karl Storz, Conmed Corp, RUDOLF Medical, LiNA, Richard Wolf, Utah Medical Products Inc, PURPLE SURGICAL MANUFACTURING LIMITED, Conkin Surgical Instruments, Laborie Medical Technologies, Bissinger, The O.R. Company, LSI Solutions |

Other key industry trends

- In terms of revenue, Australia accounted for 2.2% of the global uterine manipulation devices market in 2023.

- Country-wise, U.S. is expected to lead the global market in terms of revenue in 2030.

- In Asia Pacific, China uterine manipulation devices market is projected to lead the regional market in terms of revenue in 2030.

- China is the fastest growing regional market in Asia Pacific and is projected to reach USD 16.6 million by 2030.

No credit card required*

Horizon in a snapshot

- 30K+ Global Market Reports

- 120K+ Country Reports

- 1.2M+ Market Statistics

- 200K+ Company Profiles

- Industry insights and more

Uterine Manipulation Devices Market Scope

Uterine Manipulation Devices Market Companies

| Name | Profile | # Employees | HQ | Website |

|---|

Australia uterine manipulation devices market outlook

The databook is designed to serve as a comprehensive guide to navigating this sector. The databook focuses on market statistics denoted in the form of revenue and y-o-y growth and CAGR across the globe and regions. A detailed competitive and opportunity analyses related to uterine manipulation devices market will help companies and investors design strategic landscapes.

Total laparoscopic hysterectomy (tlh) was the largest segment with a revenue share of 38.1% in 2024. Horizon Databook has segmented the Australia uterine manipulation devices market based on total laparoscopic hysterectomy (tlh), laparoscopic supracervical hysterectomy (lsh), laparoscopically assisted vaginal hysterectomy (lavh), sacrocolpopexy covering the revenue growth of each sub-segment from 2018 to 2030.

The increasing rate of hospitalization due to gynecology procedures, such as uterine fibroids, endometriosis, and other gynecological disorders, and the growing demand for minimally invasive surgical procedures in Australia are among the major factors expected to drive market growth over the forecast period. Uterine fibroids are one of the primary indications for uterine manipulation devices in Australia.

According to the Australian Institute of Health and Welfare 2024, endometriosis is the third leading cause of nonfatal disease burden (YLD) among women due to reproductive and maternal conditions (13%), after genital prolapse (52%) and polycystic ovarian syndrome (26%). Moreover, according to the Australian Burden of Disease Study, in 2023, there were 8,213 YLDs from endometriosis in Australia, a rate of 0.61 per 1,000 females. The disease burden due to endometriosis is highest among women aged 30–34 with a rate of 1.71 YLD per 1,000 women.

The growing demand for minimally invasive surgical procedures is a key factor driving the uterine manipulation devices market growth. Minimally invasive procedures, such as hysteroscopy and laparoscopy, are increasingly preferred by patients and healthcare providers due to their reduced risk of complications, faster recovery time, and minimal scarring. In addition, over 25,000 gynecological laparoscopy procedures are performed in Australia annually, according to the Royal Australian and New Zealand College of Obstetricians and Gynaecologists.

Reasons to subscribe to Australia uterine manipulation devices market databook:

-

Access to comprehensive data: Horizon Databook provides over 1 million market statistics and 20,000+ reports, offering extensive coverage across various industries and regions.

-

Informed decision making: Subscribers gain insights into market trends, customer preferences, and competitor strategies, empowering informed business decisions.

-

Cost-Effective solution: It's recognized as the world's most cost-effective market research database, offering high ROI through its vast repository of data and reports.

-

Customizable reports: Tailored reports and analytics allow companies to drill down into specific markets, demographics, or product segments, adapting to unique business needs.

-

Strategic advantage: By staying updated with the latest market intelligence, companies can stay ahead of competitors, anticipate industry shifts, and capitalize on emerging opportunities.

Target buyers of Australia uterine manipulation devices market databook

-

Our clientele includes a mix of uterine manipulation devices market companies, investment firms, advisory firms & academic institutions.

-

30% of our revenue is generated working with investment firms and helping them identify viable opportunity areas.

-

Approximately 65% of our revenue is generated working with competitive intelligence & market intelligence teams of market participants (manufacturers, service providers, etc.).

-

The rest of the revenue is generated working with academic and research not-for-profit institutes. We do our bit of pro-bono by working with these institutions at subsidized rates.

Horizon Databook provides a detailed overview of country-level data and insights on the Australia uterine manipulation devices market , including forecasts for subscribers. This country databook contains high-level insights into Australia uterine manipulation devices market from 2018 to 2030, including revenue numbers, major trends, and company profiles.

Partial client list

Australia Uterine Manipulation Devices Market Outlook Share, 2024 & 2030 (US$M)

Related industry reports

Related regional statistics

Sign up - it's easy, and free!

Sign up and get instant basic access to databook, upgrade

when ready, or enjoy our

free plan indefinitely.

Included in Horizon account

- 30K+ Global Market Reports

- 120K+ Country Reports

- 1.2M+ Market Statistics

- 200K+ Company Profiles

- Industry insights and more